SATURDAY, MARCH 9, 2013

Could Bed Bath & Beyond Be Buffett Bait?

By ANDREW BARY | MORE ARTICLES BY AUTHOR

With strong profits and steady growth, Bed Bath & Beyond was a great retailing story in the 20th century. The moves it’s making could make it an even better story in the 21st.

One of the country’s most successful retailers is on the bargain counter.

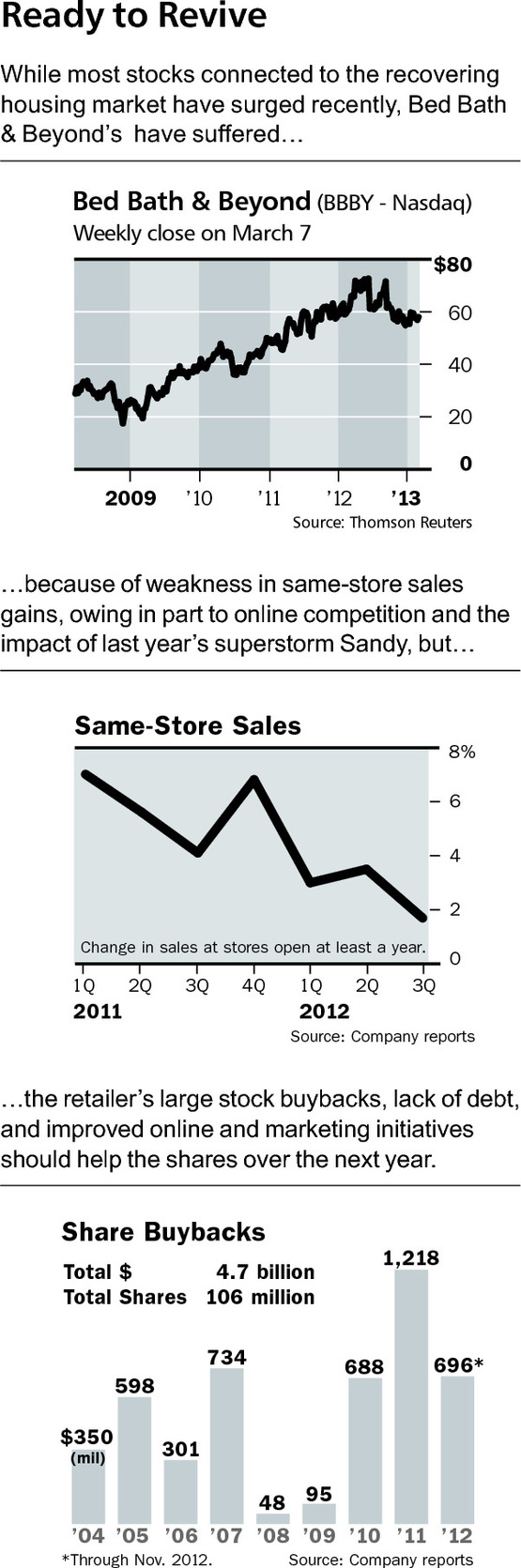

Bed Bath & Beyond has generated 16% annual growth in earnings per share over the past 10 years. But its shares, at $59, trade for less than 12 times projected profit for its fiscal year that ends in February 2014. The stock (ticker: BBBY) trades at a discount to other top retailers’, including Costco Wholesale (COST) and Target (TGT), neither of which has such a good profit history.

The shares could trade into the $70s in the next year, simply based on projected earnings gains and a higher price/earnings multiple. The insular company could attract interest from private-equity investors or even Berkshire Hathaway (BRK.A) if Bed Bath & Beyond’s co-founders, Leonard Feinstein, 75, and Warren Eisenberg, 82, decide to sell. However, there is no indication that the company is looking to sell.

A BUYER MIGHT PAY $85 a share—roughly 10 times this fiscal year’s projected earnings before interest, taxes, depreciation, and amortization (Ebitda)—consistent with prices paid for other quality companies, versus Bed Bath & Beyond’s current modest valuation of 6.5 times. The company’s $13 billion market value makes it large, but digestible. “This is a high-quality, cash-rich company that could see improving margins this year, particularly in the back half,” says Laura Champine, an analyst at Canaccord Genuity who carries a $74 price target on the stock. Bed Bath & Beyond has commanded an average of 15 times forward earnings in the past seven years.

The company, based in Union, N.J., operates 1,469 stores, including 1,004 Bed Bath & Beyonds, in all 50 states. The other 400-plus stores include World Market, which sells home furnishings, wine, and gourmet food; the fast-growing buybuy Baby chain, Christmas Tree Shops, and Harmon discount shops.

Bed Bath & Beyond has fallen from favor on Wall Street because of slowing comparable-store sales gains, mild profit disappointments, and concern that its weak Website makes it vulnerable toAmazon.com (AMZN) and other top Internet retailers. The company’s shares have slid 6% in the past year, even as virtually all stocks connected to the improving housing sector have surged.

Nonetheless, the company’s earnings in its just-concluded fiscal year ended in February likely rose a healthy 12%, to $4.56 a share, and are projected to increase 10% in its current fiscal year to $5.03.

Bed Bath & Beyond could be the most financially conservative big retailer in the U.S. It has no debt and it hasn’t carried a smidgen of debt for nearly all of the two decades since it went public in 1992. And it has $859 million—nearly $4 a share—in cash and marketable securities. The company has grown enormously, with revenue hitting an estimated $10.9 billion last year, versus $216 million in 1992 and it has accomplished this entirely with internally generated funds. Longtime investors have huge gains; the split-adjusted initial-offering price was $1 a share.

Management, led by CEO Steve Temares, plus co-Chairmen Feinstein and Eisenberg, run Bed Bath as if it were a private company. There are no investor days, limited financial disclosure, and no opportunity for questions on earnings conference calls. Want to know the sales breakdown among its chains? Bed Bath doesn’t disclose it. The retailer didn’t return Barron’s calls seeking comment. Read more of this post