Low-Quality Stocks Have Zoomed. Time to Shift Gears?

March 23, 2013 Leave a comment

March 22, 2013, 6:22 p.m. ET

Low-Quality Stocks Have Zoomed. Time to Shift Gears?

By MARK HULBERT

“Junk” continues to beat “quality” on Wall Street. Nearly four years after the end of the recession of 2007-09, it should be the other way around.

The Federal Reserve’s monetary stimulus is a big reason for this unexpected outcome.

Because the Fed’s easy-money policies won’t continue indefinitely, however, investors might want to begin reducing their holdings of low-quality stocks—which will be among the biggest casualties when the Fed turns off the spigot.

The Fed policies have distorted the markets because they encourage risk-taking. Through its quantitative-easing programs of injecting money directly into the economy, and by keeping short-term interest rates close to zero, the Fed has discouraged investors from keeping their money in conservative savings accounts and created powerful incentives for them to put more money into stocks.

So-called junk stocks—the ones that have been the biggest beneficiaries of the Fed’s policies—are those of companies that otherwise would run the greatest risk of going bankrupt. They tend to be loaded with debt and have poor balance sheets. Even worse, they also tend to have inconsistent and unpredictable earnings.

Revlon REV -1.28% was a good example of such a company in March 2009, when the bull market began. It had lost money over the previous two years and had so much debt that its liabilities were more than double its total assets. Yet, propelled by a successful turnaround strategy, the stock has gained more than 800% from March 2009 until now.

Wal-Mart Stores WMT +1.57% is a classic example of a high-quality company, having turned an impressive profit even during the worst days of the 2008 credit crunch. The company has little long-term debt and has a dividend yield of 2.6%. Even though its stock over the long term has been a stellar performer, during the recent bull market it has lagged behind the overall market: Since the bull market began in March 2009, it has gained just over 50%, trailing the Standard & Poor’s 500-stock index by more than 70 percentage points.

The typical pattern, according to data going back to the 1920s compiled by Eugene Fama and Ken French, finance professors at the University of Chicago and Dartmouth College, respectively, is for junk to outperform quality for no more than the first year of a bull market. Thereafter, market leadership shifts to the stocks of the highest-quality companies. Thanks in large part to the Fed’s easy-money policies, however, this shift hasn’t taken place—as Revlon’s and Wal-Mart’s performance attests.

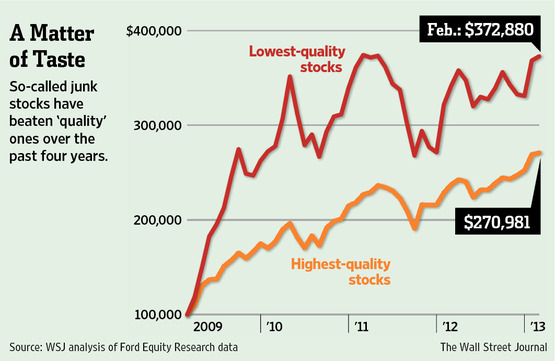

Consider two groups of stocks that were constructed according to financial-quality ratings from Ford Equity Research of San Diego. These ratings are based on factors such as debt, balance-sheet health, earnings consistency and industry stability. The first group contained the 20% of the firm’s universe of more than 4,000 U.S. stocks with the firm’s highest financial-quality ratings, while the other group contained those with the lowest ratings—junk, in other words.

Since March 2009, according to Ford, the average junk stock has gained 273%, versus 171% for the typical high-quality stock. And there is no recent evidence that this trend has reversed: Over the past three months, for example, junk has increased its lead, gaining 12.1% versus 9.6% for quality.

To appreciate just how much the Fed’s policies have been responsible for this pattern, consider how returns since March 2009 have depended on whether the Fed increased or decreased its monetary stimulus. When the Fed’s quantitative-easing programs were fully in force, junk handily won—turning in an average monthly gain of 5.6%, versus 3.4% for quality. During all other months, the average junk stock actually incurred a slight loss, versus a 0.7% monthly gain for the average quality stock.

This contrast offers a glimpse into how the stock market is likely to behave when the Fed finally does bring quantitative easing to an end and begins to increase interest rates. Not only will the market as a whole face stiffer headwinds, but previously highflying junk stocks could be big casualties. Banking stocks, and the financial sector generally, could be particularly hard hit.

Conservative investors might therefore want to begin now to shift their portfolios toward stocks of the highest financial-quality companies. Examples of stocks that Ford rates A-plus for financial quality, its highest rating, include, besides Wal-Mart,Abbott Laboratories, ABT +0.63% Coca-Cola KO -0.07% and Johnson & Johnson JNJ +0.92% . Each of these four has an S&P 500 quality rating of single-A or higher; the average dividend yield of all four is 2.6%, versus 2.1% for the S&P 500. Their price/earnings ratios, based on projected earnings over the next 12 months, range from 13.5 for Wal-Mart to 18.4 for Coca-Cola, versus 14.1 for the S&P 500.

Examples of stocks that Ford rates lowest for financial quality include Vertex Pharmaceuticals, VRTX +2.87% which has reported a loss in six of the past seven years, and BioMarin Pharmaceutical, BMRN +0.84% which has lost money in five of the past seven years.

There also is an exchange-traded fund that focuses on the stocks of the highest-financial-quality companies: The PowerShares S&P 500 High Quality Portfolio SPHQ +0.53% . This ETF invests in the stocks of companies that Standard & Poor’s rates A-minus or higher, based on the growth and stability of their earnings and dividend records. Its expense ratio is 0.29%, or $29 for every $10,000 invested.

To be sure, the Fed hasn’t given any signals that it plans to bring its monetary stimulus to an end in the very near future. But because the stock market discounts the future, it is unlikely to wait until the Fed finally changes course to begin reflecting a poststimulus world.

—Mark Hulbert is editor of the Hulbert Financial Digest, which is owned by MarketWatch/Dow Jones.