When Will Deposit Haircuts Take Place In Other European Countries?

March 29, 2013 Leave a comment

When Will Deposit Haircuts Take Place In Other European Countries?

Tyler Durden on 03/28/2013 11:55 -0400

When all is said and done, what happened in Cyprus over the past two weeks, is nothing but the culmination of re-marking the “assets” in the country’s financial system (which as noted previously, were a preponderance of worthless Greek bonds and countless other non-performing loans), long priced at assorted “myth” levels, to a long overdue reality. As a result of delaying resolving the mismatch between non-performing assets and liabilities for years, the resolution was one which saw some €16 billion of the total asset base impaired, which in turn necessitated the impairment of billions of deposits: the primary liability funding the Cypriot financial system. Furthermore, as a result of the “Freudian Slip” by the Eurogroup’s new head earlier this week, we know that Cyprus will be the template for all future bank resolutions, which seek to avoid a democratic popular vote of depositor self-impairment (a vote which is now known will never actually pass) and proceed to restructuring the banking sector a la carte, by liquidating bad banks and impairing liabilities to the point where the balance sheet is once again viable (however briefly).

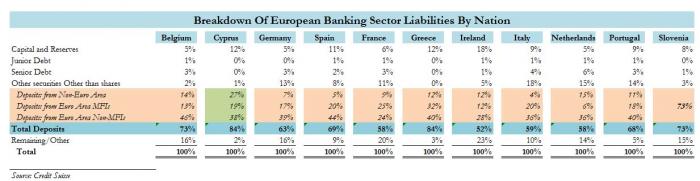

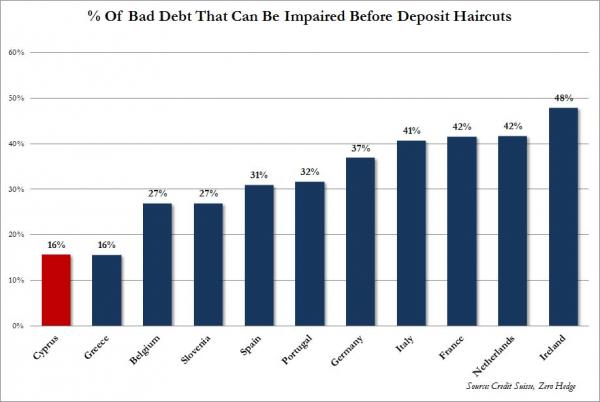

The bottom line is that at its core, it is all simply a bad-debt problem, and the more the bad debt, the greater the ultimate liability impairments become, including deposits. Which means that the real question in Europe is: how much impairment capacity is there in the various European nations before deposits have to be haircut? Thanks to Credit Suisse we now know the answer. The chart below shows the liability breakdown for various Eurozone nations, of which the key line item is the Total Deposits, and which in Europe comprises the bulk of bank funding. It becomes obvious why Cyprus had no choice but to crush depositors: they make up a whopping 84% of all liabilities (the highest in Europe and matched only by Greece), so assuming all other liabilities are liquidated, there still would be impairments if the total bad assets (assuming all bank assets are loans which in Europe, unlike the US, is more or less the case) pushed above 16% which in Cyprus they did. So applying some simple balance sheet equality math, one can quickly calculate how much of a “Bad-Debt Impairment” assorted European financial systems can withstand before they too have no choice but to follow in Cyprus’ footsteps and begin crushing depositors, who in bankruptcy court are known by a different, less friendly term: General Unsecured Claims.

Not surprisingly, in first place is Cyprus which underwent precisely the deposit haircut exercise that would have befallen Greece as well (at the same bad debt capacity), if only Greece had an easily expendable, for political reasons, deposit class – Russian Oligarchs. However, as more and more bad-debt accumulates within the system, the ability to provide a liquidity buffer, instead of resolving what is fundamentally a solvency issue, evaporates, and soon Greece, then Belgium, the Slovenia, then Spain, then Portugal, and so on, will have to address which, as Cyprus clearly demonstrated, is a solvency problem, not liquidity!

When will such days of reckoning happen? Ask the Cypriots: they had no idea they would wake up one day with virtually all of their deposits over €100,000 wiped out. Point being – nobody knows, or more specifically, fundamentally this is a political decision, usually one which is taken ahead of elections (i.e., those in Germany this September), and which has nothing to do with actual finances.

The reality however is that all of Europe’s banks have a soaring bad-asset overhang, and sooner or later it will have to be resolved.

It is now common knowledge that such resolution will not take place via additional liquidity injections, but through impairment of the various liability classes as per the reverse waterfall of seniority: first equity, then capital and reserves then junior debt, and finally, senior debt and deposits (with secured senior debt last).

The lesson here is: do your homework, and know your bank. If one’s deposits are in a bank that has, or is rumored to have, many bad loans, then pull your money and either put it in a safe bank, put it offshore, or just keep it under the mattress.

Because what happened in Cyprus is now, despite all promises to the contrary, the template for what will happen to all the countries to the right of Cyprus on the chart above.

It’s only a matter of “when.”