Keeping debt a dirty secret from investors

April 1, 2013 Leave a comment

Keeping debt a dirty secret from investors

PUBLISHED: 28 MAR 2013 00:33:00 | UPDATED: 29 MAR 2013 00:31:10

CHRISTOPHER JOYE, The Australian Financial Review

Ask yourself this question: is the amount of debt a company assumes, the rate of interest it pays, the events of default, the repayment date and all non-standard conditions (or “covenants”) vital to working out the value of that company’s equity? Any half-witted analyst or investor will emphatically answer “yes”.

Yet when I ask Damian Reichel, a partner at law firm Johnson, Winter & Slattery whether it is standard practice for companies listed on the Australian Stock Exchange to disclose all the terms and conditions of their debt arrangements, he responds: “No, it’s not standard at all. It is, however, normal to disclose the amount of debt outstanding in the company’s accounts and maturity dates so that people know when facilities expire.”

This is a problem that weighs heavily on the minds of sophisticated investors, analysts and even some regulators. While market convention is to disclose little information about a company’s leverage, it is vital to determining its equity value, even if lay retail investors tend to ignore it.

If a company’s capital structure is comprised of debt and equity, it is impossible to price one in isolation from the other. Debt directly subordinates equity in two ways: first, it has a prior-ranking entitlement to the company’s earnings for interest repayments; second, debt ranks ahead of equity if the business is wound up.

The introduction of debt into a capital structure exposes shareholders to new risks. And individuals and companies default on their obligations all the time. When they do, the lender has the right to force asset sales at prices often far below fair value, which inflicts losses on those standing last in the queue – shareholders.To price a company’s equity, it is imperative that you know the value of the debt, the rate of interest, repayment frequencies and all the key events that can trigger default.

While many of these events are boiler-plate (eg, fraud), it is also common for lenders to insert not-so-standard “covenants”. These include requiring the company to keep its ratios of “debt to equity”, “earnings to interest repayments”, and “cash to total repayments” below certain thresholds. Other covenants include change of control events and market capitalisation thresholds. If the company breaches any of these terms, it may be compelled to repay quickly all the debt it has outstanding.

So the more debt a company has the more significant it becomes to valuing the residual equity. Any reasonable investor needs to be able to develop an informed view of the probability of the company defaulting and the losses shareholders will suffer if this comes to pass.

In every private equity transaction I’ve ever seen, investors demand access to all loan information precisely because they need to go through these steps. Yet most ASX investors are denied the same rights.

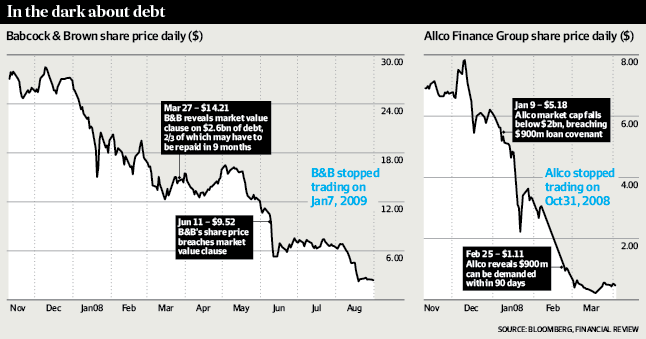

Between January 8 and 9, 2008, Allco Finance Group’s share price fell from $5.61 to $5.18. This pushed the company’s market value below a critical $2 billion milestone, about which shareholders knew nothing. Allco’s directors had agreed to loan facilities that included a covenant which allowed lenders to demand repayment of their debts if Allco’s value fell below the $2 billion mark. Allco did not reveal the covenant’s existence until February 25. By that stage the game was all but over. While Allco’s assets were worth more than its liabilities, its share price tumbled to below $1 because investors knew that it would not be able to meet its debts when they fell due.

A month later, on March 27, Babcock & Brown disclosed to shareholders for the first time it too had agreed to a $2.5 billion market value clause as part of billions worth of debt facilities. Once triggered, two-thirds of all lenders could demand their money back in 90 days after a four-month review. Babcock’s share price had already slumped from more than $25 to $15. Between June 11 and 12, it went into free-fall from $9.52 to $6.90 as Babcock breached the newly-revealed covenant. It was not long before Babcock was placed in administration.

These are just two salutary lessons about the hazards shareholders face when investing in leveraged companies that do not divulge the details of their debt facilities.

The ASX stipulates what information listed companies actually have to release via its “listing rules”, which are incorporated into the Corps Act. The law itself seems robust.

ASX listing rule 3.1 says that once an entity becomes aware of any information that a “reasonable” person would expect to have a “material” effect on a company’s price it must immediately disclose it. The “exceptions” are tightly prescribed. Companies would need to argue both that a reasonable person would not expect the information to be disclosed and that the debt facilities were a trade secret, which seems improbable (although it is a favoured defence).

One high-profile, billion-dollar fund manager, who requested anonymity, believes that “ASIC should absolutely require all companies to disclose key loan terms and conditions”.

“If companies had to reveal this information when they took these loans they would be subject to more scrutiny from shareholders, which would reduce the risk of them entering into agreements that are too lender-friendly or more onerous than what competitors get. Price discovery would be the beneficiary,” he says.

He also argues that the hedge funds and private equity firms investing in companies’ unlisted debt securities often get privileged inside information via access to the facilities’ terms and conditions, which they can then trade on to their advantage.

Lawyers who advise companies on these matters were more resistant. “The detailed terms and conditions of debt facilities are not meaningful to most investors,” Reichel says. “The material issue is whether the company has debt financing, when it matures and whether the company is in compliance.”

Investors counter that if they are only informed about defaults once they occur, they have limited ability to take remedial action. One institutional investor says investors are often never told about the distress. “What happens is they do capital raises, sell businesses and assets, and/or renegotiate the covenants. Billabong was an example of last year. Echo was another. Leighton the year before.”