Cracks appear in China; Triple threat of high leverage, slow economic growth and soaring property prices could spell trouble for world’s second biggest economy; In short, investors should not allow the size of China’s balance sheet to blind them to concerns over the underlying structural risks, given that no economy is too big to fail.

April 2, 2013 Leave a comment

Cracks appear in China

Triple threat of high leverage, slow economic growth and soaring property prices could spell trouble for world’s second biggest economy, some analysts warn.

Published: 1 Apr 2013 at 11.17

Over the past three decades, China has undergone the greatest economic boom in world history, but now it faces a major challenge to sustain its rise. As the European crisis drags on and the US recovery remains slow, a new leadership team in China is struggling to arrest slowing growth.

Opinions vary about whether the world’s second largest economy can achieve a soft landing, or whether it faces a hard landing or even a financial crisis. In any case, some economists have warned that the remaining years of annual economic growth in the high single digits can now be counted on the fingers of one hand.

According to two economists from Nomura, the same three warning signs that preceded severe downturns in Japan, the United States and parts of Europe are now flashing over China. As a result, the government has limited time to contain the growing risks and keep the country out of trouble.

“Those signs include a rapid buildup of leverage, a decline in potential economic growth and skyrocketing property prices. The government needs to take urgent action to contain such risks,” wrote Nomura economists Zhiwei Zhang and Wendy Chen.

“We believe the true extent of financial risks in China is not fully appreciated by investors but tightening its monetary policy will be the way to avoid the crisis.”The Nomura report also revealed that if loose monetary policy is maintained and risks are not brought under control, growth of above 8% in 2013 is still possible. However, it would come at the price of high inflation risk and a financial crisis in 2014.

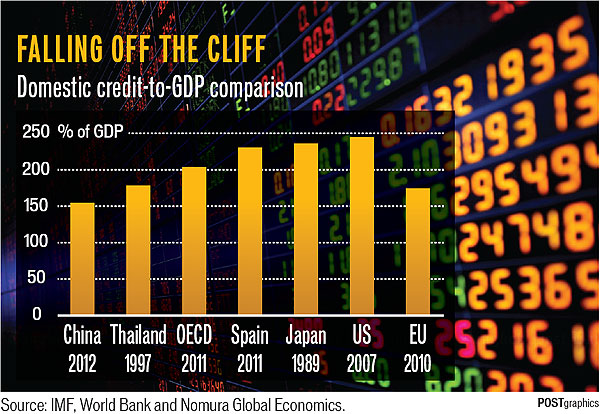

The Japanese investment bank said it was growing more concerned about China, pointing to leverage that has risen by 34% of GDP in five years. Leverage in the US, Japan and the EU rose by around the same pace in the five-year period before crisis struck.

Leverage, defined as the ratio of domestic credit to gross domestic product, increased from 121% in 2008 to 155% in 2012, the highest since records began in 1978. This has been taking place at the same time as falling productivity and a declining labour force start to become a larger potential drag on the economy.

Rapid property price inflation is also a significant warning signal, says Nomura, noting that unusually strong increases in asset prices have typically preceded banking crises.

From the official data, housing prices rose 113% between 2004 and 2012 in major Chinese cities. However, the report said the data were highly “questionable” and “contradictory” to many other observations.

A report by Tsinghua University and National University of Singapore says property prices in China rose by 250% from 2004-12, far outstripping the level of growth in the official index. In addition, land prices rose even more sharply. According to official statistics, the average price per square metre of land sold in 2003 was only US$573, rising to $3,393 in 2012 – an increase of 492% over 10 years.

The government has responded to the risk in the property sector by imposing a series of progressively tighter policies to stabilise prices, including a 20% capital gains tax on home sale profits.

Nomura economists said the pattern has been for house prices to initially dip after tightening policies are introduced. But then prices rebound, which suggests that the risks have not been mitigated.

Moreover, China’s declining potential growth rate also creates a worrisome atmosphere for both domestic and international investors. A shrinking working-age population leading to a slowdown in productivity now represents a threat to growth.

As well, China’s global export market share rose sharply before 2010, but has since come to a halt. This suggests the period of rapid productivity growth after WTO accession has likely ended.

Labour-intensive sectors such as footwear and apparel have been strongly affected. Their export market share has decreased, offsetting the rising share of capital-intensive goods.

The observations by Nomura are in line with the view of the UK bank Barclays, which noted industrial production growth in January and February was lower than expected. The report also noted that retail sales growth decelerated to a two-year low of 12.3% (Barclays had forecast 14.5%, against a consensus of 15.2%) from 15.2% in December and 14.9% in the fourth quarter of 2012.

Barclays also forecast that in light of rising fiscal and financial risks, regulators would tighten oversight of the “shadow banking” sector and local government financing. The China Banking Regulatory Commission on March 12 told banks to stop selling wealth-management products that do not conform to the rules by the end of April.

Concerns remain about how the central government intends to curb the investment enthusiasm of local governments, as two-thirds of them have set growth targets above 10% for 2013.

On the currency side, the renminbi (RMB) has appreciated by 22.9% against the US dollar and 25.7% in relative effective exchange rate (REER) terms between 2005 and 2012. This has substantially widened the wage differential between Chinese workers and those in other emerging economies.

The average wage in China was about twice that in Indonesia in 2000, but by 2011 the figure had risen to 3.5 times. Cumulative wage growth in China was 473.7%, much higher than 238.6% in Indonesia and 137.2% in India, indicating that the country has already lost its price competitiveness.

It is hard to guess when things could unravel, wrote Mr Zhang and Ms Chen of Nomura, adding that China’s policymakers have a lot less flexibility to stimulate the economy than they enjoyed in the past.

“China’s competitiveness is running out of stream and it is no longer attractive to foreign investors,” they wrote. “FDI growth in China may also face downward pressure in the years ahead.”

Not everyone shares Nomura’s pessimism. Michael Thorneman, a China-based managing partner with the global consulting firm Bain & Company, is more sanguine on the country’s prospects.

“The slowdown in the Chinese economy from the double-digit rates of recent decades to the mid-7% range is a structural issue. It is mostly cyclical, given that once an economy matures, such rapid growth simply isn’t sustainable,” Mr Thorneman told Asia Focus.

From a macro perspective, he said, a big shift is occurring as growth has come down to a more sustainable level, but China still has fantastic growth compared to many other economies. He noted that the slowdown has affected many different industries by forcing them to undertake major restructuring. Demand for expertise in this area is good for Bain’s business.

“There are a number of industries that have been hit hard, for example construction, retail and consumer products,” he said. “However, I think it is just a ‘reset’ to a different level. Yet the level right now is still measured to be a very attractive stage in terms of growth opportunity.

“If we look at our clients, generally speaking they still see China as one that offers immense opportunities; there is no doubt about that. It is still the most attractive investment landmark.”

According to Mr Thorneman, the capacity of the Chinese government is still reliable in most of the investors’ eyes, as we are witnessing policymakers’ attempts to consolidate a number of industries.

Meanwhile, corporations throughout the world have learned not to put all their investment eggs in the China basket. Instead, they are starting to seek more growth opportunities in Southeast Asia and other emerging markets.

“They are shifting. Instead of putting in another plant in China, they may be putting it into Indonesia or Vietnam in order to access the new markets with cheaper labour costs and also to diversify their portfolio. But China will continue to be an attractive market in the next decades,” Mr Thorneman concluded.

Likewise, China’s debt-to-GDP ratio is rising, though it still remains within the “safe” boundary if compared to the ratio in most developed economies. The Chinese government has a relatively large stock of net assets and seems to be in a solid position to manage its liabilities.

What’s more important than high-digit GDP growth is that policymakers must learn to put the country’s sustainable growth ahead of their careers. They also need to pay more attention to important issues of environmental degradation, food safety and the rising wealth gap.

In short, they should not allow the size of China’s balance sheet to blind them to concerns over the underlying structural risks, given that no economy is too big to fail.