Key Bond Index Gets Bitten; Investors Are Pulling Funds Tied to ‘the Agg’ as Safe Bonds Look Anything But

April 3, 2013 Leave a comment

Updated April 2, 2013, 9:51 p.m. ET

Key Bond Index Gets Bitten

Investors Are Pulling Funds Tied to ‘the Agg’ as Safe Bonds Look Anything But

By CAROLYN CUI And PATRICK MCGEE

The guiding star for many bond investors is starting to flicker. The Barclays BARC.LN +2.18% U.S. Aggregate Bond Index, known as “the Agg”—which tracks the broader debt market the way the Standard & Poors-500 follows stocks—declined 0.12% in the first quarter, its first negative return in that period since 2006. And with many large investors yanking funds tied to the Agg, the index’s flagging popularity is having repercussions for how hundreds of billions of dollars are allocated in fixed-income portfolios. The move is perhaps the most stark indication yet that the safest bonds are scaring investors.

A prime reason for the Agg’s changing fortunes is that U.S. Treasurys and government-backed mortgage debt have gained a larger share of the index, following several years of record U.S. debt issuance.

A prime reason for the Agg’s changing fortunes is that U.S. Treasurys and government-backed mortgage debt have gained a larger share of the index, following several years of record U.S. debt issuance.

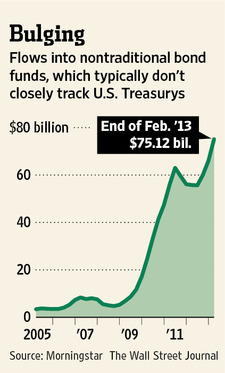

Treasurys, long the gold standard of the debt markets, have in recent years lost their allure as income-starved investors favor riskier, higher-yielding securities such as “junk” bonds and loans.

Since 1976, the Agg has posted an annualized return of 7.68%.

Though smaller than the S&P 500’s 11.24% gain over the same period, the index only had two negative calendar years during the 37-year history—in 1994 and 1999—a far more steady performance than its stock counterpart.

This year’s drop in the Agg shows investors are becoming braver gamblers, betting that gains in the labor and housing markets will finally prompt rising rates in the largest bond markets and that the Fed will reduce its debt purchases.

If that scenario comes to pass, it would be punishing for all debt investors, but particularly for those who bought more recently issued, low-yielding, high-rated bonds. Treasury bond yields are near record lows. Higher rates mean lower bond prices.

Any newly sold bonds at higher rates would be higher yielding and thus more attractive to investors.

“Simply going out and buying a U.S. Treasury is becoming a much more dangerous activity than it used to be,” said Russ Koesterich, chief investment strategist atBlackRock Inc., BLK +1.77% the world’s largest money manager. “You either take more risk, or you accept dramatically less return.”

Roughly $4 trillion is invested into strategies pegged to the Agg, which tracks high-quality U.S. bonds such as Treasurys, highly rated company debt and mortgage-backed securities.

But large investors over the past five years have pulled $171 billion away from securities that track the index, according to eVestment, a data provider on institutional investment.

The Agg’s recent decline is still small relative to the double-digit percentage plunges that investors have experienced in bad years for the stock market. Still, riskier investments have paid off this year.

Funds devoted to buying only the riskiest noninvestment-grade, or junk, bonds are up nearly 3% and the Dow Jones Industrial Average has advanced nearly 12%

If interest rates climb, bond investments linked to the Agg could be hurt, given that Treasurys now account for 37% of the index, up from 21% a decade ago.

“It makes our clients less and less interested in being benchmarked to the Agg,” says James Sarni, a managing principal at Payden & Rygel, which manages $84 billion in assets, mostly in fixed income.

The Los Angeles-based firm now has 17% of its assets tied to the index, down from about 20% in 2009, as new money is coming into the firm for other types of strategies.

Strategists at Goldman Sachs Group Inc. GS +0.44% anticipate the 10-year Treasury rate will rise from 1.85% to 2.5% by year-end, a result of U.S. economic expansion pushing investors into securities that more closely track growth rather than safer bonds, which promise a basic return.

Using Goldman’s scenario, the Agg could clock a negative 1% return by the end of 2013. If benchmark interest rates were to rise a single percentage point, the Agg would lose 5.22% in price. When bond prices fall, yields rise.

The impact could cause a big thud. Of the $663 billion of institutional assets invested in 270 U.S. core fixed-income portfolios, 75% are benchmarked against the Agg, eVestment data show. The index comprises of a total of 8,286 bonds and is worth nearly $17 trillion—more than the S&P 500, which is worth about $14 trillion.

At Delaware Investments, more clients are asking the firm to switch to a broader index, said Roger Early, chief investment officer who oversees about $130 billion in fixed-income assets. While the company still has about $25 billion tied to the Agg, the index “has become unrepresentative of what people want to invest in,” he said.

The index provider is taking note. Barclays has been developing customized indexes for clients and also rolled out new indexes to reflect changing investor demand.

Waqas Samad, head of index, portfolio and risk solutions at Barclays, acknowledged that sophisticated investors are starting to rethink their investing strategies, but said “that kind of a shift will take time.”