Billabong perilously close to a wipeout; In 25 years, the company has lost most of its street cred and its value has shrunk from billions to whatever is on offer

April 6, 2013 Leave a comment

Billabong perilously close to a wipeout

April 6, 2013, Elizabeth Knight

In 25 years, the company has lost most of its street cred and its value has shrunk from billions to whatever is on offer, writes Elizabeth Knight.

Twenty-five years ago, Billabong basked in street cred. Today, as one fashion industry insider quipped, the brand has become the barbecue short for the sausage sizzle. If the 45-year-old dads are wearing boardies with elasticised or Velcro adjustable waists to accommodate a middle-aged muffin top, their 15-year-old sons are not in the market.

On Friday, the future ownership of this Australian iconic brand hung in the balance. Two American corporate sharks have been circling the bleeding Billabong carcass for a couple of months and intense talks are continuing over the weekend.

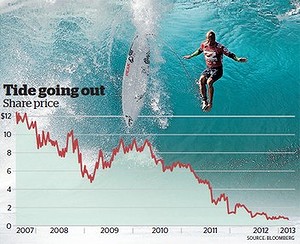

The decision by the Billabong board and its largest shareholder and founder, Gordon Merchant, to hang out the for sale sign, is the ultimate recognition the company has lost its way. Five years ago Billabong was a $5 billion company and its stock traded for $14. The prices being offered by these financial syndicates today are less than 70¢ a share – the financial equivalent of the bin out the front of the store housing the end-of-season/couldn’t-sell stock that customers rifle through. At this price the whole company is worth closer to $300 million. It is the final ignominy for the company whose financial performance has been in such steep decline that it has lost the support of many of its major investors and has been playing a dangerous game of dodgeball with its bankers.The previous management was ditched last year following a series of poor results and profit downgrades. The long-serving chairman, Ted Kunkel, hung up his boardies, as did other directors. The replacement regime, headed by former Target boss Launa Inman, devised a new corporate restructuring plan but the results to date suggest it hasn’t yet gained much traction.

Inman’s remit was not about growing the business. In a practical sense her job is more akin to managing a business that’s in runoff. She didn’t create Billabong’s problems, she inherited them, but there has been a large question mark over whether she could fix them.

Six weeks ago Billabong reported a $536 million loss for the six months to December 2012. In doing so it breached agreements with its bankers who ultimately continued their support – but at a price.

The banks took security over the assets and Billabong became their hostage. The ever-shrinking company is now so small that, says one prominent retail analyst, ”the only people interested in this stock are the ones that own it and want to get out at any price”.

For investors it’s been all about damage control. The retail recovery story is selling about as well as last season’s Billabong board shorts.

The path of Billabong’s demise is littered with poor investment decisions, strategy blunders, hubris and flat-footed management responses to structural changes in market conditions. The poor broader retail environment just exacerbated the problems.

When entrepreneurial surfer Gordon Merchant created the Billabong brand in the 1970s, it had serious credibility. In the tight and difficult-to-impress surfing circles, it passed all the tests to receive a coveted stamp of approval.

For more than 20 years it grew its popular Billabong surfwear brand – selling the must-have product primarily to small surfwear shops dotted around Australia’s vast coastline and increasingly into international markets.

It wasn’t until after 2000, when the company listed on the Australian Stock Exchange, that it started to broaden its horizons – buying new brands such as VonZipper and Element to add to its portfolio.

It was during the mid-2000s when Billabong was at its peak growth period that the seeds were sown for its ultimate corporate challenge.

The retail landscape had started to change. As one retail historian recalls, the small surf shops that made up Billabong’s retail arteries for distribution began to consolidate. Larger operators started buying up smaller shops, dividing them into massive territories. Many of the small independents that remained formed lose co-operative buying groups, covering multiple stores.

Where once the big manufacturers such as Billabong and Quiksilver had the product and could command terms, the power was shifting to the retail operators who started to dictate who the surf brands were able to sell through.

As early as 2004 Billabong had a small number of retail stores but in response to the growth in the mega retail groups, it took a massive strategic decision to dive deeply into retail to get control of the relationship with its customers.

By 2011 it had 639 stores around the world and it had morphed into a vertically integrated manufacturer and retailer of surf, skate and ski gear and various accessories.

Further complicating matters, some of the large retailers that were not bought out by Billabong were also taking the bit between their teeth and expanding into manufacturing. The market was getting messy and crowded.

Billabong’s retail strategy was being executed in tandem with the purchase of numerous new brands. During 2009 and 2010 the company had engaged in a massive spending spree, adding DaKine, Swell, RVCA, Jetty Surf, Rush, Surf Dive’n’Ski and West 49 to its arsenal.

In corporate presentations back in 2010 Billabong called this its transitional year. This is corporate-speak for undertaking major change that is yet to pay dividends. By June 2011 the management was promising the fruits of its new strategy would translate into improved earnings the following year.

But history now shows there was no harvest in 2012 and nor will there be in the 2013 financial year. The dying parts of the trees just kept getting pruned. Meanwhile, this slew of expensive debt-infused acquisitions had placed a strain on the company’s balance sheet. It was a dangerous pincer – increased interest costs and slowing cash flow.

By 2012, the company was being crushed by its debt and was in desperate need of an influx of capital. One of the few bright spots among the corporate gloom was the acquisition of watch brand Nixon. Billabong had spent $80 million on this asset and it was exceeding all expectations.

It rapidly became the jewel in its the portfolio of brands. But Billabong needed money, and offloading a near-half share in its sexiest brand, Nixon, was the easiest and quickest way to get it. The deal netted Billabong about US$285 million but several retail analysts were not supportive of the move, believing it was a short-term fix that could exacerbate the longer-term problems.

A report at the time from Merrill Lynch said, ”In our opinion Billabong has sold one of its best assets. And this is on top of a business that is already struggling to generate growth in earnings due to the underlying maturity of its wholesale business and with a considerable amount of poorly positioned retail assets.” The analysts were right in one regard. It was a short-term fix.

By June the company was again in need of money and was at risk of breaching its banking covenants. This time it appealed to its shareholders to buy new shares at a deeply discounted price in order to raise $225 million.

At the same time the company had to deliver the bad news that the full-year 2012 profit was going to be lower than had been promised only a few months earlier. Shareholders had become familiar with revised (down) profit forecasts from Billabong. It had become a chronic disappointer.

Inman’s stewardship was in its early days but even the injection of new management and the promise of a new board was not enough to cure shareholders of disappointment fatigue. In less than six months after she had started in her role she twice had to front the analyst mob and admit to profit downgrades. She had to repeat the ugly experience again a few weeks back.

For Inman it’s been a race against the clock to try to unravel most of the strategy put in place by her two predecessors over the past decade. She needs to take costs out of the business faster than the company’s revenues are declining – a frantic quest to close many of those expensive stores, reduce the number of styles, rationalise the supplier base and get rid of some sub-scale and unprofitable brands.

The bottom line is that institutional shareholders are sick of waiting. They just want to get off the Billabong train.

The decision last year by Merchant to reject a $3.30 – albeit highly conditional – offer from the private equity group TPG greatly angered other shareholders. With 15 per cent of stock, Merchant had enough power to veto this offer. And he exercised it.

He thought it was worth $5. The advisers may have been telling him this but it beggars belief that he was unable to see what was happening inside the company on which he sits as a director. Ultimately TPG came back six months later – as did another private equity group, Bain Capital. But the offer price had dropped. To get another look under Billabong’s hood both had made indicative bids of $1.45.

Within weeks Bain Capital had been frightened off by what it saw. TPG lasted three weeks longer and bailed in October. But the parade of private equity tyre kickers moved on.

It was only two months later that one of Billabong’s own executive directors, Paul Naude, teamed with a different private equity group, Sycamore Partners, to lob an even less generous indicative offer of $1.10.

By January, Billabong was also being courted by US-based leisurewear group VF Corporation and its partner Altamont Capital Partners pitching at the same price.

Naude’s team is said to have the inside running but that $1.10 ”indicative offer” turned out to be an opening bid that could have as much as halved.

The pressure on Billabong’s board to take almost any offer has been intense. To reject any offer over 50 cents carried enormous risk. The share price would plunge into free fall and no one could have predicted where it would land. Retail analysts have been changing their share price targets at a rapid rate over the past six months.

Some, such as Credit Suisse, suggest that on a worst-case scenario it was worth nothing

What started as a simple business by Merchant has become a complicated business and what was lost or forgotten in the process was the need to nurture brand. Sponsoring surfing contests and buying buff-bodied, sun-bleached surf ambassadors isn’t enough to cut it.

Regardless of who owns Billabong, the task of rebuilding an intergenerational youth brand is mammoth. And it’s even harder when the management is financially constrained and ownership clouded.

The theorists say that it’s all about staying relevant. It’s about having a clear sense of what the brand stands for – in effect, its essence. The Billabong brand is now considered to be as mature as the surfers who wore it in the 1970s.

There is a school of thought that contends the surf market has seen its better days and could be structurally shrinking.

Maybe. Or it could just be that the fad-driven, fickle youth market is not being sufficiently captivated by what’s on offer.