Beware of Index Funds That Aren’t; The new generation of investments aren’t nearly as passive— or as cheap—as you might think

April 8, 2013 Leave a comment

Updated April 7, 2013, 7:51 p.m. ET

Beware of Index Funds That Aren’t

The new generation of investments aren’t nearly as passive— or as cheap—as you might think

Index funds aren’t always what you think they are. And your innocence could cost you.

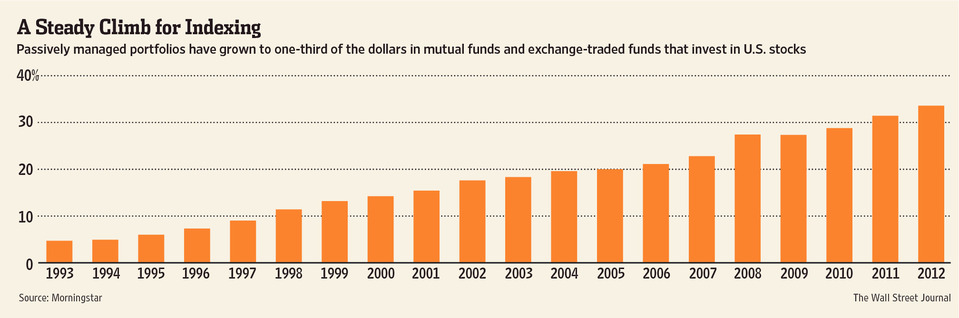

To most investors, of course, index funds are passive investments, providing returns that basically mirror the market they are designed to follow. They charge low fees and carry no hidden costs.

But the old definition is starting to change. Unlike simpler, earlier generations of index and exchange-traded funds, new variations are morphing into products that risk putting many investors afoul of the old rule about not investing in things you don’t understand.

As more money flows toward indexing, some fund firms are trying to capture a share of it by creating complex ETFs that blend active management and indexing. The fees charged by some of these funds can be several times those charged by traditional index funds. And, because they sometimes specialize in very narrowly defined, less-active markets, they can wrack up hidden trading costs.Consider one newer, complex index fund, IQ Hedge Multi-Strategy Tracker,QAI -0.01% a four-year-old ETF from IndexIQ Advisors LLC that tries to duplicate the returns of hedge-fund investments. For example, when hedge funds go “short” in a certain market, betting that prices will decline, IQ Hedge mimics that activity by taking a short position in an ETF that focuses on that market. Hedge funds follow lots of complex strategies in many different markets, however, and IQ Hedge tries to copy many of them simultaneously.

It requires considerable expertise to know how to use such an index fund effectively in a diversified portfolio. “Investors who aren’t sophisticated in sector rotation and asset allocation might be making a mistake to invest in some of these new, complex products without understanding what’s inside each fund,” says Anthony Hohmann, who oversees ETF analytical products at S&P Capital IQ, a unit of McGraw-Hill Cos.MHP +0.33%

That doesn’t mean the newer funds aren’t worth looking at. But before you buy, here are some things to consider.

1. The newer ETFs push indexing—and fees—to new levels.

One of the most popular ETFs, the 20-year-old SPDR S&P 500 SPY -0.45% fund, tracks the Standard & Poor’s 500-stock index by owning the stocks in that index. Its roughly $130 billion portfolio has few transactions—changes usually are triggered by stocks entering or leaving the S&P index. Annual turnover is under 4%, enabling sponsor State Street STT +0.70% Global Advisors to charge expenses of just 0.09% of assets each year. It’s a simple and powerful approach.

But increasingly, investors want ETFs that solve problems, such as reducing the need to rebalance, says Kevin Quigg head of global ETF sales strategy at the State Street Corp. unit. State Street responded last year by offering three actively managed ETFs, which focus on income, hedging against inflation and global asset allocation. Each spreads its dollars across a variety of narrower, mostly index-tracking ETFs.

The funds’ portfolios rebalance monthly, based on a combination of computer modeling and human oversight. But with the added complexity comes more cost: The income and the inflation-hedging funds charge 0.7% for expenses.

Traditional moderate-risk-allocation mutual funds—which may also shift portfolio positions tactically—are only modestly more costly. On average, they charge about 1% in expenses, according to Morningstar Inc. MORN -1.29%

Michael Iachini, who heads ETF research at Charles Schwab Corp.’sSCHW -1.02% investment advisory unit, says it’s important to look closely at how ETFs are designed. For instance, instead of using market capitalization as a basis for portfolio positions, some newer ETFs use other financial measures, such as revenue or dividend rates, to weight their holdings.

2. Funds that solve one problem can cause another.

PowerShares S&P 500 Low Volatility SPLV -0.17% has proved to be one of the most popular new-style ETFs, attracting $4 billion since its launch about two years ago. It’s based on the idea that stocks that gyrate less in price generally have produced good returns with less risk than the broad market. It owns the 100 stocks in the S&P 500 index with the lowest trailing 12-month volatility.

But when equities rally, as happened last year, lower-volatility stocks can trail. The fund’s net asset value rose about 10% for 2012, lagging behind the S&P 500 by about six percentage points.

By definition, a narrowly drawn product will “outperform in some environments and underperform in others,” says Francis Kinniry, a principal in the investment-strategy unit of Vanguard Group.

3. Many new ETFs miss the waves they were designed to catch.

Because many newer ETFs are designed to address issues currently on investors’ minds, timely launches can be crucial to success. Last year, about 100 ETFs were introduced, while about 100 others—a record—closed for lack of interest.

First Trust Advisors, a unit of First Trust Portfolios LP, Wheaton, Ill., has found moderate demand for its First Trust ISE Cloud Computing Index, SKYY -1.17%which focuses on the trendy business of storing and processing data on remote servers, or “cloud computing.” Launched in mid-2011, the fund has attracted about $95 million. Interest seemed to stall whenever markets went into “risk off” mode, says Ryan Issakainen, a First Trust ETF strategist.

Meantime, IQ Merger Arbitrage MNA -0.22% attracted some $30 million soon after its launch in late 2009. But assets in the fund—which uses computer modeling to gauge the odds that announced mergers will be completed—since have ebbed to less than half that amount.

Adam Patti, chief executive of IndexIQ Advisors LLC, cites the damping impact of market volatility on merger activity. Still, he says, IndexIQ views the fund as a core product and doesn’t expect to close it.

4. There can be hidden costs to go with those higher fees.

Ben Fulton, managing director of the global ETF business at the PowerShares unit ofInvesco Ltd., IVZ -1.12% says financial advisers never ask him whether the expenses his firm’s newer ETFs charge are too high, compared with those of older, passive index funds. “People are looking for investment solutions, and a cheaper product won’t do that for them,” he says.

But expenses do eat into returns. And the expense ratios shown on most fact sheets usually don’t show the total cost of owning ETFs, says Ben Johnson, director of passive-funds research at Morningstar. For example, they often don’t account for the fact that when ETFs are investing in less-actively traded markets, it may be more expensive for them to make trades, he says.

Morningstar provides an alternative way of comparing the costs of owning an ETF for the funds it tracks. On its website, it computes an “estimated holding cost,” which shows how much total return is reduced by all costs and expenses, including stated management fees.

5. Think of the new funds as garnish, not main course.

Funds with a narrow focus or specialized strategy aren’t intended to serve as core holdings in your portfolio. Instead, use them to fine-tune such things as your portfolio’s growth potential, income level or volatility, advisers say.

First Trust’s Mr. Issakainen suggests that dividend-focused investors consider owningFirst Trust Nasdaq Technology Dividend Index TDIV -0.62% along with traditional dividend strategies. Many equity-income funds tend to mostly own defensive, non-cyclical stocks, like utilities, consumer staples and health care, Mr. Issakainen says. A technology dividend fund could add balance and boost potential for dividend growth, he says.

Mr. Pollock is a writer in Ridgewood, N.J. Email him at reports@wsj.com.

The Readers Weigh In: Indexing or Active Investing?

100% indexer, with a weighted average expense ratio of 0.12% across a seven-figure portfolio.

Rob

I am 19 and invest in an S&P 500 index fund. It has been a lot of fun the past eight months to be an investor…and I’ve made 10%!

Sara Y.

Ardent proponents of index investing = knowledgeable individual investors.

Ardent proponents of “active” stock picking = financial “advisers” looking to make loads of money from not-so-knowledgeable (yet strangely overconfident) individual investors.

Army of Three

Index funds are a misnomer nowadays. Which index? If I invest in the Good Samaritan, Quasi Religious, Zombie Apocalypse index fund, does that count?

William R

100% IVV [iShares Core S&P 500 ETF IVV -0.43% ]

Lisa M