EU Sounds Alarm on Spain; Portugal to Request Extension on Bailout Loans; Momentum Seen Slipping in Madrid; Slovenia, France, Italy Also Raise Concern

April 12, 2013 Leave a comment

Updated April 10, 2013, 2:00 p.m. ET

EU Sounds Alarm on Spain

Momentum Seen Slipping in Madrid; Slovenia, France, Italy Also Raise Concern

BRUSSELS—Spain’s efforts to rein in spending and improve its economic performance are running out of steam despite much work yet to do, the European Commission warned Wednesday in a report that also singled out Slovenia as a potential trouble spot. “Spain should…maintain the reform momentum” to deal with “formidable challenges ahead,” Commissioner for Economic and Monetary Affairs Olli Rehn said after presenting an annual health check of the competitiveness of several countries in the European Union.

The report came amid reminders of the how the euro area’s protracted woes are weighing on the global economy.

Growth in the euro zone is likely to remain weak by historic standards in the coming months, the Organization for Economic Cooperation and Development said. And that weakness is a big part of why trade volumes will pick up only slightly this year from very low levels in 2012, the World Trade Organization said.

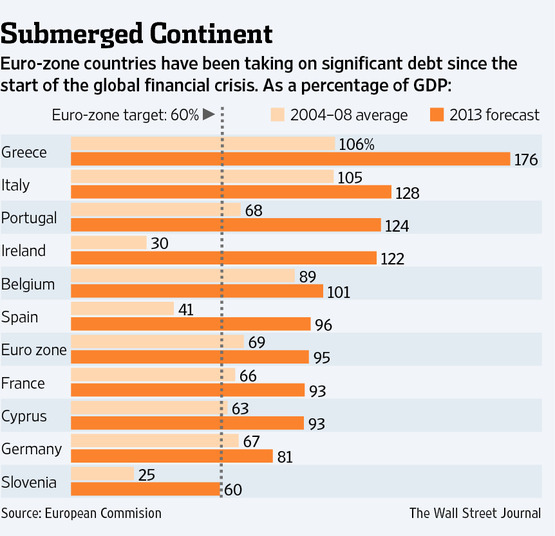

Spain is among the worst hit in Europe, with a deep recession and a jobless rate above 25%. Deleveraging and bumpy access to market financing remain a “tangible threat,” the commission report warned.

But despite years of budget cuts and a deep restructuring of the banking sector as part of a €41.3 billion ($54 billion) financial sector bailout from the euro zone, the country’s work is “incomplete,” the report said.

“Even reforms already adopted have not always displayed their full effects due to implementation lags,” the report said. “The adjustment capacity of the economy remains unsatisfactory, with much of the burden of adjustment falling on employment.”

Spanish Prime Minister Mariano Rajoy said the commission’s report relies on data from before he took office in late 2011, and said the measures that his government has enacted were already yielding “palpable results.” He promised, however, to continue with more changes.

Slovenia, a mere 0.4% of the euro-zone economy, was like Spain also cited for “excessive imbalances,” a day after Prime Minister Alenka Bratusek tried to squash rumors that Slovenia would be the sixth euro-zone member to request a bailout.

The report emphasized that the country needs to tackle the excessive corporate debtthat is putting the stability of the banking sector at risk. It said 23.7% of corporate loans are nonperforming, which means they have been in arrears for longer than three months.

“Credit is contracting and the interaction between weak banks and the sovereign has intensified,” it said. “The state has de facto become the source of capital.”

The commission warned that deleveraging in the banking sector combined with a double-dip recession are making it hard for companies to grow and are leaving troubled assets stuck on banks’ balance sheets. Slovenia’s economy shrank by 2% in 2012.

In a statement Wednesday, the finance ministry in Ljubljana said the government was “paying its utmost attention to the restructuring of the banking sector.”

The Commission’s report identified 11 other countries that need to correct imbalances, but said these weren’t “excessive.” Nevertheless, France and Italy pose systemic risks to the rest of the euro zone should their imbalances not be corrected. it said.

France, the euro zone’s second-largest economy after Germany, was losing its “resilience” to external shocks, the report said, and “its medium-term growth prospects are increasingly hampered by long-standing imbalances.”

Mr. Rehn said he would prefer to see Paris use “permanent measures” to rein in its growing public debt.

Meanwhile, Italy’s debt—estimated at 127.1% of gross domestic output in 2012 by Eurostat, the EU statistics agency—”remains a heavy burden…and is a major source of vulnerability.”

Trouble in the country’s economy, the third-largest in the euro zone, could lead to “sizable” spillovers to the rest of the currency area, the report added.

The other countries are Belgium, Bulgaria, the United Kingdom, Denmark, Sweden, Finland, Malta, Hungary and the Netherlands. Cyprus was removed from the list of EU member states suffering large imbalances because it is now in the process of completing a bailout program.

There is also much that Germany, not included in this report, can do to control its surplus, Mr. Rehn said, mentioning measures to open up its services market, increase the participation of women in the workforce and allow wages to rise with productivity.

But he said that Berlin was already taking steps in that direction and that the decline in its current-account surplus with other EU member states meant that it didn’t belong in the category of countries with substantial external imbalances.

The U.K. should move to get a grip on over-indebted, unproductive firms being kept alive by low interest rates and lender forbearance so that it can deal with risks to the stability of the financial system and boost investment in more productive firms, the report said.

The Commission has said it would factor in structural measures to tackle problems like those described in the report when considering whether to grant countries extra time to meet deficit targets. France, Spain and the Netherlands are among the countries that could need more time to reach their targets.

“Structural reforms that help to boost sustainable growth…and improve public finances are of course of substantial importance when we assess the length of time for [deficit] adjustment,” Mr. Rehn said.

Figures released Wednesday by Eurostat showed that labor costs began to fall last year in some of the countries most severely hit by the euro zone crisis, a sign that they have begun the painful process of internal devaluation that could make them more competitive.

Hourly labor costs in euro terms fell in 2012 in Greece, Spain and Portugal. They continued to rise strongly in countries including Germany, France, Austria and Finland.

But while there are some signs of progress in addressing the underlying economic weakness that led to the euro zone’s crisis, some fear that a recent easing of tension in government bond markets will lead to complacency.

“My fear is that with the financial situation being better, the securities market on the rise, policy makers tend to relax a little bit and feel that the momentum should continue, but not necessarily at the fastest pace at which it should,” Christine Lagarde, the International Monetary Fund’s managing director, said on CBS television in the U.S.

Updated April 11, 2013, 4:12 p.m. ET

Portugal to Request Extension on Bailout Loans

By ALEX MACDONALD And EAMON QUINN

DUBLIN—Portugal will ask its international creditors for an extension on the maturities of its bailout loans in order to smooth out its refinancing commitments and tap the 10-year bond markets in the future, the country’s finance minister said Thursday.

Vítor Gaspar told an audience at Dublin’s Trinity College that Portugal faces significant financing peaks over the coming years, and “that is why we are asking for a lengthening of maturities so that…we can create enough space to issue a 10-year bond successfully.”

Portugal was due to receive a €2 billion ($2.6 billion) tranche of its €78 billion bailout from the European Union, European Central Bank and International Monetary Fund this month. But the distribution has been delayed until Lisbon is able to come up with €1.3 billion in new spending cuts, after a top court in Portugal ruled last week against certain austerity measures planned for 2013.

Portuguese Prime Minister Pedro Passos Coelho hasn’t said when the government will present its new plan, which would have to be approved by the country’s parliament.

A failure to enact new cuts could push this year’s budget deficit closer to 6.3% of gross domestic product, instead of the 5.5% agreed with international lenders. Public debt would climb above the already high 124% of GDP.

Portugal has successfully implemented most of the policy actions that were set out in its adjustment program, which aims to reduce public debt and reinvigorate economic growth, Mr. Gaspar said.

The country is following the same path as Ireland in terms of adjusting its economy and regaining investor confidence, Mr. Gaspar added.

“We are trying to track Ireland as close as we possibly can,” he said.

“We need investment to pick up, we need to maintain social and political consensus, and we need to reduce public expenditure as a share of GDP in a structural and permanent way.”

Mr. Gaspar is scheduled to attend a meeting of EU finance ministers this week in Dublin, where he had been expected to get approval for extensions in some maturities of the bailout loan.

But the issue may be off the agenda for now because it would require the overall bailout program to be on track.

Still, a Portuguese government spokesman said Thursday that at the Dublin meeting, Mr. Gaspar will present guarantees that the country will fill the €1.3 billion gap, though the spokesman said the Portuguese program won’t be discussed in detail, so no new measures are expected to be presented there.

Ireland is also seeking an extension to the period over which it repays its bailout loans as it prepares to become entirely reliant on the bond markets for its financing needs from next year.

Irish Finance Minister Michael Noonan said Thursday that he is hopeful of an agreement to extend the maturities on the bailout loans to Ireland and Portugal, but the decision by Portugal’s top court may complicate matters.

European Commission Economics Commissioner Olli Rehn said Thursday in an interview that he expected euro-zone finance ministers in Dublin would agree to support Ireland and Portugal.

Mr. Rehn said he expected “a conditional decision” to support Portugal on the condition that the positive track record of implementation there continues.