Surge in Loans Puts Beijing in a Quandary; Stubborn Lending Spree Confronts Leaders With Choice of Cracking Down, and Risk Slowing Growth—or Face Crisis Later

April 12, 2013 Leave a comment

Updated April 11, 2013, 3:33 p.m. ET

Surge in Loans Puts Beijing in a Quandary

Stubborn Lending Spree Confronts Leaders With Choice of Cracking Down, and Risk Slowing Growth—or Face Crisis Later

BEIJING—A surge in lending that defied Beijing’s efforts to mop up liquidity presents China’s new leaders with the tough prospect of risking a budding growth revival by cracking down too hard to head off a bad-loan crisis.

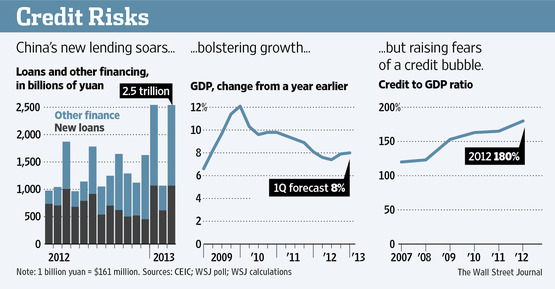

China has been on a credit binge since the global financial crisis of 2008, initially a deliberate strategy by leaders to finance investment and support economic growth. But the growing level of debt—domestic debt has topped 200% of gross domestic product, by some estimates—has prompted concerns that China faces a banking bust in the coming years. To forestall that prospect, Chinese regulators have tried to get banks and other financial institutions to somewhat dial back credit.

So far, those efforts have failed. Data Thursday showed that bank loans rose sharply in March to 1.06 trillion yuan ($171 billion) from 620 billion yuan a month earlier. A broader measure of credit that includes bonds and nonbank lending—also called total social financing—hit 2.54 trillion yuan in March, up from 1.07 trillion yuan the month before and just shy of January’s record.

“This is a reflection of the fact that China now has a much more diverse credit system” than it once did, said Charlene Chu, a Fitch Ratings Inc. senior director. “In the past, the authorities could give guidance to banks and it would be quickly followed. Now there are many other financial institutions out there” that don’t necessarily follow informal directions of the regulators.Fitch this week downgraded Chinas long-term domestic debt, saying “risks over China’s financial stability have grown.”

A high savings rate, closed capital account and robust growth mean there is no immediate trigger for a U.S.-style financial crisis. Relatively low government debt also means Beijing is well placed to backstop the banks, should problems emerge. Economists say the risk is rather that the current trajectory of credit creation is unsustainable, presenting Beijing with an unpalatable choice between slower lending and growth now, or crisis conditions a few years down the road.

The dilemma confronts China’s new leadership at a time when they both need to show firm control of the world’s No. 2 economy—and keep a recovery in growth on track.

In the short term, surging credit is tempting as it supports investment and consumption. In the past, China’s leaders—both in the central government and in the provinces—typically push growth early on in their terms as a way to prove their mettle and win allies.

China’s GDP grew 7.9% year to year in the fourth quarter of 2012, ending a six-quarter run of slowing growth. Data on GDP in the first quarter of 2013 is slated for publication Monday. The consensus forecast is for growth at about 8%.

But a rapid increase in new lending also raises concerns about inflation. “In the second half of the year they will have to tighten,” said Dariusz Kowalczyk, China economist at Crédit Agricole, who expects the People’s Bank of China to raise interest rates twice by the end of the year. Surging lending will also complicate Beijing’s quest to tame housing prices, which have begun to rise sharply again in some larger cities.

During the financial crisis of 2008-2010, China relied on heavy bank lending to churn out increases of GDP of around 10% annually while the rest of the world plunged into recession or produced wobbly recoveries. Much of the lending went into infrastructure and real estate, which boomed. But some economists argue that policy has played itself out as opportunities for productive investment diminish and firms struggle with rising debts.

Concerns that breakneck growth is unsustainable has been much on the mind of new leaders. “I don’t think China can sustain superhigh or ultrahigh-speed growth,” Chinese President Xi Jinping said this week at the Boao Forum for Asia, citing the need to balance economic growth with other priorities.

On Tuesday, Australian central banker Glenn Stevens warned China that it needs to get credit growth under control, particularly the growing segment of loans made by the informal financial sector. “China’s experience is one that others have had at various times,” Mr. Stevens said. “As long as there are incentives to bypass the formal banking sector, the shadow-banking system may keep on growing together with the risks.”

It is too early to tell whether Mr. Xi is taking measures to revamp the economy or whether provincial leaders will fall into line with a program of slower growth. Local officials are often promoted largely on their ability to increase local GDP.

Zhang Bin, a senior fellow at China’s Institute for World Economics and Politics, says he expects 2013 growth to slow to 7.5% from 7.8% in 2012—lower than the consensus estimate of about 8%. That is because each yuan of lending is producing less growth in output than it did in the past, said Mr. Zhang. He said China faces a dilemma: “short-term growth versus the possibility of financial instability.”

Underpinning part of the surge in new lending was an increase in China’s foreign-exchange reserves, also reported on Thursday. Total currency reserves rose to $3.44 trillion at the end of the first quarter, from $3.31 trillion in the prior quarter, the People’s Bank of China reported, after a year when the reserve pile showed more tepid growth. A stronger first-quarter trade surplus compared with a year earlier, and a return to inflows of capital, added to funds in China’s financial system.

Politically, the climb in foreign-exchange reserves is important because it is likely to put China’s currency practices once again on center stage internationally. China’s current-account surplus—seen as a key indicator of currency undervaluation—fell to 1.9% of GDP in 2011 from a peak of 10.1% in 2007. But a rise to 2.3% in 2012 suggests 2011 could have been the trough, with China’s trade imbalance back on a rising trend.

That could mean China comes under renewed pressure to let the value of the yuan rise markedly. This year, the People’s Bank of China has tried to keep the yuan from appreciating sharply by setting the daily value of the yuan within a relatively tight range. So far this year, the yuan has risen 0.6% against the dollar.

C. Fred Bergsten, senior fellow at the Peterson Institute of International Economics, said a substantial rise in the reserves was bound to add ammunition for U.S. lawmakers looking to penalize China for what they consider its manipulation of the currency.”If you think the Chinese current-account deficit should go to zero, then the yuan is undervalued by 15% to 20%,” Mr. Bergsten said. Many economists would consider a current-account surplus of 2.3% of GDP to be acceptable. Chinese officials have regularly said they believe the value of China’s currency is near “parity”—meaning it doesn’t need to strengthen much more or at all.