Consumer Loans Surge Across Asia; Banks From Around the World Target Middle Class With Financing for Autos, Home Appliances; debt burdens relative to individual income are up to 30% higher compared with the U.S

April 22, 2013 Leave a comment

Updated April 21, 2013, 6:38 p.m. ET

Consumer Loans Surge Across Asia

Banks From Around the World Target Middle Class With Financing for Autos, Home Appliances

By KATHY CHU

HONG KONG—Lenders from around the world are fueling a boom in short-term loans across Asia, helping push debt to record levels as a burgeoning middle class strives for a better lifestyle and banks look to diversify away from the slow-growing West.

Companies ranging from Citigroup Inc. C -0.13% to Japan’s big banks to a Dutch consumer-finance provider that built its business in Central and Eastern Europe are issuing credit cards or stepping up lending for cars, motorcycles and home appliances from India to Indonesia.

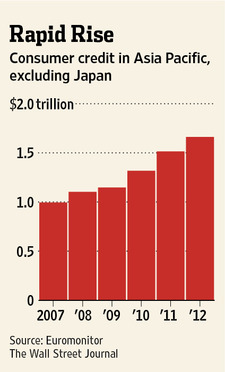

Nonmortgage consumer credit in Asia outside of Japan rose 67% in the past five years to $1.66 trillion by the end of 2012, according to data provider Euromonitor International. In the U.S. the rise was only 10% during the same period as consumers cut back on debt following the financial crisis.

The lenders are targeting Asia’s middle class, which is expected to grow by an average of more than 100 million people each year. They are pitching everything from credit cards to short-term installment loans for motorcycles and appliances. Interest rates can range from 15% for secured auto loans to as much as 40% for unsecured loans, appliances and electronics, driven by high demand for loans and little or no credit history for the borrowers. Loans are typically paid back over six months to five years.For lenders suffering from a glut of deposits, low interest rates and weak economies in the West, Asia is crucial for their growth. By 2020, more than half of the world’s middle class is expected to reside in Asia, compared with one-fourth in 2009, estimates Brookings Institution economist Homi Kharas.

Rising borrowing is expected in economies at this stage of development, and many of the companies have experience lending in markets such as these.

But some people are concerned about the growth. “The worry that’s developing is that debt is being pushed onto borrowers who might not have the capacity to repay,” says Frederic Neumann, co-head of Asian economic research for HSBC Holdings PLC.HSBA.LN +2.40%

In Jakarta, Wiwik Sugiarti lined up at a department store with half a dozen others in February to arrange financing for a $400 LG Electronics‘066570.SE +2.05% television set, months after buying a refrigerator and DVD player on credit.

“It eases my monthly budget,” says Ms. Sugiarti, 37 years old, the owner of a small grocery shop. “I can buy two or three things at the same time and not have to worry about how to pay for it now.”

In China, Citigroup Inc., which became the first Western bank to issue its own credit cards there last year, is seeing one of its fastest growth rates in credit-card accounts in the world, a bank spokesman said. The bank wouldn’t disclose details on that growth.

France’s Crédit Agricole SA ACA.FR +1.50% plans to expand its auto loans in the country by more than one-third this year to roughly 54,000 through a joint venture with local partner Guangzhou Automobile Group Co. 2238.HK +5.53% Amsterdam-based PPF Group NV’s Home Credit, which lends in places such as Belarus and Slovakia, said it is approving about 5,000 loans daily in China for mobile phones, appliances and motorcycles, more than double the number in 2011.

In Indonesia, where nonmortgage consumer credit nearly tripled in the last five years, domestic lenders Astra International ASII.JK 0.00% and PT Bank Danamon’s Adira Finance are expanding, despite tighter lending standards, while Japanese lenderMizuho Financial Group 8411.TO +0.93% has purchased an Indonesian auto-finance firm to get a foothold in the country’s fast-growing consumer-finance market.

Even in India, where defaults on personal debt rose sharply during the global financial crisis, the number of credit cards outstanding ticked up 7% to 18.9 million last year, driven in part by Western players such as Citigroup and Standard Chartered PLC.STAN.LN +0.92%

Lenders emphasized that they are being careful when they offer credit and said they were focusing on middle-class borrowers who could afford what they are buying.

Citigroup is expanding credit-card, mortgage and other consumer lending in a “disciplined manner in several high-growth markets” in Asia including China, India, Taiwan and Australia, bank spokesman James Griffiths said. In the first quarter of 2013, Citigroup’s consumer lending in Asia grew 1% year over year to $69.3 billion.

Throughout Asia outside Japan, car and motorcycle loans nearly doubled from 2007 to 2012 to a record $219.7 billion. Appliance and electronics loans also more than doubled in the region to a high of $10.9 billion, Euromonitor data show. During this time, credit-card loans grew 90% to a record $234.1 billion, according to Euromonitor.

Overall debt levels in many Asian economies are lower than in the West, but debt burdens relative to individual income are up to 30% higher compared with the U.S. in countries such as Malaysia, China, South Korea, Thailand, Indonesia and India, HSBC research shows. An added concern is that debt is a bigger burden for low-income people who have smaller financial cushions when times get tough.

Asia has a tortured history with debt. Over the past decade or so, Taiwan, South Korea and Hong Kong have all grappled with credit-card meltdowns that destabilized their economies.

Mindful of the risks, regulators in Asia are taking action. In the past year and a half, China, Malaysia and Indonesia have reined in mortgage, credit-card or motorcycle lending. Bank Indonesia Deputy Director Yunita Resmi Sari said the central bank imposed a minimum down payment for car and motorcycle loans last year to limit banks’ credit risk and to ease consumers’ debt burden.

Consumer groups in Asia, which until recently were focused on issues such as high utility bills and rising food prices, are also becoming concerned about aggressive lending and debt collection.

A leading Vietnamese provider of motorbike loans, Kuong Bank, advertises online a 1.91% monthly interest rate, equal to a more than 20% annual rate, but doesn’t explain that borrowers pay interest on the full loan amount even as the balance is paid down, says Alice Pham, director of the Hanoi chapter of Consumer Unity & Trust Society, a research and advocacy group.

Kuong Bank didn’t respond to requests for comment.