Trillion-Dollar Student Loan Bubble Cracks With Pulled Sallie Mae Bond Deal

April 29, 2013 Leave a comment

Student Loan Bubble Cracks With Pulled Sallie Mae Bond Deal

Tyler Durden on 04/29/2013 08:19 -0400

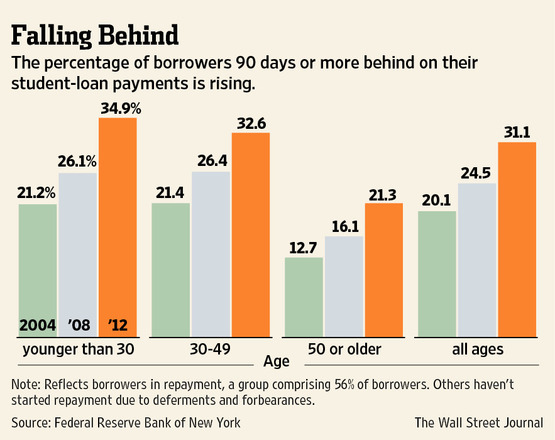

In 2007 a small number of French hedge funds imploded over sudden losses stemming from highly leveraged bets made on the unstoppable subprime mortgage market. At the time, a few saw the writing on the wall; but many simply wrote it off as just another over-levered hedge fund and the subprime mortgage market was ‘fine’. Fast forward six years and as we have discussed numerous times (most recently here and here) there is a bubble, potentially far bigger than subprime, in student loan debt. As one of the last remaining outlets for state-sanction credit creation, this is a big deal; but, of course, the popping of the bubble (or even a slight leak) is eschewed since there is so much ‘reach for yield’ and the Fed’s got your back. That is until this week. As WSJ reports, Sallie Mae (SLM), the nation’s largest non-government student lender just cancelled a $225 million debt offering as investors decided they simply were not getting paid enough for risk – amid rising student loan defaults. Simply put, there’s a limit to what investors will tolerate. SLM was offering a stunningly low 3.5% interest on the deal and investors snubbed it, “There are certain limits that can’t, or shouldn’t, be crossed if you’re an investor,” adding that, “we’re beginning to see what the tolerances are.” This is a significant shift since SLM and other issuers of debt backed by student loans sold $7.8 billion worth of securities this year through last week, up from $5.7 billion in the same period of 2012. With the portion of student borrowers who are late on their debt payments by 90 days or more climbing to 31% in 2012, from 24% in 2008; we wonder if this is the tipping point for the student debt in 2013 that was generally ignored in subprime in 2007, until it was too late.

Updated April 25, 2013, 7:23 p.m. ET

Investors Say No to Sallie Mae Bond Deal

Poor Demand for Security Backed Only by Excess Cash Flows Shows Limits to Appetite for Risk

By AL YOON

There’s a limit to how much risk investors will tolerate.

Student-loan company Sallie Mae SLM +0.24% canceled a $225 million bond offering on Thursday after about two weeks on the market, according to people familiar with the deal. The move may mark a line in the sand: Investors whose thirst for yield has revived all manner of riskier asset classes decided they weren’t getting paid enough to buy at the offered price amid rising student-loan defaults.Sallie Mae, the largest nongovernment student lender, was trying to sell the first bond of its type in more than a decade. The security is viewed as riskier than many other bonds backed by student loans because its value depends on the performance of loans already packaged in older bonds.

The yield hunt has revived the markets for securities backed by troubled mortgage loans and loans to borrowers with less than pristine credit, known as subprime. But even in these markets, there are boundaries.

“There are certain limits that can’t, or shouldn’t, be crossed if you’re an investor,” said Christopher Sullivan, chief investment officer at the United Nations Federal Credit Union. “Now we’re beginning to see what the tolerances are.”

Investors were demanding more interest than the 3.5% coupon Sallie Mae was offering on the bonds, according to people familiar with the offering. The deal was being led by Bank of America BAC +0.28% Merrill Lynch. A bank spokesman declined to comment.

Sallie Mae and other issuers of debt backed by student loans sold $7.8 billion worth of securities this year through last week, up from $5.7 billion in the same period of 2012, according to Bank of America Merrill Lynch data.

Securities backed by student loans have become popular for the extra yield they provide over safer debt, despite a significant rise in defaults on such loans. Overall, the portion of student borrowers who are late on their debt payments by 90 days or more climbed to 31% in 2012, from 24% in 2008, the Federal Reserve Bank of New York said in a recent report.

In the case of the canceled Sallie Mae offering, rising defaults could have crimped the cash flow of the federally backed loans supporting the new securities, because more defaults would mean less excess, or residual, income after holders of the original loans were paid.

What’s more, regulators and lawmakers have become concerned about growing levels of student debt, raising the risk political decisions could alter the bond market for student loans, said Jeffrey Klingelhofer, a portfolio manager at Thornburg Investment Management. For instance, a program that would allow borrowers to refinance their loans would reduce cash flow, Mr. Klingelhofer said.

“There are just too many moving parts,” he said. “Really, at the end of the day, we are not backed by an asset, and there’s a significant question of whether that cash flow would build.”

The deal’s failure didn’t affect more-traditional paths Sallie Mae has to raise funds. The lender on Thursday increased the size of a separate deal backed by its private student loans, by 33% to $1.135 billion.

The riskiest slice of that bond sold at a yield of about 3.69%, compared with the 3.48% yield on securities sold in February.

Sallie Mae’s private student loans are underwritten based on a borrower’s credit, rather than their need, which is the dominant factor when the government underwrites loans. The February deal was the first time since the financial crisis that Sallie Mae sold the subordinated portion, or riskiest slice of the security, to investors.

Delinquencies on Sallie Mae’s private student loans declined to 3.9% of loans in the first quarter, down from 4.4% in the same period a year earlier.

In addition to securitizing the excess cash flows, Sallie Mae has been selling residual interests outright. Investors have purchased them at yields in the high single digits, according to a person familiar with one of the sales.

Investors have been buying up securities backed by everything from troubled mortgages to loans to subprime borrowers looking to buy cars. Analysts expect the amount of securities backed by assets sold this year to outpace last year’s $197 billion total.