A New Era for Do-It-Yourself Investing. Many investors want to call the shots—while turning to tools and people for help as needed

May 6, 2013 Leave a comment

Updated May 3, 2013, 11:37 a.m. ET

A New Era for Do-It-Yourself Investing

Many investors want to call the shots—while turning to tools and people for help as needed

Instead of going it entirely on their own, more investors are pursuing a kind of modified DIY approach, tapping an array of increasingly sophisticated online tools and a-la-carte advice services offered by financial firms. The result is that there has been strong growth in customer assets at the mutual-fund and discount-brokerage companies that have traditionally served the do-it-yourself market, a group that includes Vanguard Group, Fidelity Investments and Charles Schwab Corp.SCHW +6.27%

Helping Hands

At Fidelity, clients approaching retirement often experiment online with the company’s Retirement Income Planner and then visit a Fidelity office to “validate” what they have found, says John Sweeney, an executive vice president at Fidelity. And an older client who is worried about leaving behind a spouse who is less financially savvy may opt to move some money into an account that Fidelity manages for them. That business is growing rapidly, Mr. Sweeney says.

Note: Based on online surveys of adults with income of at least $50,000 or more than $250,000 in investable assets. Sources: Phoenix Marketing International, Cerulli Associates.

Jim Bennett, a 65-year-old retired information-technology professional in Macedonia, Ohio, has been an avid do-it-yourselfer for decades after concluding that “nobody out there cared about my success or failure as much as I did.” Ditto for his wife, Karen, 55, a retired accountant. Still, eight years ago, the couple, who invest primarily at Vanguard, opted to have that firm prepare a financial plan for them as they looked ahead to leaving the workforce. They now update it annually, speaking by phone with one of the more than 200 certified financial planners on Vanguard’s staff.

“We have been and continue to be our own money managers,” Mr. Bennett says. But he and his wife use the service to get input and “an affirmation of what we are thinking and doing.”

Longtime do-it-yourselfers Ed and Patti Rager, Washington, D.C.-area retirees in their 60s, had an initial conversation with a Vanguard planner a few months ago. Getting a clean bill of financial health was a relief, particularly for Mr. Rager. “I could just see when we were on the phone” that he immediately felt more relaxed, Mrs. Rager says.

They might seek a follow-up chat in two or three years, Mr. Rager says, while acting on the planner’s advice to tweak their mix of stock and bond funds.

Investors who have between $50,000 and $500,000 invested at Vanguard pay $250 for a financial plan. Investors with more money at the firm get the plans free and can call the certified planners for ad hoc assistance.

“We have seen a big increase since the market downturn in 2008 in clients calling for that validation,” says Karin Risi, a principal of advice services at Vanguard, which recommends only its own funds.

Taking Back the Reins

The strength of the DIY market belies predictions that as the baby boomers inched toward a retirement funded largely by their 401(k)-plan savings, most of them would seek a one-on-one relationship with a financial adviser to manage their nest eggs. Instead, research firms say a fairly steady or even growing portion of investors—surveys put it at somewhere between one-third and two-thirds—are piloting their own financial ships.

In fact, stock-market turmoil appears to have driven some investors to the modified DIY space from the other direction. Many investors who outsourced their portfolios to professionals “were massively disillusioned by the perceived performance of their advisers” in 2008, says Ed Tracy, head of a Deloitte Consulting LLP group that provides consulting and other services to financial-services companies. Among the concerns: that advisers may not have fully understood all the products they sold and might have been influenced by their own financial interests.

Adding to investor worries: financial fraud like that perpetrated by Bernard Madoff.

Research firm Cerulli Associates has found “investors wanting to be more involved coming out of the downturn,” says analyst Roger Stamper. Investors are asking to hear more of the rationale behind advisers’ recommendations and have become more likely to bounce those suggestions off other people and do some of their own research online, according to Cerulli.

When researcher Hearts & Wallets LLC conducted focus groups with investors ages 40 to 60 last November, many participants said relying solely on an adviser “is an approach that is for ‘dinosaurs,’ ” says principal Laura Varas. “Because you can’t trust the person…you have to be involved yourself.”

Against that backdrop, there has been a “blending toward the center” in the financial-services industry in recent years, according to Ms. Varas. While firms such as Fidelity and Vanguard are offering more advice, full-service securities firms are reaching out to more do-it-yourselfers.

One example is the Merrill Edge service from Bank of America Corp.’s BAC +0.41%Bank of America Merrill Lynch unit. It offers financial-planning tools and low-cost online trading, as well as some advice services.

Such programs accommodate investors who want to work with a traditional adviser, while managing some dollars on their own at lower cost. One way to attract DIY investors, Deloitte suggested in a recent report, is for companies to position themselves as “facilitators and enablers” to those who still want to be in charge.

Money in Motion

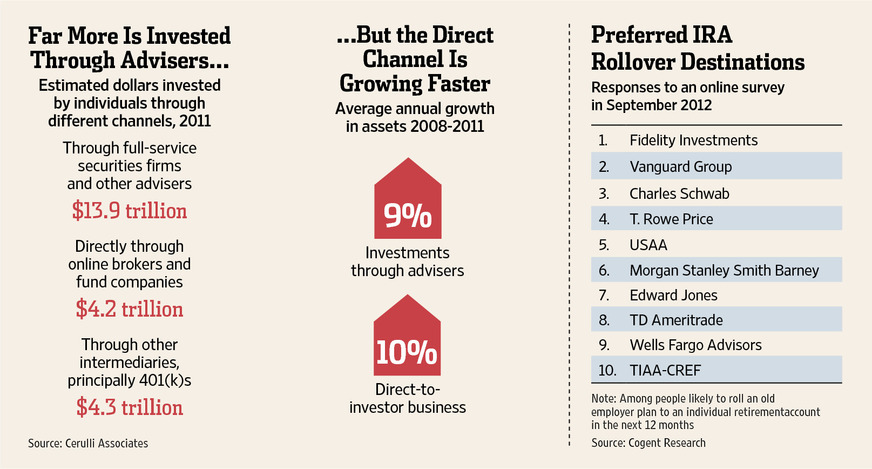

The decisions that investors make about calling the shots versus enlisting help will have huge import for financial-services companies as many retiring baby boomers roll the money in their 401(k) plans into individual retirement accounts. Those rollovers will grow to an estimated $450 billion in 2017 from around $315 billion last year, according to Cerulli, which says the financial companies that have traditionally served DIY investors have strengthened their hand in competing for rollover dollars with their expanded online tools and advice services.

Moreover, familiarity—and inertia—make it more likely that plan participants will opt for an IRA from the same firm that oversees their 401(k) plan. “That’s a big, big plus for firms like Fidelity and Vanguard that are giants in the 401(k) space,” says Antonio Ferreira, a managing director of Cogent Research LLC, which has found those two firms to be preferred destinations among consumers.

The Government Accountability Office in an April report raised concerns about 401(k)-plan providers steering participants toward the same company’s IRAs—with the participants possibly not understanding the companies’ financial interests.

When participants in a Fidelity 401(k) are leaving that employer, Fidelity “lays out all the potential scenarios they have to work with,” a Fidelity spokeswoman says. At Vanguard, a spokesman says the company “is a client-owned, at-cost enterprise, and our sole interest is giving our investors the best chance of investment success.”

Ms. Damato is a news editor for The Wall Street Journal, based in South Brunswick, N.J. Email her at karen.damato@wsj.com.

The Readers Weigh In:

Did the ’07-’09 bear market lead you to rely more or less on financial advisers?

I listen to them, however I take the final decision and directly manage my assets.

—Christophe

A financial adviser is like a real-estate agent. Always tells you to buy. When market crashed, they were not answering calls.

—Kenji

My husband and I hired a money manager for our modest but growing savings. He does not get paid for the transaction (important) but for the advice.

—Janet L

I can do better myself with E*Trade ETFC +4.03% . LOL. Don’t have anything to invest, adviser lost it all.

—Bob

I never rely on financial advisers. I listen and investigate on my own, and use reasoning and common sense.

—Guy Shannon

Relying more on my own instincts.

—David Ferrari Wilson