“All go unto one place; all are of the dust, and all turn to dust again”: Behind the hype of high-yield corporate bonds and investors’ understandable desire to make money, bad habits are creeping back in

May 7, 2013 Leave a comment

Updated May 6, 2013, 8:51 p.m. ET

Reaping Wisdom On ‘Junk’

By FRANCESCO GUERRERA

In 1977, a band of Los Angeles-based traders led by Michael Milken helped Texas International, an oil company, raise the first “junk” bond. The small issue—$30 million—opened a chapter in the history of finance. From then on, companies with less-than-pristine balance sheets were able to tap capital markets, while investors had the option of betting on securities with higher risks, and potentially higher returns, than traditional corporate bonds.

Last week, one of those traders, Leon Black, returned to L.A. and surveyed the landscape 36 years on. “The financing market is as good as we have ever seen it,” Mr. Black, now the head of the private-equity firm Apollo Global Management LLC, APO -0.34% said at a conference organized by his old boss at Drexel Burnham Lambert Inc. As declarations go, Mr. Black’s comment is to Wall Street what prime minister Harold Macmillan’s “we have never had it so good” was to Britain in 1957: a statement of fact and a bearish signal for the future. (Within years, Mr. Macmillan’s government had become deeply unpopular. By 1963, he was gone.) Facts first, worries later. Mr. Black’s comments stand to reason—with central banks keeping rates low around the world, investors crave returns from riskier assets like “junk” bonds and equities.

Last week, one of those traders, Leon Black, returned to L.A. and surveyed the landscape 36 years on. “The financing market is as good as we have ever seen it,” Mr. Black, now the head of the private-equity firm Apollo Global Management LLC, APO -0.34% said at a conference organized by his old boss at Drexel Burnham Lambert Inc. As declarations go, Mr. Black’s comment is to Wall Street what prime minister Harold Macmillan’s “we have never had it so good” was to Britain in 1957: a statement of fact and a bearish signal for the future. (Within years, Mr. Macmillan’s government had become deeply unpopular. By 1963, he was gone.) Facts first, worries later. Mr. Black’s comments stand to reason—with central banks keeping rates low around the world, investors crave returns from riskier assets like “junk” bonds and equities.

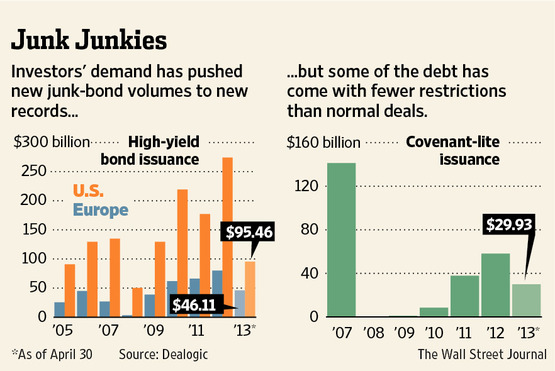

Issuance of high-yield bonds, the more polite moniker for “junk,” hit records in both the U.S. and Europe in 2012, according to Dealogic. This year has started in the same vein, with high-yield volumes rising at the fastest-ever clip. That is great news for companies such as cable television operator Charter Communications Inc.,CHTR +0.40% which just saved a bundle by selling $1 billion of bonds to replace more-expensive debt.

For investors, though, the glut of demand is beating down returns. Last week, junk bond yields, which move inversely to prices, plumbed new lows to an average of about 5.2%. If we carry on like this, we may have to change the name of the asset class to “not-so-high-yield” bonds.

Fund managers don’t care. The important number for them is the spread between returns on junk and returns on Treasuries. On that front, junk is still some 4.5 percentage points above Uncle Sam’s paper—a rich premium and well above the crazily tight spread of 2.4 percentage points seen just before the financial crisis.

The euphoria is such that Jeff Cohen, co-head of U.S. syndicated loan capital markets at Credit Suisse AG, CSGN.VX +0.52% recently told The Wall Street Journal: “Junk is a misnomer.”

I wouldn’t rush to change the name just yet. Behind the hype and investors’ understandable desire to make money, bad habits are creeping back in.

As a veteran of the 2007-2008 turmoil, I am focused on one in particular: “covenant-lite” loans. “Cov-lite” borrowers are the financial equivalent of people with commitment problems. These loans provide the borrower—usually private-equity firms or junk-rated companies—with plenty of opportunities to delay paying back the full amount.

Issuance of these loans exploded just before the crisis, as buyout firms launched ever-larger takeovers and banks engaged in a destructive race to the bottom, ceding a huge amount of power to borrowers and ending up with large losses. Cov-lites are now coming back. Last year saw the biggest issuance since 2007 and this year is on course to beat 2012.

That is worrisome, even for some users of risky paper. Ironically for a conference bearing the name of the father of junk-bond market, the Milken jamboree was overflowing with financiers expressing concern about cheap debt.

At one panel, I listened as two big-time property developers—Starwood Capital Group’s Barry Sternlicht and Equity International’s Sam Zell—were almost apologetic for how easy it is to raise money in the current environment.

Mr. Black himself sounded a gloomy note. Asked whether Apollo would take advantage of the wave of cheap capital to go on an acquisition spree, Mr. Black said that rising stock markets actually made it a great time to sell or list companies.

Rivals seem to agree. High valuations and the reluctance on the part of cash-rich corporations to dispose of assets have offset the wave of cheap money, leaving private-equity firms more willing to sell than to buy.

Last year, U.S. private-equity “exits”—sales, initial public offerings and other divestments—reached the highest level since 2007. “It’s almost biblical: There’s a time to reap and there’s a time to sow. We are harvesting now,” Mr. Black said.

For investors’ sake, let’s hope the Old Testament parallels stop there. A few verses later, the Bible reads: “All go unto one place; all are of the dust, and all turn to dust again.”