Bears Keep a Distance From Great White Short; Canada looks like a tempting target for short sellers

May 8, 2013 Leave a comment

Updated May 7, 2013, 6:54 p.m. ET

Bears Keep a Distance From Great White Short

By GREGORY ZUCKERMAN and ALISTAIR MACDONALD

Canada looks like a tempting target for short sellers. The country’s commodity-and-debt-fueled boom has slowed, and consumer debt is at records. There are concerns about a housing bubble after residential-property prices surged nearly 90% over the past decade. And some analysts smell trouble from the economy’s reliance on natural resources, as commodities prices fall and the U.S., long an importer of Canadian crude, produces more of its own oil. Despite all that, some hedge funds and other big investors are agonizing over whether to make big bets against, or sell short, Canadian investments. “I want to [short Canada] very badly,” said Vishaal Bhuyan, who runs Nariman Point, a New York hedge fund that manages more than $20 million. “But their housing bust is more slow-moving than ours was and there are no” perfect ways to bet against the Canadian housing market. The fund has held off on betting against Canadian investments.

This struggle illustrates the challenges investors face navigating the markets. Some itch to place bearish bets, arguing that economic growth in many countries has been artificially enhanced by loose central-bank policies. Still, some of these same investors have portfolios chock-full of stocks and bonds because it is hard to anticipate when troubles for the U.S. or other nations might hit.

This struggle illustrates the challenges investors face navigating the markets. Some itch to place bearish bets, arguing that economic growth in many countries has been artificially enhanced by loose central-bank policies. Still, some of these same investors have portfolios chock-full of stocks and bonds because it is hard to anticipate when troubles for the U.S. or other nations might hit.

Indeed, Mr. Bhuyan and others argue that the recent flood of money from global central banks will help Canada, along with other nations. Some also point to losses sustained by those who correctly forecast the U.S. housing bust but wagered on it too early.

Others already have been burned shorting Canada over the past few years. A short position on Canadian banks was among Toronto-based Friedberg Mercantile Group Ltd.’s four biggest losing positions in the second quarter of last year, according to a report on its website. The group, whose chief executive is Albert Friedberg, one of Canada’s highest-profile hedge-fund managers, has about $3.5 billion under management.

By the first quarter of this year the fund was still betting against Canadian banks, according to the report on its website. Mr. Friedberg didn’t respond to requests for comment. Since the start of 2012, the S&P/TSX Banks Index, which charts the performance of Canada’s largest banks, is up about 12%.

The Canadian economy has so far outperformed the most gloomy predictions. Last week, the economy posted better-than-expected gross-domestic-product growth of 0.3% for February. And while sales have fallen in red-hot property markets, prices have yet to follow suit.

Another problem: There is no index or security that is a specific bet on the Canadian housing market, making it more difficult to be a bear. Others note that government-owned Canada Mortgage and Housing Corp. insures the majority of Canadian mortgages, lending a measure of security to Canadian banks.

To be sure, more hedge funds are turning bearish. Speculative traders held a net short position on the Canadian dollar of $6.7 billion last week, according to the Commodity Futures Trading Commission’s weekly report on the commitment of traders, a larger short position than for any major currency, except the yen. The positions, which are down from an all-time high reached in mid-April, have yet to be rewarded with a major selloff. The Canadian dollar has fallen 1.2% against the U.S. dollar this year. Late Tuesday in New York, the Canadian dollar was at $0.9955, compared with $0.9932 late Monday.

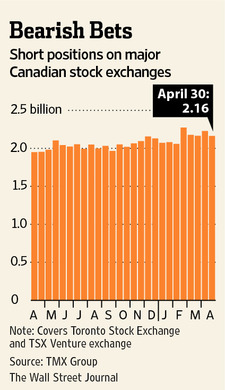

Meanwhile, short positions on Canada’s two main exchanges have risen 11% from a year earlier, a higher increase compared with the 3% rise in short positions on the New York Stock Exchange during the same period.

Bears see opportunity in what they take to be the complacent consensus view by many investors of the Canadian economy and financial sector, which weathered the financial crisis without a major bank failure and saw house prices rise.

The country is viewed on Wall Street as a “prudent nation with stringent lending standards,” said Vijai Mohan, who runs Hyphen Fund Management, which manages $11 million and is betting against Canadian bank shares and the Canadian dollar.

Mr. Mohan argues that Canadian real estate is stretched. The average house price rose to 378,532 Canadian dollars ($375,958) in March from about C$200,000 a decade earlier, according to Canadian Real Estate Association data. He has been shorting shares of financial-services company Home Capital Group Inc.,HCG.T -1.34% up 23% in the past year, and mortgage insurer Genworth MI CanadaInc., MIC.T -0.52% which is up 31% in the past year, among other Canadian shares. In a stock short sale, traders borrow shares and sell them, hoping they can buy the shares back later at a lower price and return them, pocketing the difference as profit.

Canadian household debt is about 165% of disposable income, close to the U.S. level at the height of the subprime-mortgage crisis and an increase of almost 50% in the past 10 years. In January, Moody’s Investors Service downgraded six big Canadian banks by one notch, citing their exposure to the “increasingly indebted Canadian consumer and elevated housing prices.”

The commodity slump also could bite. The Canadian central bank recently estimated that lower Canadian oil prices helped shave 0.4 percentage point from economic output in the second half of 2012, a significant impact on an economy that expanded 1.8% that year. The price of other commodities important to Canada have also fallen, with gold down 13% this year.

“There will be less demand for expensive oil from Canada as U.S. oil production grows,” said Raj Gupta, who runs Invictus RG Pte. Ltd., a $200 million Singapore-based hedge fund that has made money shorting the Canadian dollar, gold miners and Canadian energy companies this year.

The worrisome data are part of the reason Terrence Connelly of Contingent Macro Advisors LLC in Lafayette, Calif., has been recommending that his hedge-fund clients adopt bearish positions on the Canadian dollar, which has appreciated 39% against its U.S. counterpart over the past decade.

Many funds are ignoring his advice, he said.

“They worry the bubble may expand more, and many have been burned over the last two years” with positions that have lost money, Mr. Connelly said. “This is a currency that can cheapen quickly, though, so those on the sidelines may regret waiting.”