Financial Advice, Served Rare; A new wave of private firms that cater to clients’ every imaginable financial need are increasingly courting the merely wealthy

May 18, 2013 Leave a comment

Financial Advice, Served Rare

A new wave of private firms that cater to clients’ every imaginable financial need are increasingly courting the merely wealthy. Here’s what they offer.

By Julie Steinberg, Kelly Greene

You don’t have to be a Rockefeller to join a family office.

Family offices are private firms that manage just about everything for the wealthiest families: tax planning, investment management, estate planning, philanthropy, art and wine collections—even the family vacation compound.

Now many family offices are courting the merely rich.

The price of admission is still steep, and having your own personal chief financial officer doesn’t come cheap. But the help is worth considering.

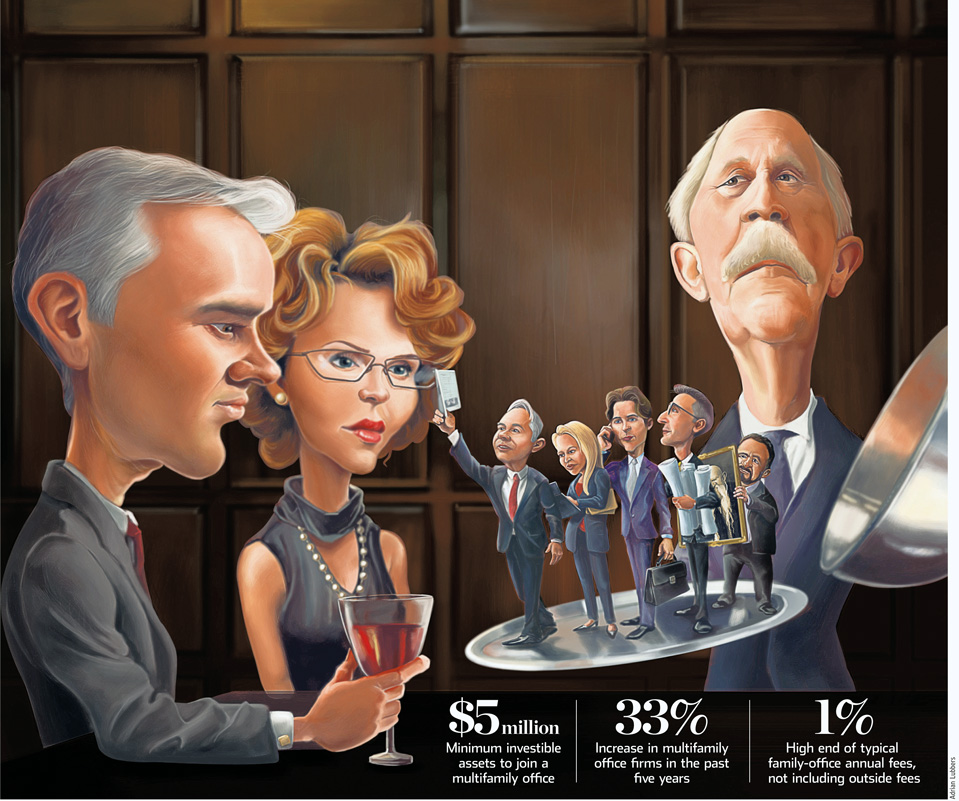

Single-family offices gained popularity in the 1800s to manage the burgeoning fortunes of tycoons such as the Rockefellers. The offices offer many of the same services as top-tier private banks and wealth managers but are devoted to a single family.The attention can cost $1 million or more per year, industry experts say, meaning family offices make financial sense mainly for families with at least $100 million in assets. There are about 5,000 such households in the U.S., according to the Family Wealth Alliance, a research and consulting firm in Wheaton, Ill, and Wealth-X, a wealth-research firm in Singapore.

By contrast, there are about 100,000 households in the U.S. with between $5 million and $10 million in investible assets, says Tom Livergood, founder and chief executive of the Family Wealth Alliance. The figure is expected to grow, he says. Entrepreneurial wealth managers are starting “multifamily” offices, which handle a handful to hundreds of families as clients.

“Even though I may have had an interest in investments, I don’t have time to think about it,” says Bernard Morrey, an emeritus orthopedics professor at the Mayo Clinic in Rochester, Minn. “You can’t be an expert in very many disparate professions.”

Dr. Morrey is a client of Abernathy Group II Family Office in New York, which grew out of a hedge fund and targets families with at least $5 million to invest. He says that working with a family office “is so important if you want to have a reasonable return on your assets. Their first role is to protect your assets, and then to grow them.”

Most multifamily offices are open to clients with at least $20 million to invest, but the average client has $40 million to $50 million, says Mr. Livergood.

Some firms are using economies of scale to make a profit from less-wealthy families. More than a third of the multifamily offices in a survey released Monday by Mr. Livergood’s firm have started marketing a specific set of services to a broader clientele. Those clients typically have $5 million to $10 million in investible assets.

Does your family qualify for a family office? Or would the sale of a business, inheritance or other windfall push you into that category?

Here’s what you need to know.

Sharing high-end wealth management services with other families can cost 0.25% to 1% of assets each year per family. There is usually a sliding scale, with families having more than $200 million in assets generally getting the lowest fees, says Carol Pepper, CEO and founder of multifamily office Pepper International in New York. Fees often include consolidated financial reports and investment management, but some firms charge more for estate planning.

For offices making overtures to those with fewer than $10 million, fees range between 0.75% and 1%, industry experts say.

On top of the basic fee, clients usually pay separate fees to outside fund managers or for any legal or accounting work done by an outside firm. Family offices will also generally accommodate any outside professionals a new client wants to keep, says Loraine Tsavaris, a managing director at Rockefeller & Co., a multifamily office in New York that also serves institutions and grew out of the original Rockefeller family office.

Clients of multifamily offices also pay less for staff salaries and other overhead by sharing the costs with other clients, says Michael Jacoby, a managing director at Deutsche Bank’s asset and wealth-management unit.

Family offices often can get the discounted fees charged to pension funds and endowments, Ms. Pepper says.

Jonathan Bergman, a managing director at TAG Associates, a multifamily office in New York with $7 billion in assets, says he negotiated a 19% decrease in the fee for clients investing in separately managed accounts.

Besides providing investment advice, family offices can provide a benefit that is tough to quantify: fostering family harmony by creating better communication among relatives. “I like that we provide an outlet for our clients where they don’t have to be the bad guy,” says Brian Luster, co-founder of Abernathy.

For example, instead of a father having to tell his son with a trust fund that he won’t get his inheritance unless he graduates from college, “we can help educate the children that this is the way the trust works, and if you don’t meet the expectations, you’re not going to get the distribution,” Mr. Luster says.

Communication is critical with these families because their wealth is so interconnected, says Stephen Campbell, managing director and head of the North America Family Office Group at Citi Private Bank, a unit of Citigroup. Communication between generations, family education and conflict resolution can help to preserve wealth, he says.

Research by Roy Williams and Vic Preisser, consultants who have studied thousands of family wealth transfers, shows that family wealth often peters out by the third generation.

But with family offices varying in so many respects, comparisons can be tricky. “If you’ve seen one family office, you’ve seen one family office,” says Evan Jehle, a principal in the family-office group at accounting firm Rothstein Kass.

Multifamily firms are proliferating, and they are grabbing more money to manage. Their numbers have increased by 33% in the past five years to more than 4,000 in the U.S., says Richard C. Wilson, chief executive of Family Offices Group, a trade group in Portland, Ore.

Assets under advisement at the 51 multifamily offices surveyed by the Family Wealth Alliance totaled $377 billion at the end of 2011, up 9.6% from a year earlier. Those assets account for three-quarters of the entire multifamily office industry, which handles some $450 billion in all.

Demand spiked for better investment advice and coordination of assets after the financial crisis, says Bob Moser, president and CEO of Laird Norton Wealth Management, a multifamily office based in Seattle with about $4 billion under management.

There has been more interest in multifamily offices from families selling their businesses. Katherine Lintz, founder of Matter Family Office, which has $3 billion in assets, says 40% of the St. Louis firm’s clients have privately owned businesses. More than half of the firm’s asset growth in the past five years has come from families who have sold all or part of their business.

The offices also are attractive because the professionals who run them often are paid by the families themselves, so there is no incentive for them to push products, says Mr. Bergman of TAG Associates. (Offices typically contract with banks and investment firms to provide deposit and trading services but aren’t paid commissions.)

Families looking for a multifamily office should make sure to find out how employees earn their money.

A family office “provides you with unadulterated risk-benefit analysis for any question you have about your assets,” says Dr. Morrey. “They don’t bother you and say, ‘We’ve got this great opportunity.’ “

If you have $5 million in assets to invest, is the expense of a family office worth it? The answer depends on what services your family wants most.

Some firms have slimmed down to the basics. Threshold Group, a multifamily office in Gig Harbor, Wash., with $3 billion in assets under management, introduced in October a service level aimed at families with $5 million to $50 million in assets to invest. Threshold had previously catered mainly to families above that level, says its president, Ed Lazar, but wanted to build relationships with clients who could potentially increase their wealth by selling a family business or investing well.

The new offering focuses on investment advice and financial planning. What isn’t included: bill paying, family-governance oversight and administrative work, which family offices traditionally provide.

But if you shop around, you might get just as much service despite your smaller net worth.

Abernathy, for example, offers family education, estate planning and lifestyle and concierge services in addition to investment management for families with as little as $5 million. Since it launched in 2011, the firm has more than doubled every year the number of families it serves, says Mr. Luster.

Other firms try to woo clients seen as likely to strike it rich down the road. “If the client has $5 million and a Harvard M.B.A. and is extremely ambitious, that’s an ideal conversation for us to have,” says Nick Delgado, chief wealth officer at Dignitas, a multifamily office in Chicago that works with 37 families worth an average of $17 million each. “We try to democratize the family-office experience.”

Setting up a family office can create access to different types of investments.

Increasingly, the wealthiest families are starting to sidestep private-equity funds to invest on their own or with other families in privately held, middle-market companies that can use the families’ know-how.

The number of family offices interested in making direct investments more than doubled to 504 last year from 224 in 2010, says John Rompon, managing partner at McNally Capital, a Chicago firm that advises families working together to make direct investments.

McNally gathers about 65 families for meetings three times a year to discuss potential investments, such as solar power and water treatment, and match up potential partners.

Tony and J.B. Pritzker, brothers in the family that once owned the Hyatt hotel chain, hired Paul Carbone last year from Baird Private Equity—the buyout and venture-capital arm of Robert W. Baird & Co.—to expand their direct-investing business, part of the Pritzker Group, their family investment firm. The brothers like being able to build businesses long-term without feeling pressure to sell, as private-equity firms often do, to generate short-term returns.

What if the family has a dispute?

One relative whose family works with Citi Private Bank’s North America Family Office Group didn’t want to have any “sin stocks,” such as tobacco- and alcohol-related investments. But the rest of the family disagreed and refused to liquidate those holdings, says group head Mr. Campbell.

The fix: breaking out the dissatisfied relative’s share of the holdings and using it to fund a “socially responsible” investment vehicle managed outside of the family office.

Ms. Pepper, of multifamily office Pepper International, suggests structuring a buyback agreement in advance that would let family members sell back shares if they are shareholders in a family operating company.

To leave the family office, an individual family member can move those investments out if those holdings are in his or her name already.

It is tougher to unwind holdings held in a trust, which are often used to shelter assets from taxes and protect assets from family members with spending or substance-abuse problems and in divorces.

When one trust beneficiary wants out of the family office and the trust has other beneficiaries who don’t, there are extra complications, says Amy Szostak, a senior vice president at Northern Trust.

Families a few million dollars shy of the cut for a multifamily office can replicate some of the experience with other wealth-management services.

Ms. Pepper suggests asking your wealth-management firm if they can provide consolidated reporting so you have a window into all of your assets and see your full asset allocation.

Also, look for a firm that will designate a financial “quarterback” to serve as the go-between with all of your advisers, including lawyers, accountants and other professionals. The quarterback needs to make sure everyone is in the loop and executing the same financial plan.

Pinnacle Wealth Planning Services, a Mansfield, Ohio, fee-only firm managing $550 million, offers quarterbacking services for clients with at least $1 million in assets. The package costs between $2,000 and $6,500 a year on top of its asset-management fee of 0.5% to 1% a year.

At Investment Financial Services in Sarasota, Fla., a wealth-management firm serving mainly families with at least $1 million in investible assets, the financial-quarterback service is included in the firm’s asset-management fee, which ranges from 0.5% to 1% a year.

“We can’t do some of the things that family offices do, but we do the nuts and bolts of a client’s wealth-management planning,” says Bill Heichel, Pinnacle’s founder. “Clients can make their own airline reservations.”