The Giant of Shareholders, Quietly Stirring; BlackRock, the world’s largest asset manager, is far from being an activist investor, but it is starting to ask more questions about companies in which it has stakes.

May 19, 2013 Leave a comment

May 18, 2013

The Giant of Shareholders, Quietly Stirring

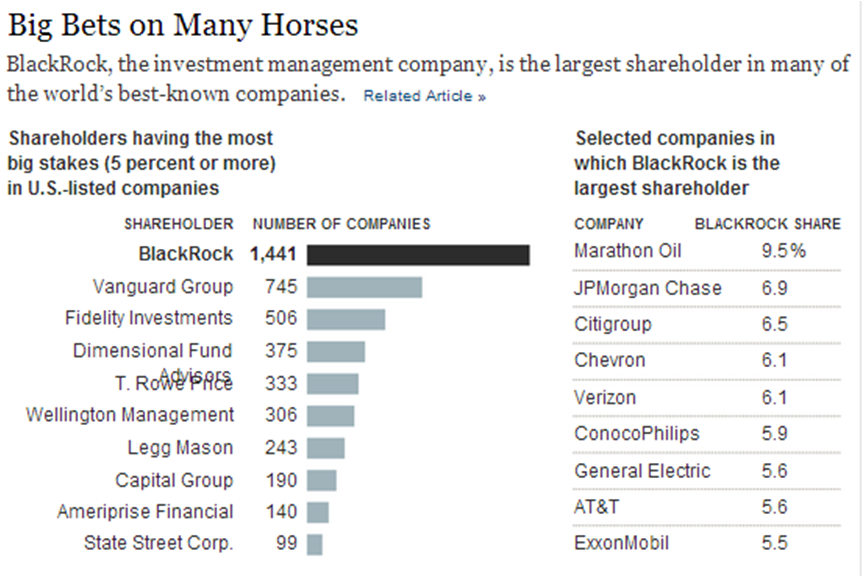

AT 11 a.m. on a Wednesday earlier this month, Michelle Edkins and her team began wheeling extra chairs into a cramped conference room in a San Francisco office tower, preparing for the corporate-governance equivalent of speed dating. Once settled, Yumi Narita started describing the disappointing qualities of a big entertainment company she’d been checking out. “I’m inclined not to trust this compensation committee,” she told the group. “Year-over-year, they pay their C.E.O. more, and the metrics are often questionable.” There were sympathetic nods around the room. Ms. Narita is one of about 20 analysts on the corporate governance team at BlackRock, the world’s largest asset manager. BlackRock’s size is mind-boggling. With almost $4 trillion under management, it is, according to a recent University of Michigan study, the single largest shareholder in one of every five United States companies. It manages money from pension funds and endowments as well as retail investors, controls large stakes in companies like JPMorgan Chase, Wal-Mart and Chevron and owns 5 percent or more of roughly 40 percent of all publicly traded companies in the country.

These investments give BlackRock tremendous influence, particularly now, during proxy season. At this time of year, public companies hold annual meetings, and shareholders vote on executive pay and elect corporate directors. Inside BlackRock, the small group of analysts led by Ms. Edkins meets every morning for about an hour, hashing out how BlackRock will vote its clients’ shares in hundreds of contests, zeroing in on directors they feel have been around too long, or ones who they think are overpaying executives.

These analysts have a language of their own, casually throwing around terms like “overboarding,” for when directors serve on multiple boards, possibly spreading themselves too thin; “engagement,” when a problem reaches a critical stage and merits a visit from a BlackRock analyst; and “refreshment,” when engagement doesn’t work and a director needs a heave-ho.

BlackRock is no activist investor. In fact, it’s far from it. It has never sponsored a shareholder proposal, and it rarely broadcasts its actions. Ms. Edkins says the firm generally votes against a director or a company proposal only when a behind-the-scenes “engagement” has failed.

A number of public pension funds and activist shareholders argue that BlackRock could use its influence to greater effect and say it sides with management far too often. It received a failing grade from the A.F.L.-C.I.O. in a 2012 survey; BlackRock voted with the federation just twice in 32 shareholder votes on issues that the union sees as important to the trustees of union pension funds.

“We believe shareholders have the power and the obligation to use every tool at their disposal to encourage greater accountability,” said Brandon Rees, acting director of the A.F.L.-C.I.O. Office of Investment. “It’s disappointing that such a large company like BlackRock votes for so few shareholder resolutions.”

There is agreement, however, that the firm has become more active in recent years, as other shareholders, too, have been expressing themselves more forcefully. It’s easy to be cynical about the value of voting on what are ultimately nonbinding resolutions that companies can ignore. But investors can now wield more power than in the past, partly because of recent laws that require companies to hold a vote on issues like executive pay. On Tuesday, in fact, shareholders of JPMorgan Chase will meet in Tampa, Fla., where the company is expected to announce the results of a the vote on an unusually tense confrontation over a motion to split the roles of chairman and C.E.O., both now held by Jamie Dimon.

BlackRock’s influence over the governance of corporations has increased as the company itself has expanded. It gained prominence during the financial crisis when Laurence D. Fink — a BlackRock co-founder and its current chief executive — became the government’s go-to guy to analyze and manage hard-to-value assets. BlackRock expanded this expertise into a separate business, advising troubled governments around the world, like Greece and Ireland. In 2009, the firm bought Barclays Global Investors in a $13.5 billion cash-and-shares deal that transformed BlackRock overnight into the world’s largest asset manager. BlackRock controls both actively managed shares, and millions more that sit in exchange-traded funds.

“BlackRock is the silent giant,” said Gerald Davis, a professor of management and organizations at the University of Michigan. He said the firm had almost no name recognition, despite managing more money than household names like Vanguard and Fidelity. “No one really knows about BlackRock but they are incredibly powerful.”

MS. EDKINS, an understated 43-year-old from New Zealand, leads BlackRock’s corporate governance effort. She got her first taste of annual reports and the corporate documents that would become her future at the University of Otago as an economics teaching assistant, where she analyzed annual reports to see which companies were disclosing their environmental impact. The experience of parsing often-dry sentences didn’t immediately turn Ms. Edkins into a corporate-governance geek. Instead, she landed a job at New Zealand’s central bank and later at the British High Commission in Wellington.

In 1997, she moved to England without a job and answered an ad in The Financial Times for a “corporate government executive” at Hermes Pensions Management. “I had to look up what corporate governance was,” she said, laughing.

Eight years later, Ms. Edkins moved to Governance for Owners, a small shareholder advisory firm in London. In an odd twist, Governance for Owners was recently charged with voting BlackRock’s shares in the proxy contest over splitting the role of chairman and chief executive at JPMorgan Chase. United States law requires BlackRock, thanks to its ties to a bank holding company, to turn over its votes to an independent third party when ownership exceeds a certain threshold. This provision is aimed at preventing any one company from having inordinate influence over the banking industry.

Ms. Edkins ended up at BlackRock in 2009, and later moved to San Francisco to lead its governance group. The way things worked in the United States, she said, came as a bit of a shock. Countries like Britain, she said, have a longer history of shareholders engaged in governance. “There is an agreed standard that has typically been developed by some commission,” she said. “Here, there is no uniform code.”

She said shareholders typically had more rights in Europe, which encourages companies to talk to shareholder groups. “In Europe it is about engagement,” she said. “Here it was, and still often is, about voting.” This, she said, leads to a more confrontational governance system in the United States.

She raised this issue at a June 2011 meeting of top BlackRock managers, including Mr. Fink. “Companies wait until the 11th hour to come to us or they assume we are going to follow I.S.S.,” Ms. Edkins says she told the group, referring to Institutional Shareholder Services, the shareholder advisory firm that recommends how shareholders should vote. “It’s frustrating.”

Mr. Fink was receptive to Ms. Edkins’s appeal. After the meeting, he wrote a letter to virtually every United States company in which BlackRock owns a stake. “Companies that focus only on gaining the support of proxy advisory firms risk forgoing valuable and necessary engagements directly with shareholders,” he wrote. “We reach our voting decisions independently of proxy advisory firms on the basis of guidelines that reflect our perspective as a fiduciary investor with responsibilities to protect the economic interests of our clients.”

The letter counted as very big news in the decorous world of corporate governance, and seemed to suggest that shareholder advisory firms, as non-shareholders, had too much influence on voting. The letter was also seen as a public declaration that companies should call BlackRock if they have a problem, and not assume that it would follow advisory firm guidance.

Just days after Mr. Fink’s letter was released, Martin Lipton and David Karp, Wall Street lawyers at Wachtell, Lipton, Rosen & Katz, wrote to their clients that “it is a helpful sign that a major institutional investor is willing to take a direct and pragmatic role in governance issues rather than outsourcing this responsibility to a proxy advisory firm or agitating for short-term results.”

MS. EDKINS oversees 20 or so people covering thousands of companies around the world, and BlackRock says they make their own decisions — regardless of the views of the firm’s portfolio managers or even Mr. Fink. During the 2012 proxy season, BlackRock voted shares on 129,814 proposals at 14,872 shareholder meetings worldwide. Almost 3,800 of those meetings were in the United States.

BlackRock analysts don’t comb through every shareholder proposal. Rather, Ms. Edkins says, the firm uses the advisory services I.S.S. and Glass, Lewis & Company to help summarize proxy statements. Once those services have identified an issue, BlackRock assigns an analyst to it.

J. Boyd Douglas, the president of CPSI, a health care provider in Mobile, Ala., said he was surprised when BlackRock withheld its vote for one of his company’s independent directors, W. Austin Mulherin, in 2012. Mr. Mulherin is a local lawyer and his firm, according to regulatory filings, annually receives “less than $120,0000” in legal fees from CPSI. This relationship called into question his independence (and earned the disapproval of I.S.S.).

After the annual meeting, CPSI arranged for Mr. Mulherin step down in 2014. “There was a delay because it’s hard to find good directors here; we are not Chicago,” Mr. Douglas said. “We needed some time.” (Mr. Mulherin did not return a call seeking comment.)

This wasn’t enough for I.S.S., and Mr. Douglas said that this year I.S.S. took a run at Mr. Douglas himself, as well as another director. Mr. Douglas immediately called BlackRock, its second-largest shareholder, asking for its support.

“We are trying and we are making changes and we don’t think it was in best interest of shareholders for Austin to come off the board immediately,” Mr. Douglas said he told a member of BlackRock’s governance team. He said the BlackRock staff member listened “respectfully” but didn’t say much. BlackRock declined to comment about CPSI, but Mr. Douglas said he and the other director that I.S.S. targeted this year were re-elected with BlackRock’s support. (The voting history of money managers like BlackRock becomes a matter of public record at the end of August.)

BlackRock has disagreed with the recommendation of the proxy advisory firms in a number of instances. For example, I.S.S. and Glass, Lewis generally support companies splitting the role of chairman and chief executive in order to create stronger, independent boards, which counterbalance management. BlackRock has rarely voted to split the role, believing that if a company has a strong lead director, there is likely no need to sever the roles.

BlackRock holds firm to certain principles when it comes to boards it sees as in need of “refreshment” — directors who have been around too long or serve on too many boards. In 2012, it voted against three directors of Coca-Cola — Ronald W. Allen, Barry Diller and Jacob Wallenberg — because each serves on more than four boards, the tipping point that suggests to BlackRock that a director is “overboarding.”

Mark Preisinger, director of corporate governance at Coca-Cola, said his company was happy with its board but knew BlackRock’s policy, so that it was no surprise when the firm voted against these directors. Despite its “no” votes, he said BlackRock was engaged with Coke on numerous topics.

BlackRock has also voted against or withheld votes from compensation committee members at companies when it thinks that they pay executives too much. Still, the A.F.L.-C.I.O. said that in 2012, the firm voted against board nominees at just 6 percent of United States companies. In contrast, the federation voted against 42 percent of all board nominees. And BlackRock almost always sides with management in “say on pay” measures.

WHILE BlackRock is more likely than not to side with management, it has been known to vote with more vocal shareholders.

In 2010, it voted against the management of the Dollar Thrifty Automotive Group, which recommended supporting a takeover by Hertz for a $51 a share. Robert Zivnuska, who runs BlackRock’s governance effort for the Americas, said a BlackRock team concluded that company was better off as a stand-alone concern. Other shareholders agreed and rejected the Hertz offer. Two years later, Dollar Thrifty was sold to Hertz for $87.50 a share, almost 60 percent higher than the 2010 offer.

“Since Ms. Edkins took over, we have seen a real change and willingness to dialogue with other investors and we hope she continues on this path,” said Dieter Waizenegger, executive director of the CtW Investment Group, which represents union pension funds.

Back in the conference room in San Francisco in May, Zachary Oleksiuk, another analyst, gave his report to the group via video conference from Princeton, N.J.. He was in charge of keeping track of Occidental Petroleum, an oil and gas exploration company based in Los Angeles, some of whose directors had served for many years and were richly rewarded. BlackRock, with a $4.6 billion stake in Occidental, is its largest shareholder.

“As you all know, Occidental has been a perennial company of concern to us,” Mr. Oleksiuk said. Just a few weeks before, he met with two key Occidental directors to voice BlackRock’s dissatisfaction. “I sent our message to them in person,” he told the group. The message was that BlackRock planned to vote against the company’s longest-serving directors and its entire compensation committee. BlackRock was certainly not the only investor objecting to the board, and a week after Mr. Oleksiuk’s meeting with Occidental, the oil company issued a statement clarifying its succession planning, hoping to quell some of the concern. It wasn’t enough.

This month, Ray Irani, the chairman and former C.E.O., stepped down from his post after failing to receive the support of a majority of investors. Whether it was BlackRock’s “engagement” or the vote, or both, one thing was clear: shareholders made a difference.