Toyota Pulls Bond Deal Due To Soaring Yields: The Japanese “VaR Shock” Feedback Loop Is Back

May 20, 2013 Leave a comment

Toyota Pulls Bond Deal Due To Soaring Yields: The Japanese “VaR Shock” Feedback Loop Is Back

Tyler Durden on 05/19/2013 12:18 -0400

Despite the eagerness of Abenomics and the new BOJ head Kuroda to have their cake and eat it too, in this case manifesting in soaring stock prices, plunging Yen, rising GDP and exports, and most importantly, flat or declining bond yields, so far they have succeeded in carrying out three of the four (assuming Japanese economic data reporting is more accurate than that of its neighbor China), as it is physically impossible for any central planner to completely overrule the laws of math, economics and physics indefinitely. In this vein, we have described on numerous occasions in the past several days the shock to the system that the massive one-way transfer out of all asset classes and into equities has engendered, and resulted in several JGB futures trading halts in an attempt to normalize a market where bond volatility has suddenly exploded. Volatility aside (and it shouldn’t be as the below section from JPM explains), the recent surge in yields higher is finally starting to take its tool on domestic bond issuers. As Bloomberg reports, already two names have pulled deals from the jittery bond market due to “soaring” borrowing costs.The first is Toyota Industries which as NHK reported, canceled the sale of JPY20 billion debt. Toyota is among Japanese firms that put off selling debt as long-term yields on government debt have risen, increasing borrowing costs, public broadcaster NHK says without citing anyone. Last week JFE Holdings announced it would delay plans to sell bonds due to market volatility. Two names down… and the 10 Year is not even north of 1%.

What happens to corporate bond funding when the one way slide that it the USDJPY continues on its way to 105, then 110, then 120, and so on, as equities explode on their way to doubling in 2013 (the NKY225 should surpass the DJIA in absolute terms in tonight’s trading session), and how will corporation raise that much needed capital to fund CapEx (if one believes Abe of course) if they can’t even handle a 10 Year that is well shy of 1%? Maybe they can all just fund their capital needs with equity going forward?

What happens to corporate bond funding when the one way slide that it the USDJPY continues on its way to 105, then 110, then 120, and so on, as equities explode on their way to doubling in 2013 (the NKY225 should surpass the DJIA in absolute terms in tonight’s trading session), and how will corporation raise that much needed capital to fund CapEx (if one believes Abe of course) if they can’t even handle a 10 Year that is well shy of 1%? Maybe they can all just fund their capital needs with equity going forward?

Perhaps, more importantly, what happens to JGB holdings as the benchmark Japanese government bond continues trading with the volatility of a 1999 pennystock, and as more and more VaR stops are hit, forcing even more holders to dump the paper out of purely technical considerations: a topic we touched upon most recently last week, and which courtesy of JPM, which looks back at exactly the same event just 10 years delayed,when in the summer of 2003 10y JGB yields tripled from 0.5% in June 2003 to 1.6%, now has a name: VaR shocks.

For those who wish to skip the punchline here it is: A 100bp interest rate shock in the JGB yield curve, would cause a loss of ¥10tr for Japan’s banks.

Oops.

For those who wish to keep reading, JPM’s Nikolaos Panigirtzoglou explains how Japan’s toxic volatility loop may very soon send JGBs soaring in yields: a perfectly logical outcome in a world that can’t have the disconnect between equity-implied growth (and inflation) and bond-implied contraction (and deflation) for ever.

And all this just as Abenomics was desperately clinging to any validation it was working.

From JPM’s Flows and Liquidity: VaR Shocks

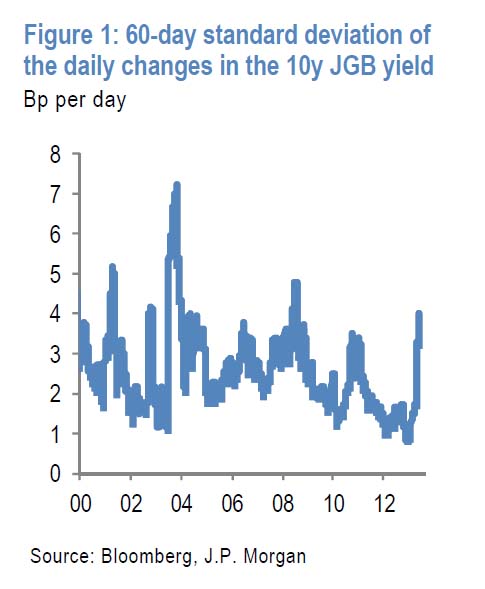

The recent rise in JGB volatility is raising concerns about a repeat of the 2003 “VaR shock” i.e. volatility-induced selloff.

The rise in JGB volatility is raising concerns about a volatility-induced selloff similar to the so called “VaR shock” of the summer of 2003. At the time, the 10y JGB yield tripled from 0.5% in June 2003 to 1.6% in September 2003. The 60-day standard deviation of the daily changes in the 10y JGB yield jumped from 2bp per day to more than 7bp per day over the same period.

As documented widely in the literature, the sharp rise in market volatility in the summer of 2003 induced Japanese banks to sell government bonds as the Value-at-Risk exceeded their limits. This volatility induced selloff became self-reinforcing until yields rose to a level that induced buying by VaR insensitive investors.

Banks typically set limits against potential losses in their trading operations by calculating Value-at-Risk metrics. Value-at-Risk (VaR) is a statistical measure that banks use to quantify the expected loss, over a specified horizon and at a certain confidence level, in normal markets. Historical return distributions and historical market volatility measures are typically used in VaR calculations given the difficulty in forecasting volatility. This in turn induces banks to raise the size of their trading positions in a low volatility environment, making them vulnerable to a subsequent volatility shock.

What was the flow evidence in the summer of 2003? By looking at quarterly Flow of Funds data from the BoJ, it was Japanese banks, Broker/Dealers and foreign investors who sold JGBs at the time. And it was VaR insensitive investors, Postal Savings and domestic Pension Funds and Insurance Companies who absorbed that selling.

How sensitive are Japanese banks currently to an interest rate volatility shock? The latest Financial System Report by the BoJ, April 2013, does not look encouraging. While Japanese major banks are close to average in terms of their vulnerability to interest rate rises, Regional and Shinkin (i.e. cooperative banks) are the most vulnerable they have ever been.

A theoretical 100bp interest rate shock, i.e. a parallel shift in the Japanese bond yield curve of 100bp, would cause a loss of ¥3tr for Major banks, ¥5tr for Regional banks and ¥2tr for Shinkin banks. As a % of Tier 1 capital, these theoretical losses are close to 35% for Regional and Shinkin banks vs. only 10% for Major banks. The maturity mismatch, the difference between the average remaining maturity of assets minus that of liabilities, has risen for all banks over the past few years. But it was the highest ever at the end of last year for Shinkin banks at 2.2 years, and the highest ever for Regional banks at1.8 years. Major banks had a much lower maturity mismatch of 0.8 years at the end of 2012.

This divergence between Major banks and Regional/Shinkin banks largely reflects differences in the maturity of their bond holdings. The average remaining maturity of bond investments has lengthened to around 4 years at Regional banks and nearly 5 years at Shinkin banks vs. 2.5 years for Major banks.

So in terms of their sensitivity to JGB interest shocks, Japanese banks appear to be more vulnerable than they were in 2003. For example in 2003, the expected theoretical loss from a 100bp interest rate shock was around ¥2tr for Major banks, ¥3tr for Regional banks and ¥1tr for Shinkin banks, significantly lower than they are currently. The maturity mismatch was around 0.8 years for Major banks, i.e. similar to the mismatch reported by the BoJ for the end of 2012. But the maturity mismatch was a lot lower at the time for Regional and Shinkin banks, at 1.2 and 1.5 years, respectively.

By themselves, these maturity mismatches and the sensitivity to interest rate shocks, appear to be increasing the chances that the Japanese government bond market will see a higher frequency of VaR shocks and thus more elevated volatility vs. other government bond markets. The potential offsetting factor is anecdotal and other evidence that Japanese banks have become more sophisticated in terms of the risk management and have gradually shifted away from mechanical Value-at Risk frameworks towards Stress Testing frameworks. This shift should have prevented banks from taking more interest rate risk in response to declining volatility and thus made them less vulnerable and less responsive to a subsequent interest rate shock.

Indeed, by looking at the risk management behavior of Major banks, for which the interest rate sensitivity and maturity mismatches are little changed since 2003, there is evidence of prudent interest rate risk management. But this is less true for Regional and Shinkin banks for which interest rate sensitivity and maturity mismatches have been rising sharply over the past years. This divergence is not surprising given that Major banks are typically a lot more sophisticated than Regional or Shinkin banks. And it is Regional and Shinkin banks which present a volatility risk for JGB markets. It is true that Regional and Shinkin banks are smaller than Major banks, but they together hold a large ¥50tr of JGBs (vs. ¥120tr of JGB holdings for Major banks).

These maturity mismatches and sensitivity to interest rate shocks have been intensified by QE because 1) of the mechanical rise in duration as yields decline and 2) because banks struggle to maintain their interest margins by extending the maturity of their bond portfolios so that they can capture extra yield. Indeed, the sharp lengthening of the maturity of the bond portfolios of Regional and Shinkin banks would appear to be a reflection of the pressure QE and a persistent low yield environment exert on banks to extend maturity. The average maturity of the bond portfolios of Regional banks was 3 years in 2007 vs. 4 years in 2012. The average maturity of the bond portfolios of Shinkin banks was 2.5 years in 2007 vs. 4.7 years in 2012.

And this is one of the unintended consequences of QE more broadly: Investors who target a stable Value-at-Risk, which is the size of their positions times volatility, tend to take larger positions as volatility collapses. The same investors are forced to cut their positions when hit by a shock, triggering selfreinforcing

volatility-induced selling. So QE potentially increases the likelihood of VaR shocks. The proliferation of risk parity investors and funds, which are strict Value-at-Risk investors and are heavily invested in bonds currently, is also likely raising the sensitivity of bond markets to sel-freinforcing volatility-induced selling.

What is the evidence of leverage outside Japanese banks? By looking at the bond holdings as % of total assets in Figure 2, Japanese banks are indeed the outlier followed by US and Euro area banks. The steady increase in the share of government bonds in Japanese bank assets reflects a sustained period of excess deposit inflows as households and corporates recycle their savings via the banking system. In a way Figure 2 suggests that Japanese banks are more vulnerable to interest rate rises and thus more likely to be the cause of a VaR shock.

Admittedly US banks feature high in Figure 2, raising concerns about their vulnerability to interest rate shocks. The problem with Figure 2 is that it does not include hedges that banks have via swap or option positions to protect themselves against duration risk. Therefore a better way to assess interest rate leverage by US banks could be to look at the quarterly trading profits of US commercial banks available from the Office of the Comptroller of the Currency (OCC). The latest observation is for Q4 2012. We proxy leverage by the ratio of the volatility of their interest-rate trading profits over bond market volatility. Figure 3 suggests that US banks’ interest-rate leverage was about average in 2012. The Dec 2012 observation is well below the highs seen in 2009/2010.