Financial innovation for once works for the investor

May 28, 2013 Leave a comment

Financial innovation for once works for the investor

Posted by: abnormalreturns, May 27th, 2013 at 4:08 pm

True, long-lasting innovations ares a rare thing in the world of finance. In my book I argue that the introduction of the ETF or exchange-traded fund was exactly that. It has taken two some decades but we are now seeing real changes in how people invest due to ETFs. I wrote:

Like all upheavals, the ETF revolution has both its benefits and its drawbacks. On the whole, ETFs have made investing easier, more diverse, and cheaper. On the other hand, the introduction of ETFs has changed the actual underlying nature of some markets, and the rapid introduction of new ETFs has diluted the benefits seen early on. Unlike many revolutions, we are not likely to see a counterrevolution unseating the ETF regime any time soon.

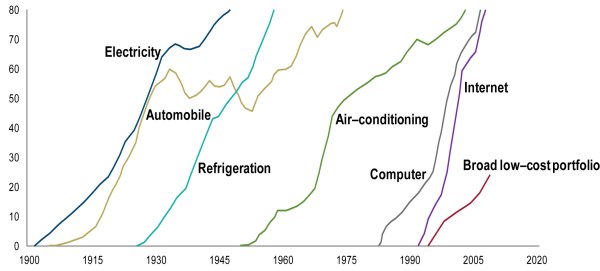

You can see how the introduction of ETFs has driven the adoption of “broadly diversified, low-cost portfolios.”Joe Davis and Andy Clarke at the Vanguard Blog compare the rise of these portfolios to other “great ideas. They write:

The adoption of great ideas typically follows an “S” curve, starting slowly, then accelerating. Eventually, the great idea becomes commonplace. The adoption of the “broad low-cost portfolio” seems to be following this pattern.

Source: Vanguard. Adapted from Visualizing Economics and The New York Times. Vanguard calculated the growth in the low-cost portfolio based on data from Morningstar, Inc. The calculation represents the percentage of U.S. mutual fund and ETF assets under management with annual expense ratios of less than 25 basis points.

They note that we are still in the “second or third” inning of this process. Of course there is a limit as to just how much of the asset management industry can (or will) shift towards this approach. To be clear the definition of these portfolios is low cost, not necessarily indexed. In any event if too much money becomes indexed there should be a resulting increase in opportunities to generate alpha.Josh Brown at the Reformed Broker notes this very point:

By the way, the ultimate irony of this rush into index products and plain vanilla beta is that excellent opportunities will be created for active managers by the competitive vacuum. Inefficiencies will once again become bountiful in the absence of people looking for them – stockpickers will find themselves alone on the beach, metal detector in hand, once again.

The point in all of this is that investors can get, at least for now, the best of both worlds. Investors who pursue broadly diversified portfolio made up with funds with rock bottom fees have the potential to generate above average returns with a relatively modest investment in time and effort. As I wrote in a prior post on the high cost of active management:

Time spent trying to find that above average active fund is time not spent in other pursuits. There will always be investors in hot pursuit of what is working now. Which is great. They are in a very real sense doing us all a favor. However for the vast majority of investors a simple, stripped down, low-cost approach to investing is in some sense the best of both worlds. It has the potential to generate above average, albeit mediocre, returns while avoiding the high implicit (and explicit) costs of active investment strategies.

This approach is above all a commitment to building simple portfolios. This is contrast to the thrust of nearly the entire money management industry which is trying to push investors into more complex products with higher fees. In a very real sense individual investors can outperform those “professional investors” who are constantly in search of the hot new manager. Morgan Housel at the Motley Fool puts it well:

3. Simple is usually better than smart

Someone who bought a low-cost S&P 500 index fund in 2003 earned a 97% return by the end of 2012. That’s great! And they didn’t need to know a thing about portfolio management, technical analysis, or suffer through a single segment of “The Lighting Round.”

Meanwhile, the average equity market neutral fancy-pants hedge fund lost 4.7% of its value over the same period, according to data from Dow Jones Credit Suisse Hedge Fund Indices. The average long-short equity hedge fund produced a 96% total return — still short of an index fund.

Investing is not like a computer: Simple and basic can be more powerful than complex and cutting-edge. And it’s not like golf: The spectators have a pretty good chance of humbling the pros.

Even though simple investing strategies have worked well over time relative to more complex ones the constant drumbeat is difficult to resist. Larry Swedroe at CBS Moneywatch recently highlighted a paper by Robert Maynard that makes this point in great detail and provides investors with the framework to rebut those who feel that a endowment-style portfolio management approach that emphasizes illiquid, opaque alternative investments is the way to go. Maynard writes:

Conventional investing has proved its worth for a number of decades, and has survived many tests. The endowment model failed its first big test, and comes with many additional problems as well. There is little reason for sophisticated institutional investors to feel compelled by the media or the anecdotal promises of its advocates to travel down that path.

The same can be said for individual investors as well. The opportunity to build a diversified portfolio are out there. Swedroe sums up the paper like this:

The bottom line is that while diversification of risks is the central tenet of prudent portfolio construction, investors can obtain all the diversification they need through publicly available vehicles. They don’t need the complexity or the high expenses of actively managed, private alternative investments to build highly diversified portfolios. By investing in publicly available funds, they maintain total transparency and have daily liquidity. This is important because the benefits of diversification are greatest when you can rebalance, which can be done only if you have liquidity.

Rebalancing is a key to this kind of uncomplicated approach to investing. However just because something is simple does not mean that it is easy. Portfolio rebalancing forces investors to sell those assets that have increased in value and buy more of those that have recently declined. This is for many a psychologically difficult exercise. Then again, a disciplined approach like this is likely to outperform one that is based on trying to jump from hot manager to hot manager.

The world of investing seems like it is becoming ever more complex. Investors can either choose to pursue complexity and with it higher costs and increasing effort. Or they can take a step back, as we often do at the beginning of the year, and choose a simple, uncomplicated approach to investing that is due to innovation has become cheaper and more freely available to investors than ever before.

Joe Davis and Andy Clarke May 22, 2013 3:40 pm

Joe Davis and Andy Clarke collaborated on this post, the result of a conversation about research that Vanguards Investment Strategy Group has conducted on the adoption and economic impact of “great ideas.”

Andy Clarke

Do you remember when you first encountered the World Wide Web? I do. It was 1993, in an office cubicle in Chicago. A colleague sat in front of her PC, scrolling through a screen of text and images. She clicked on links, opening new pages of text and images. To me, admittedly a late adopter of most technologies, it looked like magic.

When she explained what it was—a webpage for a local catering service—I had one thought: “That’s a great idea.”

I remembered this moment recently as Vanguard Chief Economist Joe Davis and I talked about his team’s research on the adoption rates of great ideas. Some ideas, such as the internet, were adopted at lightning speed. Others caught on more slowly. In the 1880s, Thomas Edison built a power plant and electrical distribution system in New York City. Not until the 1940s, however, did electric power reach 80% of U.S. households. Adoption of the automobile took even longer.

What’s the next great idea? I’m intrigued by the possibility that it’s something we’re enthusiastic about here at Vanguard: the broadly diversified, low-cost portfolio.

Joe Davis

Much like electricity, refrigeration, and other great ideas, the broadly diversified, low-cost portfolio has the potential to raise our standard of living.

Research has established that the performance of an investment program depends mostly on a few key ideas:

Asset allocation is key. A portfolio’s mix of stocks, bonds, and other assets is the primary driver of its long-term returns and the variability of those returns¹

Diversification moderates risk. Diversifying within and across asset classes reduces a portfolio’s exposure to the risks associated with a particular company, market segment, or asset class²

Higher costs mean lower returns. The lower your costs, the greater your share of an investment’s return. Over time, lower-cost portfolios have tended to outperform their higher-cost counterparts.³

The broadly diversified, low-cost portfolio, whether delivered in a single mutual fund or as a collection of stock and bond funds, capitalizes on all three of these insights. It’s, quite simply, a great idea.

The adoption of great ideas typically follows an “S” curve, starting slowly, then accelerating. Eventually, the great idea becomes commonplace. The adoption of the “broad low-cost portfolio” seems to be following this pattern.

In 1995, according to data provided by Morningstar, mutual funds and ETFs with an expense ratio of less than 25 basis points accounted for only about 5% of industry assets. Let’s call these investors the “early adopters,” Vanguard clients prominent among them. They were the first to recognize the power of the broadly diversified, low-cost portfolio.

By the end of 2012, adoption had accelerated, and portfolios with expense ratios of less than 25 basis points accounted for about 25% of industry assets.⁴ That’s progress, but investors still have a huge opportunity to lower their costs and keep more of their returns. More assets are invested in funds and ETFs with expense ratios of more than 75 basis points than in portfolios with expense ratios of less than 50 basis points.

We’re in the second or third inning of a remarkable shift toward broadly diversified, low-cost portfolios, an idea that has the power to change our lives for the better.

We would like to thank Kyle Morrison, Todd Schlanger, and Yan Zilbering for their significant contributions to this blog post.

¹ Brinson, Gary P., L. Randolph Hood, and Gilbert L. Beebower, 1986. Determinants of Portfolio Performance.Financial Analysts Journal 42(4): 39–48. [Reprinted in Financial Analysts Journal 51(1): 133–8. (50th Anniversary Issue)]

² Bennyhoff, Donald G., 2009. Did Diversification Let Us Down? Valley Forge, Pa.: The Vanguard Group.

³ Phillips, Christopher B., and Francis M. Kinniry Jr., 2010. Mutual Fund Ratings and Future Performance. Valley Forge, Pa.: The Vanguard Group.

⁴ For additional insight into the adoption of low-cost funds, see Kinniry, Francis M., Donald G. Bennyhoff, and Yan Zilbering, 2013. Costs matter: Are fund investors voting with their feet? Valley Forge, Pa.: The Vanguard Group.