China’s shadow banks: The credit kulaks

May 31, 2013 Leave a comment

China’s shadow banks: The credit kulaks

The growth in wealth-management products reflects deeper financial distortions

Jun 1st 2013 | HONG KONG |From the print edition

AS THE grandson of a “rich farmer”, a stigmatised class in communist China, Joe Zhang grew up on the wrong side of the ideological tracks. At school he envied the town-kids who could look forward to a cushy job minding grain-stores or writing propaganda. But after winning a spot at university, he eventually escaped into central banking in Beijing and, later, investment banking in Hong Kong. By pleading, petitioning and playing a lot of ping pong (a sport he hates) he was even admitted into the Communist Party in 1985.

Then, in 2011, his social climb suffered an abrupt reversal. He took on a role that remains stigmatised and discriminated against in today’s China: he became a shadow banker. His new book, “Inside China’s Shadow Banking: the Next Subprime Crisis?”, recounts his trials as the head of a microlender in Guangdong. Elsewhere in the world, microcredit is a respectable, even canonised, endeavour. In China, Mr Zhang complains in his book, it is “only slightly more respectable than perhaps massage parlours or nightclubs.”

He describes the variety of institutions and instruments that operate and innovate in the shadow of China’s mammoth banks, where they are hard for the authorities to see. They include the informal lenders, kerbside capitalists and back-alley bankers for which China is famous. But the most important institutions are China’s 67 trust companies, lightly regulated finance firms that make loans and other investments but cannot collect deposits. And the most significant instruments are the uncountable wealth-management products (WMPs), which raise money from better-off investors, in large increments (at least 50,000 yuan, about $8,160) and for short periods (typically less than six months, sometimes much less).Like banks, shadow banks are middlemen, issuing liabilities and holding assets. Another point of resemblance is that their assets are often less liquid, longer-term and riskier than their liabilities purport to be. Yet unlike banks they lack an official safety net, such as a lender of last resort, should these mismatches ever be exposed.

That makes shadow banking a bit scary. The International Monetary Fund frets that “a fast-growing share of credit is flowing through the less-well-supervised parts of the financial system.” Mr Zhang’s book is marketed to people who suspect that systemic dangers lurk in these shadows. But the tale it goes on to tell is more interesting. Shadow banking, he argues, is “more a symptom than the disease itself.”

The disease itself is financial repression. China imposes a ceiling on the interest rate that banks can pay to depositors. This keeps banks’ cost of funding low, making them eager to lend. To curb their enthusiasm, the regulators must impose offsetting limits on their lending, as Dong He and Honglin Wang of the Hong Kong Institute of Monetary Research have pointed out. These limits range from conservative loan-to-deposit ratios to heavy reserve requirements and blacklists of overexposed borrowers, such as property developers or local governments.

Where there is regulation, there is evasion, notes Mr Zhang. Much of China’s shadow-banking system serves merely to help banks evade deposit ceilings and lending guardrails. It would be less pervasive if China’s lending limits were less strict. But then those limits would not need to be so tight if banks’ funding costs were not repressed.

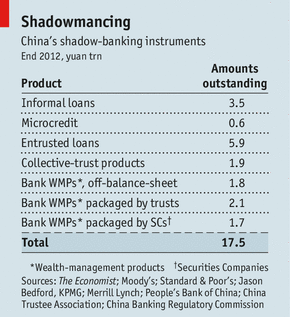

Neglected by the banks, small firms are willing to pay the 20-24% interest rates charged by China’s 6,080 microlenders. But micro-loans amounted to only 592 billion yuan ($97 billion) at the end of last year, equivalent to less than 1% of bank credit (see table). A far bigger source of finance for illiquid firms is other more liquid ones. Non-financial companies are barred from lending directly to each other, but they can make “entrusted” loans via a bank or trust company. This lending is sizeable, but also relatively safe, according to Standard & Poor’s. Most of the loans are made by big firms to their sister companies.

WMP! There it is

As well as midwifing loans from one firm to another, trust companies also raise pools of money from investors by issuing their own WMPs. These products amounted to 1.9 trillion yuan at the end of 2012. Most mature within 1-3 years, according to Jason Bedford of KPMG, an auditing firm. The money is often invested in loans to credit-starved enterprises. Some products are, however, more imaginative, speculating on tea, spirits, or even graveyards. In at least one case, a product was not just imaginative but entirely imaginary: raising money for a non-existent project dreamed up by a rogue trust-company manager.

These products are, then, risky. But potential losses are cushioned by collateral and unmagnified by leverage, Mr Bedford points out. In principle these losses are also borne by investors. The buyers of two faltering products issued by CITIC Trust, China’s largest trust company, have been told not to expect a bail-out. In practice, however, many trusts are less stiff-spined. They are tempted to rescue investors to maintain their good name.

Often, these trust products are sold through banks, which distribute them, without guaranteeing them. The public, however, “pretends not to understand the distinction”, Mr Zhang says. By feigning ignorance, aggrieved investors hope to browbeat the government into holding the banks liable, he argues. In Hong Kong banks had to ease the pain of losses on Lehman minibonds sold through their branches. It is notable that one of the banks involved, Bank of China, has been unusually reluctant to sell WMPs in the mainland, points out Mike Werner of Sanford C. Bernstein, a research firm.

Trust products sold by banks tend to be confused with a less risky kind of WMP: bank products packaged by trusts. In the first case, Mr Bedford explains, the bank provides a service to the trust companies, offering its staff and branches as a distribution channel. In the second case, the roles are reversed: trust companies and, increasingly, securities companies, provide a service to the bank, helping it to package assets in its WMPs.

Unlike trust products sold by banks, bank products packaged by trusts are fairly conservative. They are mostly “deposits in disguise”, as Standard & Poor’s put it, offering yields one or two percentage points higher than the deposit-rate ceiling. As well as helping banks to breach this ceiling, these products allow banks to window-dress their balance-sheets, points out Mr Werner. The WMPs are typically timed to mature just before the end of each quarter. As the money is returned to the WMP-buyers, it is paid into their deposits at the bank, just in time to bring the bank’s loan-deposit ratio below the regulatory limit of 75%.

If enough of the riskier WMPs fail, it might prompt investors to stop buying fresh products. Since WMPs usually mature long before the underlying assets do, that could inflict a nasty credit crunch on otherwise solvent ventures. But the impact on the banking system would be less obvious. If investors lose confidence in WMPs, they are likely to switch to deposits instead. The result would be a run to the banks, not a run on them. The only worry is that investors may not run to the same banks that issued most of the WMPs. China’s smaller joint-stock banks, which have led WMPs issuance, could therefore face a funding squeeze.

One answer would be to introduce formal deposit insurance. That would force banks to pay for the implicit backing they enjoy from the state. It would instil confidence in the smaller banks, as well as the ones that are obviously too big to fail. It would also draw a clearer distinction between safety (insured deposits) and risk (uninsured investments).

Critics of China’s shadow banking like to compare WMPs to the collateralised debt obligations at the heart of the global financial crisis. But according to Ting Lu of Merrill Lynch, the banks’ WMPs bear a closer resemblance to American money-market funds, investing mostly in safe, liquid, short-term paper. Those funds, which first arrived in America in 1971, competed successfully with bank deposits, forcing legislators to phase out America’s caps on deposit interest rates in the 1980s. Perhaps the banks’ WMPs will prove a similar spur to reform in China.

Mr Zhang is impatient for that day. He graduated from the central bank’s academy back in 1986 with a thesis entitled “The Path to Interest-Rate Liberalisation”. Then, he thought the removal of interest-rate controls was only five years away. Over a quarter of a century later, students are still writing the same thesis, he says. “Those five years have never ended.”