Is This China’s ‘Minsky Moment’?

May 31, 2013 Leave a comment

Is This China’s ‘Minsky Moment’?

Tyler Durden on 05/30/2013 22:18 -0400

China’s credit growth has been outstripping economic growth for five quarters with the corporate debt bubble looking increasingly precarious (as we explained here and here). This raises one key question: where has the money gone? As SocGen notes, although such divergence is not unprecedented, it potentially suggests a trend that gives greater cause for concern – China is approaching a Minsky moment. At the micro level, SocGen points out that a non-negligible share of the corporate sector and local government financial vehicles are struggling to cover their financial expense. At the macro level, they estimate that China’s debt servicing costs have significantly exceeded underlying economic growth. As a result, the debt snowball is getting bigger and bigger, without contributing to real activity (see CCFDs for a very big example).This is probably where most of China’s missing money went.

Via Socgen’s Wei Yao,

The missing money

In the first quarter, China’s total credit growth – bank loans, shadow banking credit and corporate bond together – accelerated to the north of 20% yoy, more than twice the pace of nominal GDP growth. This gap has been widening since early 2012.

True, the gap was once close to 30ppt in 2009 and credit growth looked like leading economic growth most of the time in the past ten years. However, we still think the recent divergence is particularly worrying.

Since 2009, China’s credit growth has outpaced nominal GDP growth in every quarter except one (Q4 11), whereas, in previous years, economic growth managed to better credit growth more than half of the time. The excess borrowing that occurred in 2009 has never been absorbed by the real economy and now more borrowing is being piled on top of this. In addition, the credit binge in 2009 was a result of the exogenous policy shock engineered by Beijing.

Authorities were quick to boost credit supply within months of the breakout of the Great Recession, long before generic credit demand from corporates picked up. However, this time, the economic slowdown as well as the credit pick-up is largely endogenous. The increase in credit demand is disproportionally larger compared to the recovery in investment appetite so far. This raises the question whether activity growth will really follow and if so by how much?

The role of shadow banking

Another big difference between the current situation and that which occurred in 2009 is the greater and increasing presence of non-bank credit. Bank loans accounted for most of the credit surge in 2009, but it is the shadow banking system and the bond market that have supported the upturn since 2012. Loan growth barely accelerated beyond 15% last year, and actually dipped somewhat entering 2013. In contrast, trust loans more than doubled in the past 12 months and corporate bonds increased by nearly 50%.

Borrowing from shadow channels like trusts are hardly a voluntary choice, as costs are often stiflingly high and duration unpleasantly short. Hence, there is an issue of adverse selection. It is those who are unable to roll over bank loans that have to tap the shadow banking system and refinance at more demanding terms. Local government financing vehicles (LGFVs) have joined this league since 2012, as the banking regulator put more and more restrictions on formal banks’ lending to them.

The ever-greater role non-bank financing has played in this credit cycle has clearly increased the vulnerability of China’s already burdened financial system.

Debt snowball

A fast rising debt load of an economy suggests either deteriorating growth efficiency or high and rising debt service cost, or in many cases both. There is clear evidence that China is suffering from both of these. We have written extensively on the point of declining growth and summarised the causes as:

excess capacity resulting from inefficient investment in the past and

increasingly marginalised private sector.

Here, we focus on the debt problem.

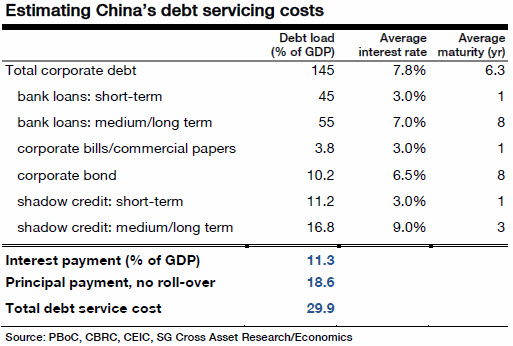

Adopting the methodology from a 2012 BIS paper, we manage to estimate China’s debt service ratio (DSR) at the macro level, and the result is very alarming.

First, taking bond, formal and shadow banking credit together, we see the debt burden of non-financial corporates and LGFVs at 145-150% of GDP as of end-2012. We consider LGFVs with other corporates because they are in pursuit of the same financing sources and increasingly face similar borrowing costs.

Second, the average interest rate and maturity are estimated at 7.8% and 6.3 years (see table below). Bear in mind that this is a fairly rough estimate, as detailed loan-level data are not easy to obtain, especially for shadow banking credit. As a general rule, we choose to adopt more lenient assumptions when information is scarcer. Therefore, maturities used in the calculation for each segment are probably longer than in reality and actual prevailing interest rates in the shadow banking system may be higher.

Third, assuming the repayment schedule of an instalment loan (i.e., a regular mortgage, for example), we then arrive at a shockingly high debt service ratio of 29.9% of GDP, of which 11.1% goes to interest payment (=7.8%×145 % of GDP) and the rest principal. At such a level, no wonder that credit growth is accelerating without contributing much to real growth!

A Minsky moment?

As a reference, the BIS paper estimated that a number of economies had similar or moderately lower debt service ratios (DSRs) when they were headed towards serious financial and economic crises. Examples include Finland (early 1990s), Korea (1997), the UK (2009), and the US (2009). This is one more data point in China that evokes the troubling thought of a hard landing.

However, we also agree that the actual DSR is probably lower. The assumption of an instalment-loan schedule implies that roll-over is not an option and all debt is fully repaid at maturity. This is clearly not the case in China. Otherwise, the 1% non-performing loan (NPL) ratio of the formal banking system would be simply impossible to explain – not to mention the zero default record kept by China’s domestic bond market or by the vast numbers of low-return infrastructure LGFVs.

Apparently, debt roll-over is not a good thing either; and, it cannot explain the increase in the debt burden. Hence, the logical conclusion has to be that a non-negligible share of the corporate sector is not able to repay either principal or interest, which qualifies as Ponzi financing in a Minsky framework. The mechanism that still holds the situation together is the state-backed formal banking system and its unspoken commitment to supporting local governments. We think this precarious equilibrium could last a bit longer but not much longer, particularly if the central government does nothing.

It is encouraging that the new leadership has so far tolerated slowing growth and largely resisted the temptation to resort to the 2009 approach. This at least has the merit of not making the problem any bigger than it already is. Furthermore, the set of new financial regulations targeting the shadow banking system and the bond market reflects the awareness of authorities of the level of financial risk. Nevertheless, we think more corporate defaults, rising NPLs, and some degree of credit crunch will still be unavoidable in the next three years, which lends weight to our below-consensus medium-term growth forecast.