Swoon in Bonds Puts Eye on Fed

May 31, 2013 Leave a comment

May 30, 2013, 8:06 p.m. ET

Swoon in Bonds Puts Eye on Fed

Investors Debate: Bubble, Confusion or Sign of Health?

By DAVID WESSEL and VICTORIA MCGRANE

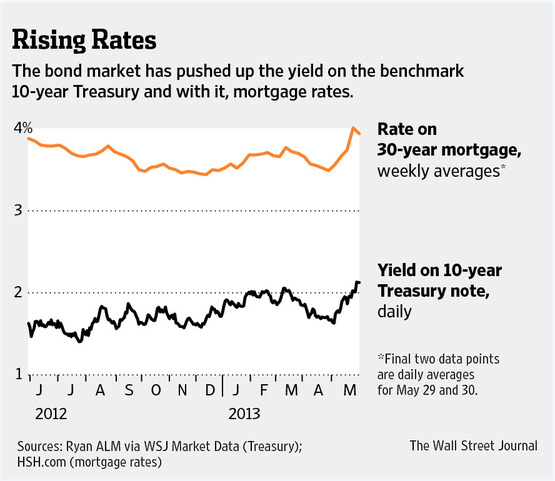

The bond market’s monthlong plunge has pushed long-term interest rates on mortgages and U.S. Treasurys to their highest levels in more than a year, sparking a debate: Is this a bursting bubble, the aftereffect of clumsy Federal Reserve communication or a welcome sign the U.S. economy is, at last, on the mend.

Yields on the benchmark 10-year U.S. Treasury note now stand above 2.1%—still low by historic standards, but nearly half a percentage point higher than at the start of May.

Rates on 30-year fixed-rate mortgages rose a hair above 4% this week, according to HSH Associates. Six months ago, they were below 3.5%.With stock prices, movements are easy to read: Up is good. Down is bad. Reading the bond market is trickier.

One camp sees the recent fall in bond prices, which move inversely to yields, as confirmation of a bond-market bubble fueled by the Fed and bound to end badly, retarding an economy whose growth is already painfully slow.

In this view, “the Treasury market is a beach ball being held under water, and the second the Fed lets go [interest rates] are going to shoot up,” said Dan Greenhaus, chief global strategist at brokerage firm BTIG LLC.

Another camp sees the same trends as a welcome move toward more normal interest rates and a signal of better times ahead. The anomaly isn’t the recent rise, but the drop in yields at the end of April to levels lower than those recorded during the Depression.

“As long as you’re seeing higher yields because of higher growth and inflation expectations, that’s undeniably a positive,” Mr. Greenhaus said.

If the bond market were signaling panic or loss of confidence in the U.S. economy, proponents of this narrative say, stock prices and the U.S. dollar would be falling, too. But since bonds turned at the start of May, the Standard & Poor’s 500-stock index has climbed 3.6% and the WSJ Dollar Index 2.3%.

While analysts argue, some already are moving money out of bond-market mutual funds, apparently figuring rates are likely to rise from here no matter what the cause, causing losses for bondholders.

In the week ended Wednesday, investors pulled nearly $880 million from mutual funds and exchange-traded funds focused on high-yield bonds, the largest weekly outflow since early February, according to Lipper.

But Lipper data show that, overall, investors are still putting money into bond funds and ETFs: $15.2 billion in May. They are putting more into stock mutual funds and ETFs, though: $22.4 billion.

Few doubt that over the next several years, long-term rates will rise closer to the 4% or 5% level if the economy continues its gradual recovery. The question is when.

Bill Gross, co-chief investment officer of bond giant Pimco, declared on Twitter three weeks ago: “The secular 30-yr bull market in bonds likely ended 4/29/2013.”

The Fed is clearly a big factor. After cutting short-term rates nearly to zero in late 2008, it began buying longer-term debt in a successful effort to pull down long-term rates and encourage investors to move into riskier assets. It is currently printing $85 billion a month to buy long-term Treasurys and mortgage-backed debt.

The Fed has been specific about short-term rates: Barring an outbreak of inflation, it will keep them very low as long as unemployment, now 7.5%, is above 6.5%.

But the Fed has been vague about the fate and rate of its bond buying, saying it will keep buying “until the outlook for the labor market has improved substantially in a context of price stability.”

Markets, hungry for more certainty, tend to overinterpret each adverb Fed officials use. Investors and traders had been anticipating the Fed would stop buying bonds in the first quarter of 2014.

Comments last week from Chairman Ben Bernanke and the release of the minutes of the last Fed policy meeting led some to think that day might come sooner. In anticipation, some investors sold bonds.

“We are trying to make an assessment of whether or not we have seen real and sustainable progress in the labor-market outlook,” Mr. Bernanke told Congress last week. Answering a question, he said the Fed could decide to scale back bond-buying in one of its “next few meetings.”

“The Fed has been clumsy because it is struggling to come to terms with the uncharted territory of these markets, and there is no unified opinion among its members as to the appropriate exit strategy,” said Adrian Miller, a fixed-income strategist at securities dealer GMP Securities LLC.

The recent spike in rates conjured up fears of a bursting bubble in bonds, a rapid and disruptive increase in interest rates that would produce big losses for individuals and institutions with big bond portfolios and raise borrowing costs across the economy. There were more than a few references this week to 1994, when Alan Greenspan’s Fed raised short-term rates after a long hiatus, bond markets around the world tanked and Orange County, Calif., ended up in bankruptcy court.

But the Fed remembers that, too. Fed officials stress almost daily that they won’t move abruptly and they aren’t going to move unless most policy makers are confident the economy really is doing better.

“We are not sitting in Jan 1994 about to get hit with the first rate hike,” David Zervos of investment bank Jefferies wrote clients Thursday. “We still have a long road to recovery and there will be fits and starts. But most importantly, we are not dealing with a Volcker or early 90s Greenspan Fed here,” both of whom raised interest rates aggressively at times.

“This is the Ben and Janet show!” he wrote, referring to Mr. Bernanke and Vice Chairwoman Janet Yellen. “These guys have long advertised a policy of not removing accommodation too quickly.”

The past several days in the bond market have been “a little jarring,” Michael Feroli ofJ.P. Morgan Chase JPM +1.74% & Co. said. “But if the markets can settle down here for a few days, I think the damage won’t be all that great. We’re still not talking about rates that would choke off the recovery.”

The recent volatility is likely to prompt Fed officials to reinforce their caution and clarify their thinking in order to calm markets as much as they can.