A misleading model: Low bond yields have in the past been bad, not good, for equity returns

August 7, 2013 Leave a comment

A misleading model: Low bond yields have in the past been bad, not good, for equity returns

Aug 3rd 2013 |From the print edition

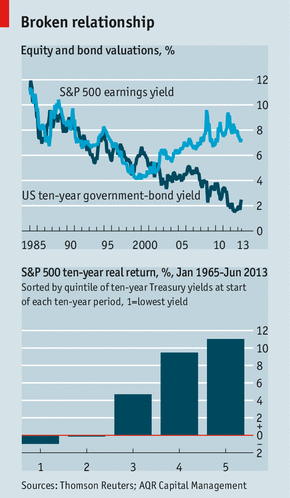

BULLS tend to find all sorts of reasons for forecasting a higher stockmarket. This is especially true of investment-bank strategists, whose bonuses are likely to get bigger when share prices are rising. Low bond yields are often seized on by equity bulls. A recent research note from Deutsche Bank, for example, suggested there was a straight trade-off between changes in bond yields and the valuation of shares, in the form of the price-earnings ratio or “multiple”. Lower bond yields mean a higher multiple; based on current yields, shares are cheap. It is all remarkably reminiscent of the so-called “Fed model”, much loved by bulls in the 1990s. The model was based on a reference in Alan Greenspan’s 1997 congressional testimony to the close relationship between the ten-year bond yield and the earnings yield (the inverse of the price-earnings ratio) on the S&P 500 index. If the earnings yield was higher than the bond yield, then equities were cheap. Bond yields and earnings yields did indeed seem to move in tandem for about 15 years, and then the relationship broke down completely at around the turn of the century (see top chart). Read more of this post