or Banks, the Chinese ‘Princeling’ Stock Has Fallen; Drought in IPO Market Curbs Need for Elite Connections

August 23, 2013 Leave a comment

August 22, 2013, 11:46 a.m. ET

For Banks, the Chinese ‘Princeling’ Stock Has Fallen

Drought in IPO Market Curbs Need for Elite Connections

WEI GU

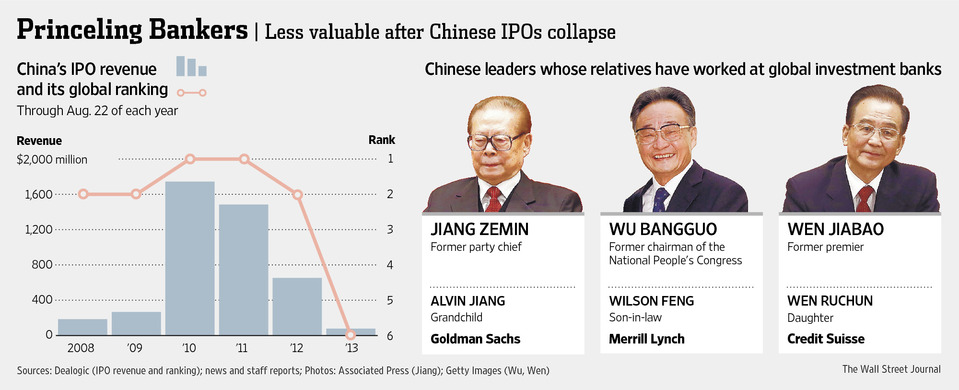

The great irony of the U.S. government’s investigation into the hiring of Chinese princelings by J.P. Morgan Chase JPM +1.12% & Co. is that right now, the children of China’s elite aren’t that valuable to the big investment banks. China’s state-owned companies, where the princelings could help the most, are far less important to the banks than they were when there was a steady parade of multibillion-dollar initial public offerings. Recently, China has suffered an IPO drought.IPO fees paid by Chinese companies tumbled to $77 million so far this year, from $652 million in the same period of 2012, and $1.7 billion in 2010, according to Dealogic.

“The market has moved from big-cap IPOs to midcap listings, bonds, and M&A,” said Tjun Tang, a senior partner and managing director at Boston Consulting. “The way you source your transactions is different now.”

The next big IPO expected out of China—Alibaba Group—illustrates the shift. Although China Investment Corp., the nation’s sovereign-wealth fund, has a small stake in the company, the person who has the most control over the likely offering is Alibaba’s founder, Jack Ma. In fact, when the company in 2007 listed a unit, Alibaba.com, one of the people who help Goldman Sachs Group Inc. GS +1.46% win the deal was Mr. Ma’s private banker.

“Now it is more about relationships with the entrepreneurs; people who do well are those with broader networks,” said Mr. Tang. “It is not that you can hire one banker who can bring you all the relationships you need.”

Now, the more-valuable bankers—rather than the children of a Chinese leader—are those who are well connected outside China. As Chinese companies prowl the world for acquisitions, those who can introduce them to hot companies for sale, or can help them get foreign-government approvals, are going to get the deals.

Even if Chinese IPOs rebound, the business has become much less profitable. In 2012, a record 17 underwriters split the $88 million fees from People’s Insurance Co. (Group) of China Ltd.’s $3.6 billion Hong Kong IPO. By comparison, in 2010, only seven banks had to share the $140 million in fees from the $10.4 billion Agricultural Bank of China raised in Hong Kong.

Another change in the China IPO market is the rising power of investors, who no longer rush to buy the latest Chinese offerings. As a result, the most valuable connections are those with hedge funds and private-banking clients, which could be big buyers in an IPO. Banks are often compensated according to how many shares they sell, said bankers. That is why banks have hired a few high-profile China economists in the past few years, hoping to leverage their credibility among investors.

A few senior bankers complained that they can’t find people with the connections powerful enough to single-handedly bring in big deals anymore. There are more stakeholders, such as regulators, the corporate parents of firms that are listing, and officials at higher levels, so just hiring the child of the chairman of a state-owned companies isn’t going to guarantee anything. A new generation of government leaders also means there are more people with ties to the government, further diluting the value of connections.

Probably because of the lower rate of return after the financial crisis, as well as the increased reputational costs for both the banks and officials, many princeling rainmakers are moving on. Wilson Feng, son-in-law of Wu Bangguo, the former chairman of the National People’s Congress, rocketed to be the vice chairman of Merrill Lynch’s China investment-banking team, where he helped land the $19 billion IPO of Industrial and Commercial Bank of China in 2006. Mr. Feng left in 2009 to find a job in the state-owned sector.

Banks are also become increasingly wary of the risks of people with powerful connections. While some bankers from privileged backgrounds are just as qualified and motivated as others, some don’t show up to work, know nothing about corporate finance, speak little English and are there simply because they are related to somebody.

“Many banks have this problem—how to deal with these people?” said the China head of a major investment bank. “Some are getting smarter about using their performances to push them out.”