Rolling returns to assess fund performance

August 29, 2013 Leave a comment

Tom Brakke

Morningstar published an article on rolling returns that included this graphic:

It shows the percentage of time the three-year trailing returns for six funds spent in each quartile of their respective categories. (This is monthly for ten years, so 120 observations.) By chance, I had just read this from Howard Marks, I believe from 1990: “I feel strongly that attempting to achieve a superior long term record by stringing together a run of top-decile years is unlikely to succeed. Rather, striving to do a little better than average every year — and through discipline to have highly superior relative results in bad times — is: less likely to produce extreme volatility, less likely to produce huge losses which can’t be recouped and, most importantly, more likely to work (given the fact that all of us are only human).”When I worked for a large asset management firm, portfolio managers were compensated based upon performance versus an index and versus a competitive group of twenty funds. Bonus calculations were determined by what quartile you were in for the year within your competitive group, but there were multipliers that kicked in based upon which quartile you were in for longer periods of time, up to five years.

You naturally paid attention to the pattern of returns generated by each manager at the firm. For example, there were two large and successful growth funds, but the managers couldn’t have been more different. One bought and held quality companies, very often from the IPO. He would almost always be at the very top or very bottom for any short period of time, but was ensconced in the top quartile for longer periods.

The other manager was always trying to be in the top quartile — and was not shy about getting a little less growthy to get there. He also had a good long term record, but arrived there in a completely different fashion than the other manager. Understanding how the managers thought about incentives and their competitive rankings was extremely important in figuring out whether and how to invest with them.

Another manager, of a fixed income fund, epitomized the philosophy that Marks outlined. For shorter time periods, he was without fail in the second quartile, which put him firmly in the first quartile over any longer period of time.

Using rolling returns as Morningstar suggests is a good way to sort managers, but look at year-by-year rankings too, since that is key to the compensation structure for most managers. Should you have the analytical tools, it also helps to see how managers do in different types of market environments.

The bottom line: You’ll often learn more about the nature of a manager’s returns by looking in new ways at how he or she created them.

On a Roll

By Michael Herbst | 08-26-13 | 06:00 AM | Email Article

Morningstar analysts look at a variety of factors when assessing a fund’s performances as part of the Analyst Rating process, including rolling returns. To assess rolling returns, start with the trailing decade or a manager’s tenure on the fund. Then look at performance over rolling periods during that stretch. For instance, to look at rolling three-year periods over the trailing decade through May 2013, start with performance over the three-year period from June 2003 through May 2006, then July 2003 through June 2006, and so on through May 2013.

Rolling returns can show how consistently a fund has performed relative to its benchmark or category rivals. They also help investors understand a fund’s risk/ reward profile. Has a fund’s performance zigzagged between its category’s top and bottom quartiles, and if so, why? If its rolling returns land near the category average, is that pattern due to its strategy or is it a sign of merely average execution? When used with risk-adjusted performance measures such as the Morningstar Rating for funds, rolling returns help inform what investors could reasonably expect from a fund’s performance pattern going forward.

It’s helpful to look at other rolling periods, too. A fund with 20% annual turnover indicates an average holding period of five years, so looking at five-year rolling periods might be more appropriate. Looking at 10-year periods can give a better sense of what to expect from deeply contrarian managers. This article walks through several world-stock fund examples.

Let’s Get Rolling

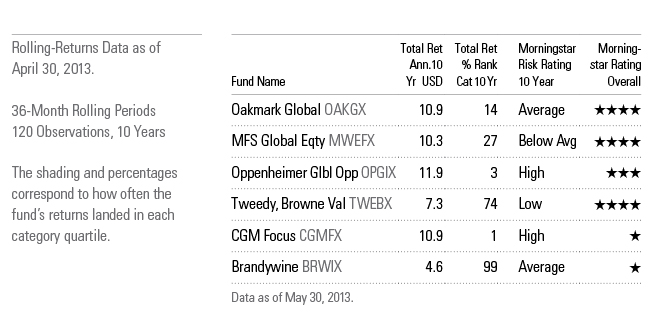

The rolling three-year returns for Oakmark Global (OAKGX) reflect the fund’s fairly consistent relative performance over the trailing decade. Over that stretch, its rolling returns landed in the category’s top quartile 45% of the time and in the second quartile 48% of the time. Skippers Clyde McGregor and Rob Taylor favor stocks trading at deep discounts to their estimates of intrinsic value. They’re no dumpster-divers, however, and they generally opt for companies with promising growth prospects. That double-barreled approach helps avoid value traps and builds a margin of safety into the portfolio.

The duo’s solid execution has kept the fund’s rolling returns mostly out of the category’s bottom two quartiles. However, periodic bumps are part of the package, given a fairly concentrated portfolio and top position sizes of 3.5%-5.0% of assets. In 2011, several of the fund’s then-top holdings such as Oracle (ORCL), Julius Baer (BAER), and Daiwa Securities (DSEEY) sold off, fueling the fund’s 11.6% loss that year and causing its three-year rolling returns to fall in the category’s bottom quartile for several periods ending in mid- to late 2012. Rolling returns don’t capture the fund’s above-average Morningstar Risk over the trailing three-year and five-year periods or the fact that investors have been compensated for that risk–those traits are reflected in the fund’s 4-star Morningstar Rating.

Rolling Steady

The rolling three-year returns for MFS Global Equity (MWEFX) land in the category’s middle two quartiles 60% of the time, yet it’d be a mistake to dismiss the fund as average. The fund has appealing defensive characteristics. Managers David Mannheim and Roger Morley stock up on higher-quality blue chips domiciled in developed markets. As of March 31, 2013, only 8% of assets were parked in no-moat stocks (those without any sustainable competitive advantage) versus the MSCI World Index’s 13%. That stability-oriented approach means the fund’s short-term performance will likely lag when racier fare is rallying, as in 2003, 2005, and 2009-10, but it held up nicely in 2008 and late 2011.

The duo’s style has translated into less volatility over the long haul. The fund’s Morningstar Risk-Adjusted Returns over the trailing decade through May 15, 2013, land just inside the group’s top quartile, and its three- and five-year rolling returns over that stretch didn’t once land in the category’s bottom quartile.

Roll With the Punches

Sometimes interpreting rolling returns isn’t as straightforward. Investors might see the three-year rolling returns for Oppenheimer Global Opportunities (OPGIX)topping the category 58% of the time and hop on board. Yet they shouldn’t overlook the 12% of the time it has landed in the category’s bottom quartile, which reflects its High Morningstar Risk. That volatile profile stems from manager Frank Jennings’ penchant for small-cap stocks, heady growers, concentrated sector bets, and top position sizes that at times have bumped up against 10% of assets. Apparently he’s toning down his approach a notch, but it’s too soon to tell whether the fund’s rolling returns will land more consistently in the middle of the pack.

The three-year rolling returns for Tweedy, Browne Value (TWEBX) also look a little extreme, though for very different reasons. Those rolling returns over the past decade land in the category’s top or bottom quartiles 85% of the time, but take those with a grain of salt. Over that stretch, the fund landed in the mid-value, large-value, and (since 2009) world-stock categories, yet both traits are to be expected given management’s approach. The fund’s deep-value DNA and focus on capital preservation mean its performance may lag quite a bit and for long stretches in up markets, testing investors’ patience.

Yet the fund should make up relative ground by losing less money when the market sours. Its 23.4% loss in 2008 was much lighter than the MSCI World’s 41.9% swoon, and the fund also fared relatively well in late 2011’s downturn. A single year of extreme outperformance or underperformance can skew a fund’s rolling returns, but virtually all of this fund’s top-quartile three- and five-year rolling returns stem from its relatively strong showings in 2008 and 2011. That, coupled with the fund’s Low Morningstar Risk rating, suggests this fund is most suitable for investors seeking strong downside protection, but only those able to look past years of weak relative returns when things aren’t as dire.

Let Some Funds Roll on By

Each of the funds above is a standout, but rolling returns can also raise a red flag. For instance, those for CGM Focus (CGMFX) land in the large-blend category’s top quartile 66% of the time and in the bottom quartile 29% of the time. That may seem like a good trade-off at first glance, but those bottom-quartile periods have been particularly painful, including a 48.2% loss in 2008 and a 26.3% loss in 2011.

Continuing on the 1-star theme, rolling returns for Brandywine (BRWIX) fall in the mid-growth category’s bottom quartile 42% of the time, reflecting that fund’s continuing challenges and raising the concern that management’s stock-picking doesn’t have the same edge it might have had 10-15 years ago.

Rolling returns are no silver bullet, but they can be a powerful diagnostic tool, especially if used in combination with other performance measures.

{kind=link}