GE Set to Exit Retail Lending; Worries About Banking Exposure Has Conglomerate Focusing on Industrial Operations

August 30, 2013 Leave a comment

August 30, 2013, 1:04 a.m. ET

GE Set to Exit Retail Lending

Worries About Banking Exposure Has Conglomerate Focusing on Industrial Operations

KATE LINEBAUGH and SHARON TERLEP

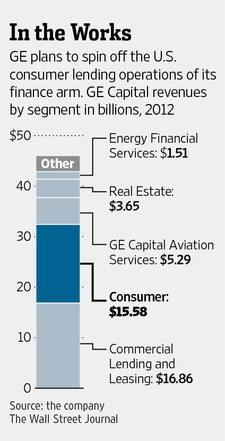

General Electric Co. GE -0.39% is preparing to spin off one of its most important financial assets—the unit that issues store credit cards for 55 million Americans—as it retreats from one of the high-growth businesses that defined the modern conglomerate. The decision to divest the business, amid concerns about the company’s exposure to banking, marks an important moment in the evolution of GE and the country’s three-decade long consumer credit boom. GE Capital expanded to the point that its portfolio of loans and other assets now would rank it as the country’s fifth-largest commercial bank.Preliminary work to separate the business through an initial public offering is under way, according to people familiar with the matter.

GE has said the U.S. consumer-finance business earned $2.2 billion last year. The operation accounts for about $50 billion of the $274 billion in loans outstanding by GE Capital.

An IPO could come early next year, the people said. Bankers from J.P. Morgan Chase & Co. and Goldman Sachs Group Inc. GS +0.43%are working on a possible offering, one of the people said. Alternatives including smaller spinoffs or asset sales are under consideration, the people said.

A sale of the unit would be quicker and more straightforward, but a buyer for the entire operation is unlikely to emerge given its large size and the fact regulatory hurdles largely prevent major banks from doing big deals.

The company’s consumer finance business provides store credit cards and financing for 55 million Americans at retailers such as Wal-Mart Stores Inc. WMT +0.07% andGap Inc.’s GPS +0.54% Banana Republic.

But after fueling the growth of the U.S. economy and GE’s profits for years, credit use hit a wall during the financial crisis, leaving investors wary of paying too much for shares of companies in the banking business. GE’s planned consumer-lending exit comes as low delinquency rates have the business performing better than it has in years.

GE Chief Executive Jeffrey Immelt is under particular pressure to beef up the conglomerate’s industrial side. GE’s shares have underperformed other industrial conglomerates like Honeywell International Inc. HON +0.77% and United Technologies Corp., UTX +0.48% which lack substantial finance businesses, and his pay in part rests on focusing on its industrial operations. The CEO has pledged to pare the company’s reliance on its lending business to 30% of its profits from more than 45% now.

GE has been steadily reducing the size of GE Capital since the credit crisis. It is moving against a backdrop of activist investors agitating for change at other American companies including Procter & Gamble Co., PG +0.60% Microsoft Corp.MSFT +1.61% and Apple Inc. AAPL +0.16% Mr. Immelt signaled in the spring that he was open to splitting off the retail financing assets that the company had unsuccessfully tried to sell before the financial crisis.

While the size of the planned IPO hasn’t been determined, credit card and payments company Discover Financial Services, which has $75 billion in assets, is valued by the market at about $23 billion.

Exiting consumer finance would remove a support that GE has leaned on to help prop up earnings as its power-plant business sputters. Overall, the consumer-lending business earned $3.24 billion globally last year, down 13% from 2011.

Mr. Immelt will need to move quickly to redeploy proceeds from a sale into industrial businesses that are seen as less risky. “Investors value financial-type earnings less than they value industrial-type earnings,” said Bob Spremulli, an equity analyst at teachers’ pension fund TIAA-CREF.

At the helm of GE for almost a dozen years, Mr. Immelt hasn’t had an easy go of it. Four days after taking over, the Sept. 11, 2001, terror attacks crippled his aviation business. The financial crisis half a decade ago whacked GE Capital, flattened sales and exposed the vulnerabilities of GE’s financial operations.

The damage is evident in the company’s share price, which is down roughly 40% over Mr. Immelt’s tenure. The S&P 500 stock index is up about 50% over that same period. Honeywell’s shares are up around 125%, and United Technologies is up about 200%.

The 57-year-old chief executive has responded by positioning GE as a global infrastructure manufacturer focused on complex, big-ticket items such as locomotives, jet engines and gas-fueled power generators. He has shed businesses that fall outside of that mandate, including entertainment arm NBCUniversal, the company’s plastics unit and its reinsurance business.

In December, Mr. Immelt said he would like earnings from the industrial businesses to account for 65% of the company’s earnings by 2015, up from about 55% in the quarter ended June 30. At an investor conference in May, Mr. Immelt alluded to the possible divestiture of bigger pieces of GE Capital through an IPO, saying the timing was good.

GE has moved to help its lending operations stand on their own by building up bank deposits and is keeping its options open for shedding assets over the coming few years. The consumer finance operation is highly profitable, according to GE executives. Michael Neal, who retired as the head of GE Capital in June, said in May that the private-label credit-card business had a return on equity of 50%.

In the second quarter, earnings at the U.S. consumer-finance business fell 12% from a year earlier to $563 million, while assets grew 9% and 30-day delinquencies fell to 3.85%.

At the end of June, its private-label card and consumer-credit business had $50.2 billion in loans in the U.S., of which 65% were related to the credit-card business. The remainder involved providing store credit on purchases of goods like electronics and recreational gear.

More broadly, big U.S. consumer-finance companies have faced tough headwinds in recent years, both from increased regulatory scrutiny and consumers focusing on paying down debt. Total credit-card balances, for example, have shrunk from nearly $900 billion in 2008 to $714 billion last year, according to industry consultant Nilson Report, a payments-industry newsletter.

For years, the conglomerate relied on its lending business as a source of profit and steady injections of cash to fuel industrial investments. The unit borrowed cheap, short-term funds, thanks to its ties to GE’s diverse industrial businesses and strong credit ratings.

But in 2009, GE’s access to that funding shriveled. Since then, GE has transformed GE Capital. Once an opaque institution that competed with private-equity shops, GE Capital now trumpets its mundane loans to fast-food franchises and trucking companies that get little attention from big banks.