Pay-TV Dinosaurs Study Evolution; Web TV Is a Threat to Pay TV—but the Old School Can Adapt

September 1, 2013 Leave a comment

Updated August 30, 2013, 7:23 p.m. ET

Pay-TV Dinosaurs Study Evolution

Web TV Is a Threat to Pay TV—but the Old School Can Adapt

Even if pay-TV providers are getting pushed around the living room, they can do more to keep a grip on the remote control. Cable and satellite companies find their margins attacked on one side by rising programming costs and on the other by more consumers dropping video subscriptions in favor of cheaper online options. Meanwhile, a new generation of consumers is being raised on services like Netflix NFLX -1.37% . And Big Tech companies angling to deliver TV over the Internet may be starting to make more serious inroads, as evidenced by recent news of Google‘s GOOG -1.00% talks with the National Football League and Sony‘s SNE -1.09% preliminary deal with ViacomVIA +0.03% to carry its channels.

That is indeed a challenging landscape. Despite the forces mounting against them, pay-TV providers are far from powerless.

As much as media companies might spar with them publicly, networks say they aren’t set up to deal directly with consumers and aren’t looking to do so. And even if consumers are unhappy with the current model of bundled content, they are unlikely to want to pay multiple bills to multiple companies as content moves online.

For cable and telecom companies, the most obvious way to guarantee a place for themselves in the future of TV is through control of the broadband pipes. Rolling out usage-based pricing would guarantee an incremental benefit for every video customer switching to watch content over the Internet.

It stands to reason that companies would want to have usage-based pricing in place before a tech company launches a fully Internet-based TV alternative. Yet most have been tentative about pushing such a measure, with the threat of consumer or regulatory backlash potentially holding them back. If pressures increase, though, they may grow less hesitant.

In the meantime, there are other things pay TV can do. One is to continue to innovate with the goal of making it easier for people to watch content on the device and schedule of their choice. This includes expanding options like video on demand and apps for so-called TV Everywhere. Devices like Dish‘s DISH +1.35% Hopper DVR and advanced interfaces like Comcast‘s CMCSA -0.82% X1 platform also help stave off cord cutting.

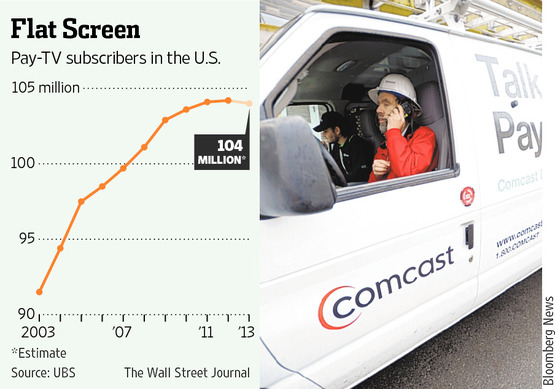

Granted, Big Tech TV entrants are likely to turn their expertise toward developing revolutionary interfaces and devices of their own. But there is inertia involved with switching video providers, and the 104 million U.S. households that subscribe to video services today are still pay TV’s to lose.

Even if pay-TV providers can’t beat Big Tech’s gadgetry prowess, they may be able to use pricing to their advantage. While programming costs are rising rapidly, greater scale allows companies to spread those over a wider base.

This suggests that, at least at first, tech companies will be at a disadvantage to traditional providers. Of course, tech companies could accept a lower margin on video subscriptions in hopes of gaining scale. But the higher cost basis may still make it difficult to undercut pay TV.

And if tech companies get media companies to sell their channels separately or in smaller groups, as opposed to the current practice of bundling them together, pay-TV providers should be able to demand similar terms.

Comcast and Time Warner Cable already offer less-expensive video packages that don’t include some sports. The ability to let consumers select their own channels or pay less for a smaller or less-costly set of them could further aid subscriber retention and help preserve margins.

Many of these initiatives could benefit from industrywide action, a possible reason Liberty Media Chairman John Malone is interested in spearheading cable consolidation through his interest in Charter Communications CHTR +0.43% . Mr. Malone’s vision—or a merger between satellite players Dish and DirecTV DTV -0.03% —could look more appealing as tech companies come closer to launching TV services.

The mounting threats may make it seem like pay TV is on the start of a journey toward extinction. But investors shouldn’t underestimate the industry’s potential to evolve.