China Cash Crunch 2: Just When You Thought It Was Safe to Go Back in the Markets

September 5, 2013 Leave a comment

September 5, 2013, 2:15 PM

China Cash Crunch 2: Just When You Thought It Was Safe to Go Back in the Markets

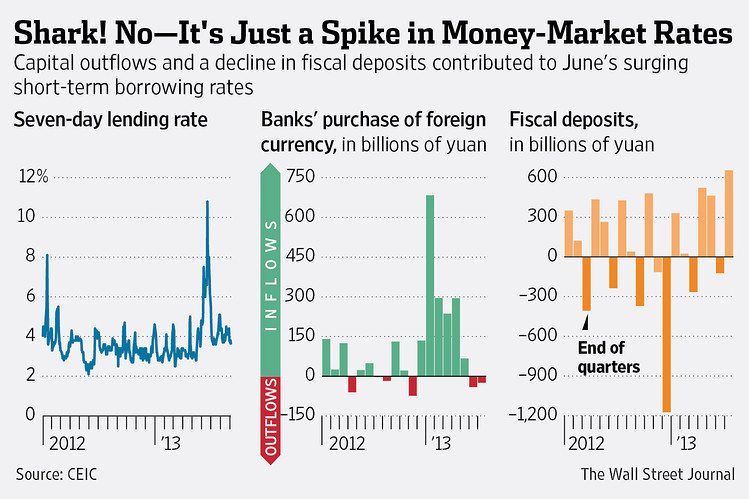

Could June jitters in China’s money market be followed by a September shudder? The causes of the June cash crunch that pushed short-term borrowing rates close to 30%, triggering a sell-off in the mainland’s equity and bond markets, were complex. But analysts break it down into five main factors. Some of them look set to return.

1. Capital outflows. With a hefty trade surplus and foreign companies lining up to invest in factories, China has got used to seeing capital flowing in. But those flows reversed in June as the U.S. Federal Reserve suggested it would soon start winding up the ultra-loose monetary policy that has pushed bucket loads of dollars into emerging markets. Net foreign exchange outflows from China totaled 41.2 billion yuan ($6.73 billion) in June. China’s central bank “really underestimated how much liquidity was leaving the country,” said Francis Cheung, an analyst at brokerage CLSA – part of the reason it didn’t move faster to supply liquidity to the market. Capital outflows continued to the tune of 24.5 billion yuan in July, the most recent figure available. Lately the outward pressure may have relented, since China has started to post better economic data. The offshore yuan traded in Hong Kong has been stronger than its onshore counterpart since early August, suggesting that capital wants to get into the country. Still, with investor sentiment fragile, and the Fed poised to start unwinding its quantitative-easing program, cash could easily start heading out again.

2. End-of-quarter demand for cash. China’s financial system has to deal with regular liquidity strains as banks pretty up their loan-to-deposit ratio to meet regulatory hurdles at the end of each quarter.

Small banks often manage to boost their loan-to-deposit ratio by as much as 5% to 7% in time for the end of the reporting period, according to Mike Werner of Bernstein Research. Given existing loan and deposit levels at small and mid-size banks, that could mean demand for as much as 1.6 trillion yuan from the money markets.

3. Wealth-management products falling due. China’s banks have massively expanded their stock of wealth-management products, short-term investment products that offer some of the security of a deposit but with higher returns. The value of outstanding wealth-management products topped 10 trillion yuan by the end of March, according to estimates by Fitch Ratings.

The problem: with short-term products sold to savers used to make long-term investments, when the products fall due banks often have to hit the money markets for funds. Charlene Chu, China bank analyst at Fitch, estimated that 1.5 trillion yuan in wealth-management products fell due in the last 10 days of June – adding to banks’ demand for cash.

Having experienced a nasty cash crunch once, the banks may now be taking liquidity management more seriously, but Bernstein’s Mr. Werner isn’t counting on it. “It would be reckless if they didn’t adjust their behavior,” he said. “Does that mean they will? Not necessarily.”

4. Drawdown of fiscal deposits. Government departments add to seasonal demand for liquidity by drawing down their deposits as the end of the each quarter nears. They withdrew 121.9 billion yuan of fiscal deposits in June, pulling in the opposite direction as the People’s Bank of China tried to soothe the market.

The end of this quarter will likely follow the same trend: September has seen an average 987 billion yuan fall in fiscal deposits in the last three years.

5. Actions of the big banks. The PBOC could cast away these problems with a wave of its monetary wand, but that would undermine its goals of clamping down on financial speculation and slowing growth of the money supply.

The central bank surprised everyone with its reluctance to provide liquidity in June, though data now available show it did put its balance sheet to work – loaning 433 billion yuan to cash-strapped banks.

Some of China’s biggest lenders also stepped into the breach. Industrial and Commercial Bank of China lent more than a trillion yuan into the interbank market during the crunch, its chairman said, and Agricultural Bank of China supplied a net 840 billion yuan. Neither bank said whether the central bank had leaned on it to release the funds.

Add it up, and the strained calm of the last two months might be tested.

“There’s a decently high chance that you’re going to see rates get very volatile as we get into the fourth quarter,” said Jonathan Anderson, a former International Monetary Fund economist now at Emerging Advisors Group. “I don’t think we’re done.”