Rates too low: Why housing trouble in Australiaa could be just months away

September 16, 2013 Leave a comment

Rates too low: Why housing trouble could be just months away

Published 12 September 2013 10:04, Updated 12 September 2013 12:19

Christopher Joye

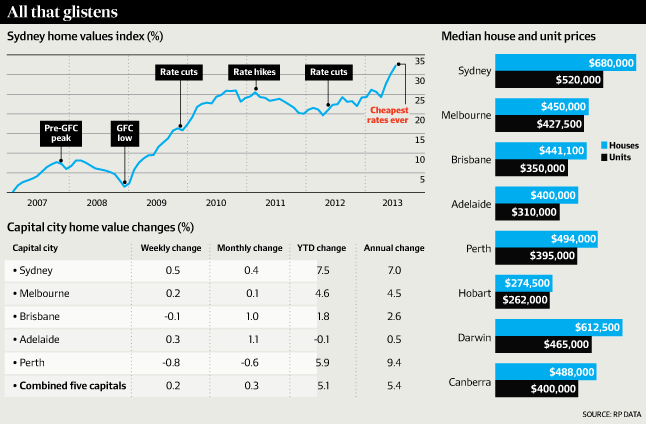

I am worried about Australia’s housing market. Very worried. Not so much about the fundamentals, which are solid. Or current performance, which is robust without raising alarm. I am concerned about what lies around the corner – and here, I am talking months, not years. I presented at a hedge fund conference during the week with notorious housing pessimist Gerard Minack. There was a fascinating role reversal. Asked about Australia’s housing prospects, Minack said he now buys into the view that house prices will track incomes. Minack was up front in admitting that he forecast striking price falls during the global financial crisis – he certainly bandied around figures in the 20 per cent range. He explained that he was wrong because it was “garbage in and garbage out”. The enormous rise in the jobless rate he anticipated never materialised.This has been a maxim I’ve advocated for years. I’ve regularly demonstrated that domestic housing costs have tracked, or slightly under-clubbed, disposable household income growth since 2003. That’s comforting and what should happen through a cycle. Amid forecasts of catastrophic gloom in 2008 and again in 2011, I attracted criticism for publishing more reassuring views.Price depreciation was likely to be modest, I argued. And if the Reserve Bank of Australia cut rates, the elasticity of our interest rate sensitive housing market would surprise on the upside. This was close to what transpired.

RBA cuts have gone too far

But I no longer think the situation is so benign. The RBA’s rate cuts have gone too far. And if they stay this low for too long, there is a real chance Australia could, belatedly, have an acute housing crash with real consequences for the economy.

While this is not my current central case, several factors give me pause.

The first is that households have not really deleveraged despite much spruiking about our “cautious consumers”. Australia’s elevated household debt-to-income ratio, which looks set to climb further, is not far off the all-time, pre-GFC peak.

This highly leveraged consumer is an artefact of Australia’s even more leveraged banking system. The major banks are leveraged about 80 times across their $1 trillion home loan books. Put differently, they are only holding about $1.25 of true loss-absorbing capital against every $100 – as opposed to the “risk-weighted” value – of their assets.While banks do not “mark to market” their mortgage books with current prices because they account for them on a “hold to maturity” basis, with such extreme leverage you only need a small drop in asset values to make the banking system theoretically insolvent (assuming market prices).