India and the danger of potential

September 24, 2013 Leave a comment

India and the danger of potential

| Sep 24 11:47 | Comment | Share

If India continues its current path it will face a catastrophic shortage of jobs, creating a young and angry population, and with it conditions for social unrest and economic disaster. Whether India exploits or is undermined by its demographics will likely be determined by the policy choices over the next two administrations. It simply cannot afford a repeat of the last five years. That’s from a recent Espirito Santo note that makes for refreshing reading compared with the usual demographic dividend stories that cruise through our inboxes every few days.India is understandably a favourite topic of the latter, more usual, type — Deutsche, for example, has India’s working age population hitting 866.5m in 2040, and that’s with a cutoff age of 59 years, meaning it would bypass China as the world’s largest pool of workers in the late 2020s.

A little more from ES on what threatens to be quite the resultant mismatch:

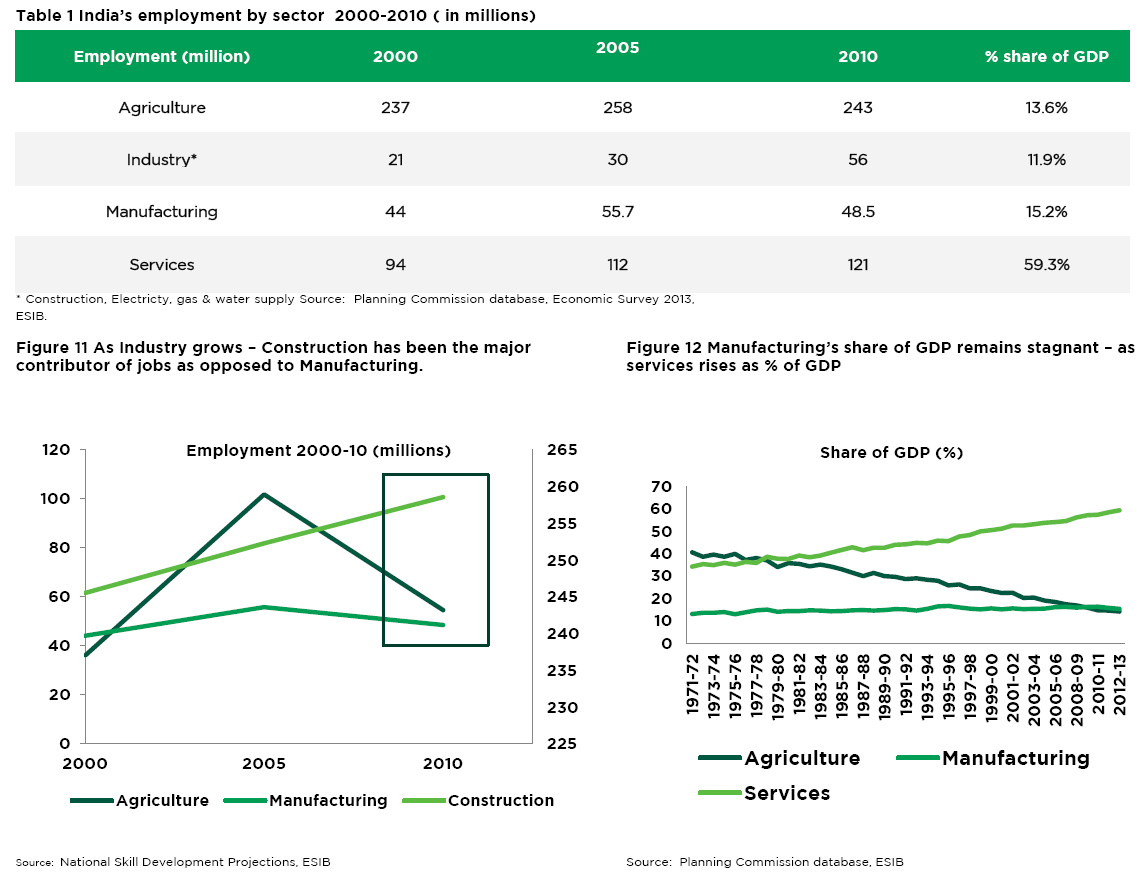

Manufacturing’s importance [in India] has stagnated for 40 years and now contributes 15-16% to GDP, employing only 10.2% of the labour force. Services has meanwhile grown its share nearly 10% every decade to 60% of GDP today. But employment creation hasn’t kept pace, with the labour force share growing from 17% in the early 1970s to 27% today. This precocious development model isn’t sustainable. Services is unlikely to employ more than 25-30% of the incoming labour force over the next decade. Manufacturing will have to pick up the bulk of the rest. Yet manufacturing has added jobs at only 1-2 million a year since the 1970s, and actually lost 7 million jobs between 2005-2010.

And whilst manufacturing isn’t creating enough jobs and the nation faces a huge labour surplus, services actually faces a shortage of people with the right skills for the kinds of jobs it is creating, causing wage inflation in the sector which risks eroding its comparative advantage. If these scenarios play out in tandem, and they will if current trends continue, demographics would create a disaster – not a dividend.

The intent here isn’t to blindly counter the optimism of the headline numbers but to point to the enormous policy challenges that exist (and have existed but not been met). Sure, the pressures created by imbalances will force change over time in one way or another, but choosing not to preempt them ignores the sad danger inherent in potential.

A final chunk from ES (with more on policy challenges, China comparisons and the likein the usual place for those who want it):

Our point in this note isn’t that India should follow the East Asian model. Its development path has been and will be different. India’s growth of and comparative advantage in services is to be celebrated and fostered. Our point is simply that India can’t take an entirely different development path. It needs successful large-scale manufacturing to productively absorb its demographic bulge. Our tone in the note might seem pessimistic. But our point is really that India’s ability to exploit its demographics over the next 20 years, or to be undermined by them, remains highly uncertain, and will be probably be determined by the policy choices and implementation of government, and probably by the next administration. That is how urgent the challenge is.

Interesting then, as Ambit Securities note, that the most reformist governments in India have been minority ones like the Narasimha Rao government which initiated the 1991 reforms. In fact, say Ambit:

a large part of the underperformance of the current Government could be attributed to the fact that the Congress had more than 200 seats in the Lok Sabha which in turn made the majority party highly complacent.

So the suggestion that, right now, the most likely outcome of the 2014 election is a whoppingly large coaliton formed by the BJP (with or without Modi at its head) needn’t be cause for automatic depression.