Financial consulting: The advisory industry has shown remarkable resilience since the crisis

September 27, 2013 Leave a comment

Financial consulting: The advisory industry has shown remarkable resilience since the crisis

Sep 28th 2013 | New York |From the print edition

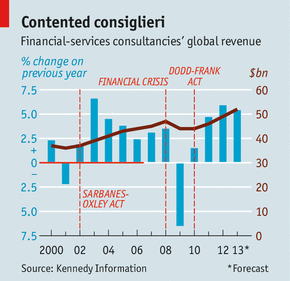

CONSULTANTS studiously avoid taking credit for their clients’ successes in order not to be blamed when things go awry. They have not been able to avoid the spotlight during the financial crisis. In a 2008 shareholder report explaining a huge write-down, UBS blamed “external consultants” for recommending that it go into areas like subprime mortgages. An ex-head of Citigroup’s investment bank told investigators he had relied on “a careful study from outside consultants” when moving into collateralised-debt obligations.Yet although many Wall Street titans failed during the crisis, the advisers whispering in their ears have emerged even stronger (see chart). According to Kennedy Information, a research firm, the global financial-services consulting business posted record revenues of $49 billion in 2012, a fifth of the consulting industry’s total.

Three main factors account for the consultants’ resilience. Perhaps the most powerful is the business’s each-way bet on boom and slump. When the economy is flourishing, banks, insurers and asset managers are eager for counsel on mergers, marketing and expansion. When it crashes, they are desperate for guidance on cutting costs and divesting dud assets. “The Firm”, a new history of McKinsey, recounts how the company’s consultants joked that they would first tell banks to close underperforming branches. Once they cut too far, McKinsey would then recommend ambitious expansion. When the banks grew too large, the cycle would start anew.

A second boost comes from the rise of “Big Data”. Regardless of the business cycle, banks and investors are constantly improving statistical models and trading platforms. All six of the biggest financial consultants—the consulting arms of the “Big Four” accounting firms of Deloitte, PwC, Ernst & Young and KPMG, plus IBM and Accenture—have large information-technology practices. A handful of boutiques, such as Britain’s Holley Holland, specialise in integrating the data systems of sprawling financial conglomerates.

Consultants have also profited from financiers’ consistent failure to analyse their own businesses. Banks and asset managers have little information on their clients’ behaviour and preferences. That has opened the door for strategy consultants, from generalist giants like McKinsey and Boston Consulting Group to niche advisers such as Novantas and First Manhattan. Such firms have industry benchmarks coming out of their ears.

The final source of buoyancy for the consultants is compliance and risk consulting. Facing a host of new rules, clients have flocked their way. Perhaps the biggest beneficiary is Promontory, a boutique headquartered in Washington, DC, that now has nearly 400 employees. Its boss, Eugene Ludwig, once led America’s Office of the Comptroller of the Currency (OCC); most of its staff have come from the public sector. It charges hefty fees to advise firms on how to comply with regulations and what to expect from the government. Promontory’s fans argue that it helps firms follow the rules. Critics counter that ex-regulators’ inside knowledge enables clients to exploit overstretched public agencies.

In some cases governments have become big clients themselves. Oliver Wyman, a strategy firm, did little work for the public sector before 2009; now such jobs make up an estimated fifth of its financial division’s revenue. The Bank of Spain hired it to “stress test” the country’s banking system in 2012; on September 24th the European Central Bank announced it had chosen the company to help review loan books across the continent for its forthcoming “asset quality review”.

Regulators can also hand work to consultants indirectly, by ordering the targets of regulatory actions to hire outside firms. But that risks creating a conflict of interest between the consultant’s loyalty to the company that pays it and to the regulator it must report to. In 2004 New York regulators and Standard Chartered agreed that the bank would hire an outside firm to examine its money-laundering compliance standards. In 2012 state regulators accused the consultant, Deloitte, of providing Standard Chartered with confidential information about its other clients, and of removing a recommendation from a report at the bank’s behest. In June Deloitte agreed to pay a $10m fine and for a year to stop taking on new work requiring the regulator’s approval. New York has also subpoenaed Promontory in the case, and PwC in an investigation of its work for a Japanese bank.

A much bigger snafu unfolded in 2011-12, when the OCC and the Federal Reserve began a review of home foreclosures. They required 14 mortgage servicers to engage independent analysts to pore through 800,000 loans. Almost two years later, the firms had not finished even a quarter of the work. In January the government reached a deal with 11 of the servicers to end the review early. They agreed to pay homeowners $3.6 billion—less than twice the $2 billion paid to the consultants.

All of which has increased the odds that financial consultants will themselves become targets of regulation. In its deal with New York, Deloitte agreed to new rules regarding communication with the government and transparency. The state is now making those policies mandatory. Federal restrictions may be next. In April the Senate held a hearing on the industry. The OCC has requested that Congress allow it to sanction misbehaving companies; Maxine Waters, a Democratic legislator, has introduced a bill that would require the government to pay consultants directly. Consultants have spent years profiting from the heavy hand of the state. They may soon get slapped by it.