Michael Mauboussin – What Does a PE Multiple Mean? PE Multiples Are Not Valuation, They Are Shorthand: Mauboussin

February 9, 2014 Leave a comment

Michael Mauboussin – What Does a PE Multiple Mean?

by VW StaffFebruary 07, 2014, 12:07 pm

Michael Mauboussin is considered an expert in the field of behavioral finance and has some famous books on the topic including, Think Twice: Harnessing the Power of Counterintuition and More More Than You Know: Finding Financial Wisdom in Unconventional Places.

Michael Mauboussin new report from CS

The price-earnings multiple remains the primary method analysts use to value stocks. 3 Researchers who surveyed equity research reports found that more than 99 percent of the analysts used some sort of multiple and less than 13 percent used any variation of a discounted cash flow model.4 Price-earnings multiples may be a common way to assess the attractiveness of a stock, but most investors fail to have a clear sense of what a particular multiple implies about a company’s future financial performance and don’t understand how multiples change over time.

The sloppy use of multiples is almost everywhere you look. In our opinion, some analysts justify their recommendations with apples-to-oranges comparisons of businesses with different economics, suggest companies should trade at the same multiple as the past without a solid economic justification to do so, and compare price-earnings multiples with growth rates without any mention of the underlying economic returns. Price-earnings multiples are widespread in use yet remarkably poorly understood.

Take as an example two companies, Apple, Inc. (AAPL) and Edison International (EIX), which had the same price-earnings multiple, 12.8, based on year-end 2013 prices and 2014 consensus earnings estimates. Setting aside any perceived mispricing, it stands to reason that the prevailing price-earnings multiple implies radically different outlooks for these two companies. They are in separate sectors (information technology and utilities), with vastly disparate economic returns on capital (AAPL’s CFROI® is 25 percent versus EIX’s 5 percent), substantial variance in the outlook for earnings growth (the expected 5-year earnings per share growth is nearly 50 percent for AAPL and 7 percent for EIX), and very different capital structures (AAPL has net cash while EIX has a healthy amount of debt).

How can two companies so unalike have the same price-earnings multiple? Contemplating how these two stocks arrive at the same multiple from very different directions provides a mental warm-up for the process of carefully considering what comprises a price-earnings multiple. Without a proper appreciation for the factors that determine a multiple, there is no way to apply it intelligently in exercises of relative or absolute valuation.

The value of a financial asset is the present value of future cash flows. Few serious market practitioners would disagree. But many investors shun models that project and discount future cash flows because they deem them too complicated or sensitive to assumptions. Yet these same individuals seem blithely content to rely on multiples.

Here’s the challenge. With discounted cash flow models, the value is sensitive to the inputs. But the assumptions underlying the inputs are explicit. You can compare them to base rates, discuss them, and debate them. With multiples, those assumptions are buried. The assigned multiple becomes a point of persuasion rather than a thoughtful case based on the economic drivers of value.

The goal of this piece is to provide an analytical bridge between price-earnings multiples—really, multiples of any kind—and sound economic reasoning. We’ll start by looking at price-earnings multiples through a classic valuation lens, and will examine the two main components of that model. We’ll finish by discussing the role of multiples in considering price-implied expectations.

PE Multiples Are Not Valuation, They Are Shorthand: Mauboussin

by Michael IdeFebruary 07, 2014, 2:37 pm

Price-earnings multiples (PE multiples) are the most commonly used tool for evaluating a stock’s futureprospects, but according to Credit Suisse analysts Michael Mauboussin and Dan Callahan, few have a solid grasp on what it means.

“The sloppy use of multiples is almost everywhere you look,” write Mauboussin and Callahan. “PE multiples are widespread in use yet remarkably poorly understood.”

Valuation can be broken down into multiple components

They argue that company valuations are best understood when broken down into two distinct pieces: steady-state value and future value creation. Steady-state value is fairly intuitive, measuring net profits against the cost capital, plus any cash lying around. Future value creation is more complicated. While most investors think in terms of growth, the concept can be misleading because there is a cost of capital. Growing with returns below the cost of capital actually destroy shareholder value.

“Acquisitions are a good example because the acquiring company grows, and in many cases the deal is accretive to earnings per share. That many deals grow the business and earnings yet destroy value is a stark reminder that an acceptable return on incremental investment is paramount,” they write.

Future value creation depends on the spread between return on invested capital and the cost of capital (which can certainly be negative), the size of the investment, and the company’s ability to find investments with a positive spread (competitive advantage period in the equation below).

Steady-state value accounts for 80% of the market’s value

Breaking down the entire market into these two pieces, steady-state value accounts for about 80% of current market values, but that changes over time.

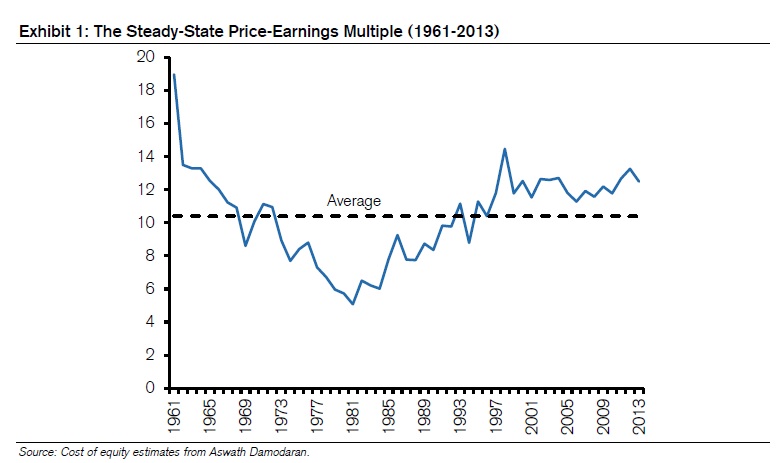

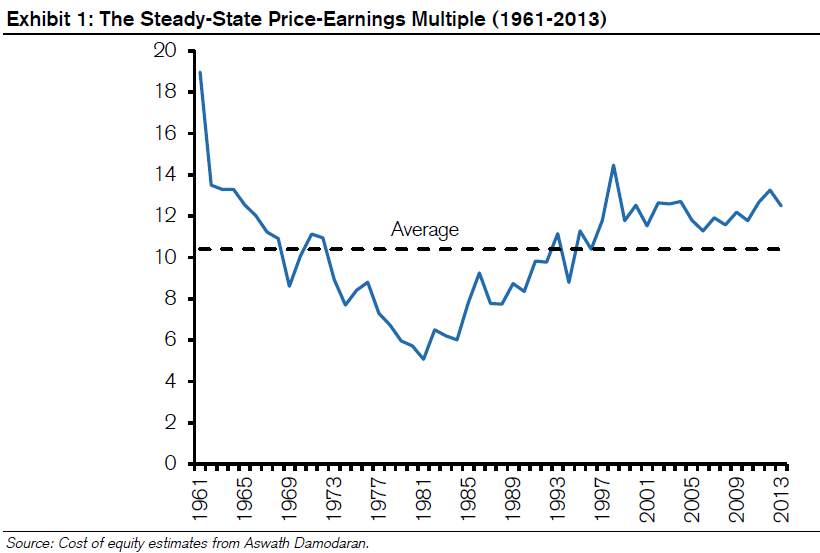

“As of the beginning of 2014, Aswath Damodaran, a professor of finance at New York University’s Stern School of Business, estimated the cost of equity in the United States to be 8 percent. This translates into a steady-state PE multiples of 12.5 times,” write Mauboussin and Callahan.

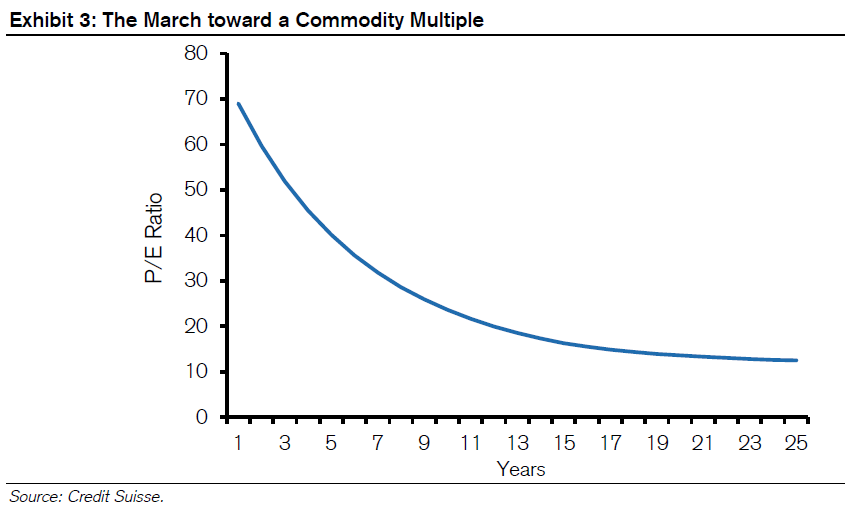

Understood this way, it also makes sense that most companies’ PE multiples will decline over time as the business matures and the stock price approaches its steady-state value, and while actual stocks are more complex than models, you can see how the decline in PE multiples for mature businesses trends toward what Mauboussin and Callahan call the commodity multiple.

“Multiples are not valuation; they are shorthand for the process of valuation,” write Mauboussin and Callahan. Comparing PE multiples without understanding how those multiples break down into component pieces is investing blindly, in their view, and washes out important distinctions between companies by aggregating everything into a single, oversimplified number.