Big Banks’ Vanity Unfair for Their Investors

February 14, 2014 Leave a comment

Big Banks’ Vanity Unfair for Their Investors

JOHN CARNEY

Feb. 11, 2014 2:46 p.m. ET

Even leaving aside the flashy watches, bespoke suits and ostentatious vacation homes, bankers’ obsession with the way they are perceived may be more costly than it appears—costly to investors, that is.

A recently revised working paper from a trio of economists at the Federal Reserve Bank of New York demonstrates that in the depths of the financial crisis, banks willingly overpaid for loans from the Fed. They did so by choosing to borrow from a special facility, even though the cost was at a substantial premium to funds available from the Fed’s discount window, the paper notes.

The likely reason: Banks wanted to avoid the stigma of borrowing from the discount window. So they chose to borrow more expensively—raising their own interest expense at a time when the financial system was under severe strain—for appearance’s sake.

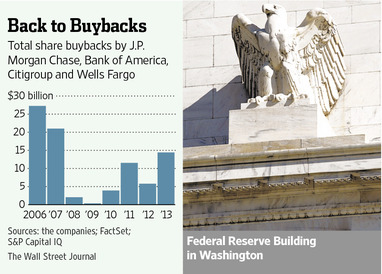

Albeit crisis-era behavior, it is telling for investors who in March will learn which big banks have received the Fed’s blessing for capital returns. In large part, those will come in the form of share buybacks.

While investors usually welcome buybacks, banks don’t seem to take a disciplined approach to them. That may lead them to again overpay, especially given run-ups in many bank stocks last year, in hope of looking good to investors.

Recent history shows how banks can destroy value when overly optimistic executives buy too high and are sometimes forced to later sell low. Bank of America, BAC +0.96% for example, spent $3.8 billion in 2007 to repurchase 73.7 million shares at an average price of $51.42 a share, or about 3.4 times its average tangible book value at the time. Less than two years later, it needed to issue billions of new shares at an average price of just $13.47.

Some banks have talked about the need for more restraint on buybacks. On J.P. Morgan Chase‘s JPM +1.22% latest earnings call, chief James Dimon explained why his bank had repurchased just $2.2 billion of stock in the last three quarters of 2013, since receiving authorization to buy back $6 billion through the end of the first quarter of 2014.

“We don’t just buy back stock regardless of price. Not that we think it’s a bad price, but when it was at $33 a share or whatever, that was an extraordinarily compelling price,” said Mr. Dimon, who had previously spoken of reducing buybacks when the stock exceeds certain levels of price to tangible book value.

Most banks, though, don’t seem to link buybacks to valuation. They are simply eager for them as a means to return excess capital and boost returns on equity.

And the Federal Reserve, which signs off on the banks’ capital-return plans, has tended to give them greater leeway in terms of buybacks than dividends. This is largely a response to a crisis experience: Banks were loath to cut dividends, even when their financial condition was deteriorating, for fear of spooking investors.

But this only reinforces inflexibility when it comes to dividends. So investors are led to once again believe that such payouts are sacrosanct, even as it prompts banks to possibly overpay for their own stock.

Buybacks can also prove ineffective in reducing shares outstanding—which should boost earnings per share—due to stock issuance to employees. Over the past three years, for example, Wells Fargo WFC +0.99% has bought back about $11.7 billion of its own stock. That is equal to nearly 5% of its current market value. Yet the bank’s average shares outstanding have declined by less than half of 1% from the first quarter of 2011 through the end of 2013.

Perhaps the lesson for investors is simple: Banks may be specialists in lending money, but aren’t always wise about how they borrow and spend it.