German Thriftiness Vexes Banks; A Glut of Deposits Has Lenders Struggling to Invest It All

February 22, 2014 Leave a comment

German Thriftiness Vexes Banks

A Glut of Deposits Has Lenders Struggling to Invest It All

CHRISTOPHER LAWTON and LAURA STEVENS

Feb. 13, 2014 4:16 p.m. ET

FRANKFURT—Hauke Hanke’s frugality is becoming a problem for Germany’s banks. Like many of his compatriots, the 30-year-old scientist from Berlin typically saves as much as 25% of his paycheck every month.

Despite earning a paltry return on his savings account at Postbank, a part of Deutsche Bank AG DBK.XE -0.45% , he said it is too much work to shop around for the best deal on interest rates. As for racier investments such as stocks, he also thinks it is too much effort to ensure good returns, while his friends and family often avoid them because of the risk.

“Germans really hoard their money,” he said.

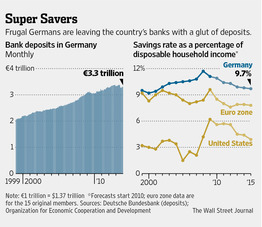

While Mr. Hanke saves even more money than his average countryman, thrifty Germans are leaving the country’s lenders with a glut of deposits. Bank deposits in Germany hit an all-time high of €3.39 trillion ($4.6 trillion) in June of last year, before falling slightly to an estimated €3.3 trillion in December, according to the latest monthly data from the Deutsche Bundesbank, Germany’s central bank, whose records stretch back to December 1948.

At a time when economic growth is lackluster and loan demand tepid, Germany’s banks are finding it hard to put all of those deposits to work and earn a decent return.

The interest margin for German banks, calculated as net interest income divided by average annual total assets, has been decreasing over the past three decades.

The European sovereign-debt crisis in 2009 exacerbated the problem, and the long period of low interest rates in the euro zone is making the situation even more difficult. The margin is now just below 1% from around 2% in the mid-1990s, according to Germany’s central bank.

“The most important source of earnings, especially for the German universal banking system—net interest income—is declining,” Sabine Lautenschläger, a European Central Bank executive board member, said late last year, when she served as vice president of Germany’s central bank.

Throughout the crisis, risk-averse Germans have poured their money into the safety of the country’s stable banking network, particularly its small savings and cooperative banks.

Fearing a resurgence of euro-zone problems, business owners and customers increasingly keep their money liquid in the form of demand deposits, which can be withdrawn at any time.

Such deposits are expensive to banks because the interest rate they pay on them is higher than what they would pay if they borrowed the cash from other banks. Rock-bottom interest rates for longer-term deposits provide no incentive for savers to lay the money down for longer.

Recent data show that the level of retail demand deposits increased to a record €935.8 billion in November 2013 from €510.1 billion five years earlier, according to the latest data from Barkow Consulting, a financial-consulting firm.

The savings culture stems from the economic troubles following the two world wars and was amplified by the euro crisis, according to experts. Germans are expected to have saved 9.9% of their disposable income in 2013, according to a forecast by the Organization for Economic Cooperation and Development. That compares with a forecast saving rate of 7.9% in the euro zone and 4.5% in the U.S.

About 9.4 million Germans, representing about 15% of the population, participated in the stock market either directly as shareholders or indirectly via funds as of the first six months of 2013, according to the Deutsches Aktieninstitut, a trade group representing capital-markets interests in Germany.

Two factors have contributed to the low participation rate, said Andreas Hackethal, a professor at Frankfurt’s Goethe University who has studied the trend. The dominance of government-backed social pension plans for retirement planning means Germans don’t need to invest in stock investment vehicles like the individual retirement accounts or 401(k) plans popular in the U.S.

In addition, many investors who waded into the market for the first time in the past couple of decades suffered losses, Mr. Hackethal said. “Many Germans have burnt their fingers,” Mr. Hackethal said. Others “are scared to make a mistake.”

Traditionally banks have invested deposits in German government bonds, known as Bunds, for profits, but record-low interest rates have nearly eliminated gains.

That leaves lending as one of the banks’ only recourses, but Wolfgang Kuhn, chief executive of Südwest Bank, a private bank in Stuttgart, said that customer deposits have increased faster than credit demand, thanks in part to the uncertain overall economic environment.

Unfortunately for German banks, relief from low interest rates is unlikely to come soon.

In November, ECB President Mario Draghi addressed German banks’ concerns about “the implication of low interest rates for savers” during a visit to Berlin, calling such worries understandable, but said “interest rates are low because the economy is weak.”