Beijing Signals New Worry on Growth

March 6, 2014 Leave a comment

Beijing Signals New Worry on Growth

Economic Growth Forecast Is Unchanged From Last Year at 7.5%, but Leaders Show New Concern on Reaching Goal

MARK MAGNIER

Updated March 5, 2014 2:08 a.m. ET

The Chinese government maintained the country’s growth target at 7.5% for the coming year. But as City University of Hong Kong professor Joseph Cheng tells Deborah Kan, concerns over steady growth are mounting.

BEIJING—China’s leaders kept the growth target for their giant economy unchanged but signaled that they are more concerned than ever about reaching it, giving themselves the option of letting credit flow freely to keep from falling short.

The suggestion of more lending to buoy growth—despite repeated recent efforts to rein in debt—is the latest sign of government unease that a slipping economy could trigger higher unemployment and corporate failures, aggravating already high social tensions.

For years, China kept a growth target of about 7.5% but actually grew far faster; in the last two years the economy has barely cleared that figure, and many economists have said it would have a tougher time meeting the goal this year as its economy matures and global demand for its exports comes under pressure. That is a troubling trend for the rest of the world, which has increasingly depended on China to fuel the global economy.

At home, as well, the Chinese regime has felt pressures that can be exacerbated by a slowing growth rate. Last week the government set up a committee to improve cybersecurity and police the Internet, upsetting some middle-class Chinese who have taken to social media. Over the weekend, assailants rampaged through a provincial railway station, killing 29 in what the government says was the work of separatists from the northwestern Xinjiang region.

In opening the annual session of the national legislature Wednesday in the Great Hall of the People, the leaders and the more than 2,900 delegates stood for a moment of silence to honor the victims of Saturday’s knife attack.

In his work report to the National People’s Congress, Premier Li Keqiang said government spending is being increased by more than 9%, with a push to build more public housing, and the overall fiscal deficit is projected to rise more than 12%.

Mr. Li called for a “balanced” monetary policy, in a change from the “prudent” monetary policy used last year. The slight wording change allows the government to loosen credit, a move that economists have said would likely give a short-term boost but worsen the growing credit problems plaguing local governments and the shadow-banking market.

Economists are bracing for trust and bond defaults this year and greater market volatility given the number of debt-plagued companies close to the edge. A third of the outstanding 4.6 trillion yuan ($750 billion) trust loans are due to mature this year, which many struggling firms rely on for capital.

Many construction and real-estate companies are also heavily dependent on debt-laden local governments for work building dead-end projects. Nearly half the 17.9 trillion yuan debt held by local governments in mid-2013—up 67% from the last audit in 2010, according to a National Audit Office report—comes due this year. Standard Chartered economistStephen Green says there is a better-than-50% chance that a local-government bond will default this year.

China’s Ministry of Finance said military spending this year would rise more than 12%—the largest percentage rise in defense spending since 2011 and continues an almost unbroken string of large increases for two decades.

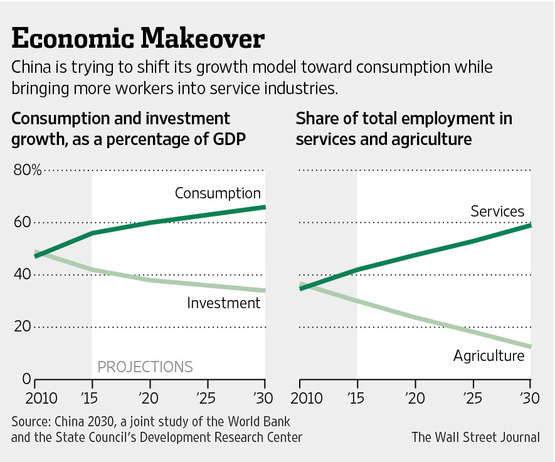

Maintaining fast growth will become increasingly challenging. The World Bank and the government’s Development Research Center project a decline in China’s average annual growth rate from 8.6% during the 2011-2015 period to 5% by 2026-2030.

That is assuming China suffers no major shock and carries out reforms to give economic winners such as technology companies, entrepreneurs and service industries—not low-end mines and bloated state factories with good party connections—preferential access to capital and equipment.

Sitting in his renovated Shanghai apartment, 27-year-old Ma Yiding said he has seen many venture capitalists, bankers and brokers through his website marketing job become increasingly cautious as debt mounts and more real-estate projects sit empty.

“China’s economy is not so healthy,” he said. “Markets should be able to solve their own problems, which carries some promise. But I’m somewhat pessimistic over how much we can really change.”

Mr. Ma sees too much focus on economic growth and not enough on consumer and quality-of-life issues, including air pollution. “The Internet has all sorts of products for baby care,” he said, patting his dog, Twitter. “But it’s really hard to find a park where children can play.”

During its 2002-2007 heyday following accession to the World Trade Organization, China saw exports grow 29% annually on average, helping fuel global growth of 3.4%, among the highest six-year average on record.

Among the biggest foreign beneficiaries of China’s stellar rise have been commodity producers, many of whom are now struggling.

On Indonesia’s Bangka and Belitung islands, white-sand beaches and swaying palms mask trouble in paradise. The area produces most of Indonesia’s tin—BHP Billiton was partly named after Belitung—and China’s reduced appetite is giving mine owner Johan Murod headaches as he watches company revenues decline by some 25% since last year. In a bid to survive, he has cut business travel at his company, PT Babelionia Internasional, and used mining tracts to breed cattle, farm fish and grow water spinach.

The pain isn’t limited to tin; China’s demand for local palm oil and pepper is also declining.

“If you come here, you’ll see banks, coffee stalls and shops are all quiet now because so many people are out of work or watching their incomes drop,” Mr. Murod added. “The impact of the China slowdown is very significant.”

Domestically, China faces a crossroads as its investment-led growth model flags. The challenge ahead, economists said, includes easing land, labor and capital controls—a cultural shift for a government with a penchant for control.

Even as older Chinese save and scrimp, many in China’s younger generations are tired of delayed gratification. “I see spending as an investment in myself,” said Huang Bingni, a 38-year-old beauty products saleswoman in the eastern city of Maanshan, who uses much of her income on cosmetics and nice clothes. “I want to have a good life now.”

Chinese companies that focus on quantity over quality and ignore customer service face a tough future, said Wang Jinshi, owner of Beaumarchais, a company producing high-end, custom-made shoes in the southern city of Foshan.

“This kind of company can’t survive,” he said. “Quality is really important now.”