Buffett’s Berkshire Beatdown

March 9, 2014 Leave a comment

Buffett’s Berkshire Beatdown

Posted MAR 4 2014 by WESLEY R. GRAY, PH.D. in TURNKEY BRAINWAVE, UNCATEGORIZED

Wesley R. Gray, PhD, has been sharing knowledge via his blogs since 2007. Dr. Gray and his team have created over a thousand posts and have thousands of readers from all around the globe. We continue to pursue our mission to democratize quant and help you unlock alpha. Wes is currently the Executive Managing Member of Empiritrage.

Fortune has an interesting article on Warren Buffett’s performance over the past 5 years (12/31/2008 through 12/31/2013)

Furthermore, though Buffett doesn’t specifically talk about this in his annual letter to shareholders, these results capped a five-year period, year-end 2008 to year-end 2013, in which the S&P 500 beat Berkshire’s gain in book value per share — the first such period in Berkshire’s history. For the five years, the S&P index jumped 128%. Berkshire’s book value per share rose by only 91%. Source:http://finance.fortune.cnn.com/2014/03/01/buffett-berkshire-hathaway-earnings/

We did our own analysis of the past 5 years. The Berkshire letter states the following book value growth percentages for the past 5 years (ending December 31, 2013):

2009: 19.8%

2010: 13.0%

2011: 4.6%

2012: 14.4%

2013: 18.2%

The source for Buffett’s returns–the annual letter.

These returns correspond to total return of 91.47% and a compound annual growth rate of 13.87%.Not bad!

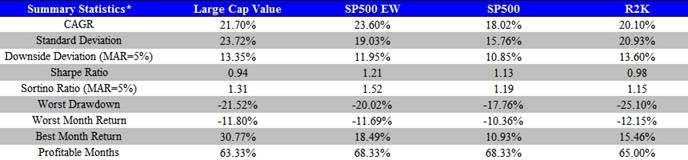

Below we post the following asset classes from 12/31/2008 through 12/31/2013:

Large Cap Value = The top market cap and top B/M quintile Fama French equal-weight portfolio

Source: Ken French’s website)

S&P 500 EW = S&P 500 Equal-Weight Index Total Return Index

Source: Bloomberg

S&P 500 = S&P 500 Total Return Index

Source: Bloomberg

R2K = Russell 2000 Total Return Index

Source: Bloomberg

Buffett lagged the S&P 500 by nearly 400bps. That is fairly tragic. But how about arguably more appropriate benchmarks such as the large cap value index or the S&P 500 equal-weight index? Buffett tilts cheap and he position sizes more akin to equal-weighting than he does towards market-cap weighting (see: http://www.cnbc.com/id/22130601) Buffett loses by 8-10%+ a year. That IS tragic.

This is not a message saying Warren Buffett is a clown. We have clearly cherry picked a 5-year period where Buffett “lost his touch,” but the long-haul record of Buffett is undeniable: Buffett is a certifiable investment stud for the ages. If I could have his children, I would. So what is the point of highlighting Buffett’s Berkshire Beatdown? We think this is a chance for all of us to eat some humble pie. Buffet’s underperformance is a reminder that investing is incredibly difficult and even over a relatively long horizon the greatest managers/strategies can endure a pain train. We have first-hand insight on this cruel reality, because we crank the numbers on every strategy fathomable and there is no such thing as a strategy that works “all the time.” All the best systems have drawdown events and 5yr periods (sometimes 10yr periods) where they underperform the benchmark. The strategies that don’t have these characteristics can be sold by Bernie Madoff and Associates. Good luck with that. Buffett has been, currently is, and always will be an investment genius who can create value above and beyond a market-cap weighted passive index. I truly believe that. However, he still has to play in the same universe we play in. A universe filled with massive volatility, uncertainty, and fickle psychology. How’s the humble pie taste? Mine is excellent.