Currency Zone Defies Mainstream Economics Profession With Continued Controversial Policies

March 13, 2014 Leave a comment

Why Euro-Zone Chiefs Buck the Trend

Currency Zone Defies Mainstream Economics Profession With Continued Controversial Policies

SIMON NIXON

March 9, 2014 4:58 p.m. ET

The euro zone is used to being criticized by the mainstream economics profession.

Since the start of its debt crisis, the currency union has been attacked for imposing too much fiscal austerity, for failing to create jointly guaranteed euro-zone bonds and for refusing

to directly recapitalize weak banks from common euro-zone funds.

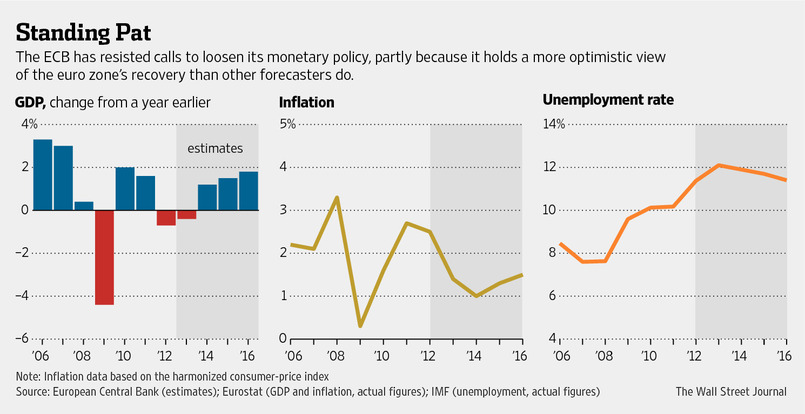

Even now that the economy is recovering, its policies remain controversial. Last week, Christine Lagarde, the managing director of the International Monetary Fund, called yet again for the euro zone to loosen both fiscal and monetary policy to boost demand to head off the threat of deflation. Many in the U.S. government and U.S. Federal Reserve share her concerns, as do many economists. One might call it the new Washington Consensus, albeit this time based on neo-Keynesianism rather than the neo-Liberalism of the 1990s.

Yet the euro zone has again ignored the advice. Despite weak growth, low inflation and high unemployment, the European Central Bank last week left its monetary policy unchanged, dashing hopes that it would follow the Fed and other major central banks in embarking on a major bond-buying program or announce a package of cheap loans for banks.

What explains Europe’s continued rejection of mainstream economic thinking?

One answer is that the ECB simply doesn’t share the IMF’s gloomy analysis. Core euro-zone inflation in February is estimated to have been 1% compared with 0.8% in January, and the ECB has raised its growth forecasts to 1.2% this year and 1.5% in 2015. Although it expects inflation to remain very low for the next two years, only reaching 1.7% in the fourth quarter of 2016, the ECB doesn’t believe the euro zone will tip into outright deflation.

It reckons that two-thirds of the fall in inflation since early 2012 is attributable to lower energy prices and that the appreciation of the euro since 2012 has reduced inflation by 0.5 percentage points. Falling prices are anyway part of the crisis-country adjustment process—the so-called internal devaluation—and can help the economy by boosting spending power. It would make no sense for the ECB to lean against this sort of disinflation.

Of course, this doesn’t tell the full story. After all, the IMF thinks the ECB should embark on quantitative easing even if outright deflation is likely to be avoided, since even low inflation can be harmful as it makes it harder for crisis countries to bring down debt-to-GDP ratios or to regain competitiveness. If wages are stagnant in Germany, then workers elsewhere will struggle to become relatively more competitive without politically difficult wage cuts.

But even though many euro-zone policy makers share these concerns, there are practical, political and philosophical obstacles to loosening fiscal and monetary policy. These relate to the nature of the currency union.

Take fiscal policy: Any scope for looser policy is limited by the euro zone’s tough fiscal rules. These rules and the new mechanisms for budgetary oversight may not make sense from a Keynesian demand-management perspective, but that misses the point. Binding fiscal rules have played a vital role not only in convincing the markets that countries are serious about paying down debt but also in persuading member states to agree to vital steps toward greater integration, such as the creation of a banking union or common bailout funds.

It has been the willingness of Greece, Portugal and Spain to do “whatever it takes” as much as the ECB that has ensured the euro’s survival. Sure, there is plenty of scope to make fiscal policy in many countries more growth-friendly—shifting the balance between tax rises and spending cuts and raising indirect taxes to fund cuts to taxes on labor—but there is little appetite in the euro zone to loosen its fiscal targets.

Similarly, the bar for QE in the zone is set very high. That’s not just because credit risks on acquired assets must be shared among member-state taxpayers, but because the risk of moral hazard is higher in a currency union. The ECB’s offer of cheap loans reduced the pressure on regulators and governments to recapitalize weak banks. Similarly, once the ECB starts buying government bonds, pressure to cut debts and reform broken economic models is sure to ease, leaving the ECB at the mercy of profligate governments.

Indeed for many euro-zone policy makers, the risk that countries will abandon reforms outweighs the risks associated with low inflation. This is the key economic point of difference with the Washington Consensus. Of course, most Keynesians insist they recognize the importance of supply-side reforms—Ms. Lagarde referred to them in her speech last week. But throughout the crisis, many have tended to treat them as secondary to macroeconomic policy best left until the economy is stronger.

But Europe’s structural rigidities aren’t a secondary issue. One reason why the recession was so deep is that rigid labor and product markets, excessive bureaucracy and inefficient justice systems prevented the reallocation of resources. As Greece’s central-bank governor, George Provopoulos, acknowledged in a speech last month, the reforms Greece has undertaken during the crisis have been overdue for decades. The reforms being discussed in France and Italy are equally overdue.

Long term, the euro zone’s prosperity depends on boosting productivity and fostering investment and innovation; if short-term steps to boost demand undermine those efforts, then economic imbalances will worsen—once again destabilizing the currency.

That means that the euro zone’s recovery is likely to be slower, and unemployment is likely to remain higher than if it were to find a way to overcome the practical obstacles and follow the Keynesian prescriptions. Or at least, that is what most macroeconomic models predict. But then those models are based on neo-Keynesian theories that have proved to be far from robust both before and during the crisis.

Indeed, those models have consistently underestimated the recovery in Europe over the past year; estimates of Spanish GDP growth this year have doubled in six months to about 1% and some in the Spanish government now privately believe growth this year could hit 1.5%. It wouldn’t be the first time the Washington Consensus was wrong.