| Dear Friends and All,

Emergence of Mittelstand Compounders in Asia? The Case of PT Selamat Sempurna

It was a busy day on March 11 at the grave of a hero in Blitar, a city located right at the foot of the explosive Mount Kelud, and 167 kilometers from the East Java capital of Surabaya city, Indonesia. Megawati, daughter of Indonesia’s first president Soekarno, and Jakarta’s governor Joko “Jokowi” Widodo went together to visit Soekarno’s grave to pay their respects to the independence fighter of the world’s third biggest democracy with a trillion in GDP, or the near-equivalent of South Korea or China’s Guangdong province. Two days later on March 13, Megawati announced Jokowi, the furniture-seller who first became the mayor of the ancient Javanese city of Solo and later Jakarta, as the party’s presidential candidate for the July 9 elections.

On March 13, we have the privilege of having lunch together with our Moat Report Asiasubscriber Frederick Sturm, managing director at the Singapore office of the Austrian private banking empire Valartis Group, and Frederick’s wife Dr Monika Patricia Sturm who’s a successful, intelligent and modest value investor. Over at the Singapore Management University (SMU), the Omaha of Singapore far away from the speculative crowd and syndicates, we discussed whether in the rent-seeking and crony-capitalist economies of developing Asia, such as Indonesia and China, can Asian family businesses emulate the success of Germany’s mighty Mittelstand and hidden global champions in compounding value. We also express the desire to catch up again at the 11th Value Investing Summit July 2014 in Molfetta, Italy, in the lovely Bari/Puglia region in which we are invited as one of the keynote speakers to share our Bamboo Innovator investment framework and our biggest mistake with over 100 value investors from all over the world. We will also be presenting on 28 Mar to a group of around 200 value investors in Singapore.

Top left: Jakarta Governor and Indonesian Democratic Party of Struggle (PDI-P) presidential candidate Joko “Jokowi” Widodo bows to party chairwoman Megawati Soekarnoputri after receiving a piece of a ceremonial yellow-rice cone during the 41st anniversary of the PDI-P in Jakarta; top right: Soekarno statue and grave on the back where the gapura (gateway) is. Bottom: Eddy Hartono of ADR Group and PT Selamat Sempurna (SMSM IJ) – Stock Price Performance, 1996-2014

<Article snipped>

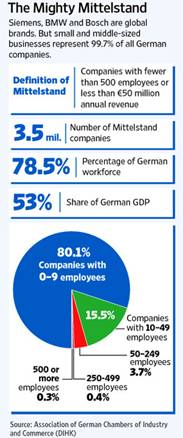

Germany’s Mittelstand, the more than 3.5 million small and midsize family enterprises employing more than 78 percent of workers and contributing more than half of the country’s GDP, forms the backbone of Germany’s resilient export-driven economy. The Mittelstand traces its roots to the Middle Ages, when the country that is now Germany was divided into hundreds of states. Competition between them created a number of industrial regions with their own educational institutions, banks and political administrations. This is very different from the centralized economies such as in France. WWII cemented the Mittelstand’s importance, as big corporations were tainted by their association with the Nazis and often based in big cities destroyed by allied bombing. The Mittelstand had to export early on, given that some German states were smaller than two football fields.These agile creatures darting between the legs of multinational monsters are dominant global players insophisticated, hard-to-imitate niche products and valuable critical niches that are largely invisible to the average consumer. While BMW (BMW GR), Audi (NSU AG), enterprise software giant SAP AG (SAP GR), Adidas (ADS GR), Hugo Boss (BOSS GR), Robert Bosch, consumer giantsBeiersdorf (BIE GR) and Henkel (HEN GR), dialysis giantFresenius (FRE GR), pharmaceuticals giant Bayer (BAYN GR), chemicals giant BASF (BAS GR), industrial gas specialist Linde AG (LIN GR), truck and engine maker MAN SE (MAN GR), Siemens (SIE GR) are well-known names, there are quiet resilient compounders that fit the Bamboo Innovator framework, including commercial kitchen equipment company Rational AG (RAA GR), eyewear specialistFielmann (FIE GR), KSB (KSB GR) pumps, women’s fashion Gerry Weber (GWI1 GR), specialty chemicals specialists Brenntag (BNR GR), K+S AG (SDF GR) and Lanxess (LXS GR), Kärcher high-tech cleaners, Würth group (the Fastenal of Europe), auto gasket maker Elringklinger (ZIL2 GR), flavor and fragrance specialist Symrise (SY1 GR), electronic payment specialist Wirecard (WDI GR), lab solution specialist Sartorius (SRT GR), medical vision technology specialist Carl Zeiss Meditec (AFX GR), engineering specialist Bilfinger (GBF GR), packaging and bottling machine maker Krones (KRN GR), cable specialist Leoni (GR), metalworking specialist Schuler (SCUN GR), medical products Paul Hartmann (PHH2 GR), DIY home improvement specialist Hornbach Baumarkt (HBM GR) and so on. Germany’s Mittelstand, the more than 3.5 million small and midsize family enterprises employing more than 78 percent of workers and contributing more than half of the country’s GDP, forms the backbone of Germany’s resilient export-driven economy. The Mittelstand traces its roots to the Middle Ages, when the country that is now Germany was divided into hundreds of states. Competition between them created a number of industrial regions with their own educational institutions, banks and political administrations. This is very different from the centralized economies such as in France. WWII cemented the Mittelstand’s importance, as big corporations were tainted by their association with the Nazis and often based in big cities destroyed by allied bombing. The Mittelstand had to export early on, given that some German states were smaller than two football fields.These agile creatures darting between the legs of multinational monsters are dominant global players insophisticated, hard-to-imitate niche products and valuable critical niches that are largely invisible to the average consumer. While BMW (BMW GR), Audi (NSU AG), enterprise software giant SAP AG (SAP GR), Adidas (ADS GR), Hugo Boss (BOSS GR), Robert Bosch, consumer giantsBeiersdorf (BIE GR) and Henkel (HEN GR), dialysis giantFresenius (FRE GR), pharmaceuticals giant Bayer (BAYN GR), chemicals giant BASF (BAS GR), industrial gas specialist Linde AG (LIN GR), truck and engine maker MAN SE (MAN GR), Siemens (SIE GR) are well-known names, there are quiet resilient compounders that fit the Bamboo Innovator framework, including commercial kitchen equipment company Rational AG (RAA GR), eyewear specialistFielmann (FIE GR), KSB (KSB GR) pumps, women’s fashion Gerry Weber (GWI1 GR), specialty chemicals specialists Brenntag (BNR GR), K+S AG (SDF GR) and Lanxess (LXS GR), Kärcher high-tech cleaners, Würth group (the Fastenal of Europe), auto gasket maker Elringklinger (ZIL2 GR), flavor and fragrance specialist Symrise (SY1 GR), electronic payment specialist Wirecard (WDI GR), lab solution specialist Sartorius (SRT GR), medical vision technology specialist Carl Zeiss Meditec (AFX GR), engineering specialist Bilfinger (GBF GR), packaging and bottling machine maker Krones (KRN GR), cable specialist Leoni (GR), metalworking specialist Schuler (SCUN GR), medical products Paul Hartmann (PHH2 GR), DIY home improvement specialist Hornbach Baumarkt (HBM GR) and so on.

All of these Mittelstand hidden champions radiate the EKS element in their business model. EKS stands for Engpass konzentrierte Strategie, inspired by an unconventional German management thinker Wolfgang Mewes who promoted a “bottleneck-focused strategy”. Essentially, EKS suggests that the key to success is to concentrate all resources, however limited, to solve a specific “burning problem” (the bottleneck) for a well-defined customer group…

<Article snipped>

The key difference between Mittelstand bamboo innovators and the Asian firms that determine the scalability of the business models lie in the fact that most Asian firms have…

<Article snipped>

Established in 1976, PT Selamat Sempurna (SMSM IJ, MV $460m), part of the ADR Group, is the largest auto filter manufacturer in Indonesia…

<Article snipped>

As Eddy Hartono discovers the power of Mittelstand EKS focus in solving its customers’ burning problems, shareholders’ value has compounded by 16-fold since 2000 with the long-term potential to continue to grab a larger share of the $50 billion filtration market ($16 billion target market for HD engine/mobile, industrial air, automotive and industrial hydraulics) and “to give the customer a better choice”:

“Finding solutions through our products and services through improvements in efficiencies while proactively working with our customers and suppliers to give the best value, on a global basis, is the alternative we are seeking. This involves investing in Human resources, technology, latest manufacturing processes, software, communication and others which would bring enormous tangible and intangible values to ADR Group, at the same, bringing the customer close. We at ADR Group would continue to work hard and explores opportunities in order to create addedvalue so that we can stand by our motto ‘To Give the Customer a Better Choice’.”

To read the exclusive article in full to find out more about the story of Eddy Hartono’s PT Selamat Sempurna; the origins of German Mittelstand compounders and their similarities and differences with Asian firms; and how to identify the Asian Mittelstand hidden global champions, please visit:

|

|

“In business, I look for economic castles protected by unbreachable ‘moats’.”

– Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxyand The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

- Individual subscription at $1,994 per year:

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of March investigates the Middleby of Asia commanding a dominant market share of over 80% in hypermarkets, 50% in chain outlets, 30% in 4- to 5-star hotels in China and an overall 30% in its home market. Yet, no single customer accounts for more than 5% of its revenue. Just to recall for value investors, NYSE-listed Middleby, with its sleepy and boring business, has compounded 100-fold from around $50m to $5.7bn since its tipping point in 1999. The founders of this Asian family business demonstrated clear dedication in building up the company with its wide-moat business model backed by a strong and unique distribution/marketing network in finding, winning and binding new customers to build massive brand equity and long-lasting relationships with clients over time. Their devotion to its core product for nearly 20 years results in maximum problem-solving skills, innovative strength and product leadership and hence, to ever greater customer benefit that will protect the company to consolidate the fragmented market and provide ample opportunities to continue its profitable growth. The company is currently trading at PE13e 15.8x and an undemanding EV/EBIT 10.1x and EV/EBITDA 9.5x and its growth potential based on its unique business model is not priced in. There is a structural re-rerating of niche business models with (1) diversified client base, (2) steady revenue streams, (3) lean capex requirements that creates ample free cashflow and defensive growth. Based on PE, P/CFO and EV/EBIT, the company is trading at a 40-50% discount to the foreign listed comparables despite more efficient use of assets in generating profits and cashflow. It has an attractive 7% earnings yield growing at 20% over the next 3-5 years and a 3.8% dividend yield that is supported by its strong cashflow generation ability, steady revenue stream and lean capex requirements to limit downside risks in valuation. Based on the growth plans to penetrate new product and customer segments; build its third plant in India in addition to the ones in its home market and in China; and potential bolt-on acquisition opportunities with its healthy balance sheet in net-cash position, it has the potential to double its operating cashflow in the next 3-5 years and market value could double, representing an upside potential of 100-140%.

Our past monthly issues examine:

- An emerging Asian Walgreens which is a top 3 community pharmacy operator in its home market. Walgreens is a classic neglected American compounder up over 272-fold to $54 billion from under $200m as it quietly consolidates the market. Over the decade, we observed that it is difficult to scale services-based businesses without an entrepreneurial mindset, committment and execution and the bold and unique management system of the company since 2000 allowed the pharmacists to be part-owner of the business which will lead to increased level of commitment and an owner’s mindset in growing the business for the long-term in the community. The firm has strong cash generation ability due to its negative cash conversion cycle (CCC) in the business model to help the business stay resilient during difficult times and to fund capex needs internally without straining the business model scalability as the network expands. The centralized logistics system provide regular deliveries to all of its community pharmacies enables the outlets to maximize retail space without the need to have space to keep stocks. This also enables the community pharmacies to optimize retail space to carry a wide range of products which is important as consumers increasingly have top-of-mind recall for the company as the destination to go to for their healthcare needs. Like Walgreens, the company believed in the power of embedding technology into the business model to better compete and its financial and warehousing/inventory management systems are integrated with its in-house POS (point-of-sale) system which is linked among all its community pharmacies and head office via virtual private network. The company is founded by five college friends who were somewhat frustrated that their pharmacy degrees were underappreciated and under-rewarded as compared to their medical degree counterparts even though they had studied hard for 4-5 years and had in-depth medical knowledge. They were eager to prove themselves that they are as capable, if not more so. This restless spirit to prove their capabilities resulted in them coming together to be entrepreneurs and they wish to provide the platform for similar restless pharmacists to apply their hard-earned knowledge acquired in the university. We find that this common purpose and camaraderie spirit is rare in Asian companies and makes the company unique to scale up sustainably. The company is currently trading at a EV/EBIT of 13.9x and EB/EBITDA 12.6%. In the next two to three years as the company expands its network of outlets, operating cashflow (CFO) could increase 50-60% and a re-rerating could result in a doubling in market value.

- An Asian-listed pharmaceutical company which has a dominant franchise in a neglected but growing disease and is a leader with a domestic market share of 49% in this niche segment and is the only fully-integrated player amongst the few pre-qualified WHO firms, giving it >30% EBITDA margin, better pricing power compared to the competition, and significant advantage over other players in ramping up the global business from the current 30% market share in the most-common treatment drug (vs Novartis 50%). Furthermore, the pharma company has the second-highest GP/TA (gross profit/ total asset) ratio in the industry at 56.3% and the most conservative accounting practice in the industry which “depresses” earnings relative to its peers i.e. it is the only domestic firm which expenses, and does not capitalize, all R&D. With the new plant for formulations export to US, the deepening of the niche drug franchise, growing wins in chronic pain and other niche areas and the commercialization of the potential blockbuster product of blood thinner by FY16/17, EBITDA could potentially double to $200m in the next 4-5 years, triggering a valuation re-rating to a market value of $3.4bn, a 130% upside.

- An Australian-listed company with market value $405m, EV/EBITDA 7.5x, EV/EBIT 10x, div 3%, 70% domestic market share whose management made the controversial bold decision to stop overseas exports in order to focus on cultivating the higher-margin domestic market with innovative marketing strategy and new products and is potentially doubling its supply in the next 3-5 years. It is in its 10th year of listing after piling the foundation in consolidation, investment, rationalization for its next stage. It has an all-time low debt-equity position 18.6% with healthy balance sheet. “Buffett of Nordic” recently increased position between Apr-Sep this year in the peer comparable of the company and the billionaire investor announced in Nov an acquisition of a rival in a wave of global consolidation and with the view on a sustained recovery in product prices.

- A Northeast Asia-listed company with global #1 market share leadership in 4 different products, including making the components for an innovative consumer product whose sales have climbed from $90 million to $526 million in the recent three years. The company is a hidden global consolidator with underappreciated growth. The stock is trading at PE 11.5x, EV/EBITDA 9x and generates a sustainable dividend yield 5.75%.

- A Taiwan and Southeast-Asian-listed entrepreneurial company, both with a dominant 80% domestic market share and have innovative business models to generate substantial cashflow to support both expansion and a 4-5% dividend yield.

- There is also a behind-the-scene conversation with the CEOs of the companies to understand their thinking process in building up the business.

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our existing institutional subscribers from North America, Europe, the Oceania and Asia,including professional value investors with over $20 billion in asset under management in equities, secretive Singapore-based billionaire entrepreneur who’s a super value investor and successful European multi-billion family offices. Questions range from:

- The nuances of internal dealings in Asia, including the case discussion of the recent deal in which HK billionaire’s Lee Shau-kee Henderson Land acquiring Towngas or Hong Kong & China Gas (3 HK) from his family holdings, seemingly déjà vu from the early Oct 2007 transaction when the market peak.

- The case of F&N Singapore spinning out its property unit FCL Trust and getting “free” special dividend-in-specie and the potential risk in asset swap restructuring to deleverage the hidden debt in the entire Group balance sheet.

- The dilemma of whether to invest in a Southeast Asian-listed company and hidden champion with a domestic market share of 60% due to family squabbles and a legal suit over the company’s ownership.

- Discussion of the wise and thoughtful 107-year-old Irving Kahn’s investment into a US-listed but Hong Kong-based electronics company with development property project in Shenzhen’s Qianhai zone and the possible corporate governance risks that could be underestimated or overlooked, as well as their history of listing some assets in HK in 2004.. This is also a case study of “buy one get one free” in John’s highly-acclaimed book The Manual of Ideas in which the “free” property is lumped together with the (eroding) core business to make the combined entity look cheap and undervalued. What are the potential areas that value investors need to watch out for when adapting the SOTP (sum-of-the-parts) valuation method in Asia?

- And many more intriguing questions.

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|