Small proves beautiful at boutique banks

March 21, 2014 Leave a comment

Last updated: March 16, 2014 2:22 pm

Small proves beautiful at boutique banks

By Ed Hammond in New York and Daniel Schäfer in London

On an August evening in 2012, Jim Mooney and Mike Fries gathered for an informal dinner at the Hamptons house of Aryeh Bourkoff, the Wall Street dealmaker. Mr Bourkoff, who had launched his own investment bank LionTree a month earlier, had chosen his guests carefully.

Over sake and cigars, he floated the idea of the two men combining the cable companies they respectively headed, Virgin Media and Liberty Global. The $23bn deal was completed within six months, with LionTree credited as Liberty’s lead adviser.

LionTree is one of a growing band of independent investment banks taking a share of the US merger and acquisition fee pool, once the preserve of Wall Street’s largest financial institutions. Their success reflects a rejection by international corporations of the notion that the size of a bank’s balance sheet correlates with the quality of its advice.

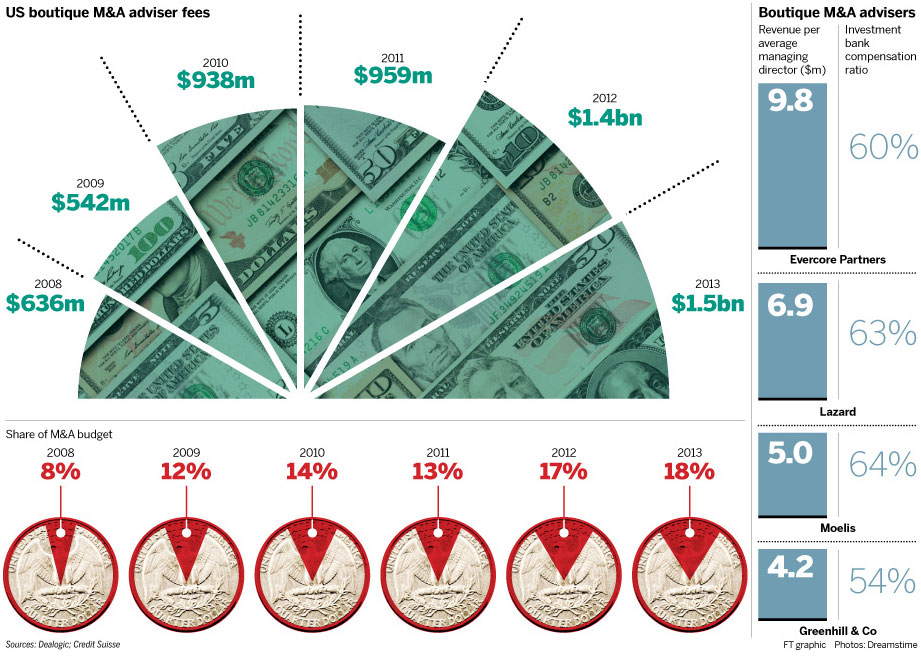

In 2013, independent investment banks, or advisory boutiques as they are often called, took close to 20 per cent of US M&A fees and collected about $1.5bn in revenues. That market share, more than double the 8 per cent achieved in 2008, means that seven of the top 20 M&A fee earners are now independent advisers, according to data from Dealogic.

That swing was highlighted this month when Moelis, the boutique founded by the former UBS banker Ken Moelis in 2007, announced plans for an initial public offering that will value it at close to $2bn.

Blair Effron, one of the founders of the independent investment bank Centerview Partners, says the rise of boutiques has been predicated on their ability to work closely with a much smaller client base. “We are around our clients all the time, not just when they are doing transactions, and try to go as deeply as we can to understand their businesses.”

Centerview is working on the largest announced deal of 2014, Comcast’s $45.2bn merger with Time Warner Cable, and last year it racked up lead credit for the $23bn buyout of Heinz, backed by Warren Buffett.

In the wake of the global financial crisis, independent advisers touted their services using the argument that they were free from the conflicts of interest suffered by its larger rivals, which also used their balance sheets to finance deals. Today, with practices such as “staple” financing scarce, that thesis carries less weight.

“The balance sheet plays less of a role in deals, which means advice and human capital have become a more wanted quantity,” says Ashley Serrao, a banking analyst at Credit Suisse.

Operating underneath the radar

When Simon Robey left Morgan Stanley early last year to set up his advisory boutique, City bankers quipped that all he had done was move his office from London’s mundane banking centre of Canary Wharf to the upmarket district of Mayfair,writes Daniel Schäfer.

The strength of Mr Robey’s relationships with some of the UK’s biggest company boardrooms – cultivated over 25 years at Morgan Stanley – is such that many of his clients would follow him wherever he went.

The tilt towards seeking advice from specialist M&A advisers rather than defaulting to one bank for all a company’s financial needs points to an increasingly fragmented professional services landscape. In the case of the banking sector, it also illustrates the migration of talent from bulge-bracket lenders to smaller operations, removed from the regulatory and political wrangling that has dogged big banks since the start of the financial crisis.

As a result, the sector has become increasingly tiered. The umbrella term “advisory boutiques” fails to offer a true picture of the range, from one-man bands to powerhouses such as Rothschild and Evercore.

At one extreme is Lazard. Too large to be categorised as a boutique, it alone occupies a middle ground between the other independents and the titanic M&A practices of bulge-bracket banks such as Goldman Sachs and Morgan Stanley.

At the opposite end of the spectrum sits Paul Taubman, who quit Morgan Stanley in 2012. He has gone on to act as a self-employed adviser on two of the largest deals of the past decade: Verizon’s $130bn takeover of its wireless joint venture with the UK’s Vodafone and the Comcast/Time Warner Cable merger. He told the Financial Times in a recent interview he was merely enjoying retirement.

The larger independent banks, such as Evercore, Moelis and Greenhill, have attracted big talent in recent years. Almost half of the 30 largest deals announced in 2013 involved an independent adviser.

“Who wants to spend the first 20 minutes of every client call justifying something that has happened at the parent company?” asks one banker who recently made the transition from a large Wall Street bank to an independent firm.

The chief executive of a rival boutique argues, though, that the big banks’ falling share of the M&A market represents a more fundamental shift in Wall Street’s priorities. “Post-crisis, the skill set needed to survive was not the same as is needed for M&A. Wall Street needed people who understood risk management and credit derivatives, not relationships.”

But it is among the smaller boutiques, including Blackstone Advisory Partners and Centerview, that the real boom is occurring.

Relationships are key to deals

In the first few days of 2014, Centerview Partners helped Jim Beam, the US spirits group, sell itself to Suntory of Japan for $16bn. A month later, the investment bank cropped up on the list of advisers to have secured Time Warner Cable’s $42bn sale to Comcast, writes Ed Hammond.

The deals marked the closing of a circle Blair Effron (above) and Robert Pruzan, the Wall Street dealmakers who founded Centerview eight years ago.

The thriving US boutique sector has not yet been replicated in Europe, where the continent’s scattered markets and generally lower fee levels have kept independent investment banks further from the mainstream.

Rainmakers in the City of London such as Simon Robey and Simon Warshaw, who have teamed up in the “advisory kiosk” Robertson Robey Associates, prefer to work with a handful of exclusive clients while staying below the radar. The two brothers Michael and Yoel Zaoui, who were in senior M&A positions at Morgan Stanley and Goldman Sachs before setting up on their own, have a similar strategy.

But the same lack of scale that helps independents get established can prove problematic in the long term. The smaller the bank, the greater the so-called “key man risk”, where the reputation, and therefore earnings, of the business are dependent on one or two names associated with the bank. Be it Roger Altman at Evercore, Mr Moelis or John Studzinski at Blackstone, the success of each boutique depends heavily on a few powerful rainmakers.

So important are these individuals to the franchise they head that clients will often build in key man clauses into letters of engagement, meaning that a contract will be void if a certain individual leaves the boutique before the deal is complete.

There is also the difficulty of how to grow. “I cannot scale my business because I cannot hire enough of the quality of people needed,” says Mr Studzinski. “In a boutique you don’t have the balance sheet and product suite to fall back on, so you need people who already have serious, trusted relationships who can bring in business and a network from the start – that’s a rare person.”