Part 1: Apple Watch and The Digital Pulse From Asia

September 21, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | September 15, 2014 |

Bamboo Innovator Insight (Issue 50)

|

| Apple Watch and The Digital Pulse From Asia

What can the Apple Watch do that the iPhone can’t?

The most “wow” that Tim Cook elicited in his launch of the Apple Watch last Tuesday was a Starwood app that will let you bypass the check-in queues and check into a hotel room by just waving your Apple Watch to open the door of the properties which include the Westin, Sheraton, W and so on.

The answer to the elusive “killer-app” for smartwatches – the feature that will make them indispensable in people’s lives – will unlock the estimated value of the $93-billion wearable devices market, of which smartwatches are believed to account for two-thirds of the value. There is, however, growing disillusionment on the prospect for wearables: Nike has already abandoned its initially-promising Fuelband unit which ran up $60m in sales in 2013 andeBay has been flooded with Samsung Galaxy Gear smartwatches which clocked in $240m in sales last year.

Instead of thinking about Apple Watch as a stand-alone product that Swiss watchmakers scoffed at, imagine if the Apple Watch can work together with the iPhone to do a two-factor authentication for payments to replace your wallet, including new things that the two connected devices can do together. As Apple assumes a more central role in the financial universe with its Apple Pay service that uses the near-field communication (NFC) to exchange information wirelessly between devices, the 50-year-old antiquated credit card system might be transformed and new types of transactions previously done with cash and other payment methods might be processed, creating a new wave of demand. “It’s all about the wallet. Our vision is to replace this,” Tim Cook warmed up the crowd. Visa,MasterCard and American Express – who account for 83% of all credit card volumes in US – are all signed up for the Apple Pay launch, including a significant number of merchants including Starbucks, Disney, Whole Foods,McDonald’s.

The Apple Watch is the company’s first major advance into a new product category since the iPad in 2010. Apple was not exclusively about the discovery and commercialisation of the innovative new products from iPod (unveiled in October 2001), iPhone (June 2007) to the latest iPad (April 2010). Its wide-moat success comes from wrapping the new products around the “emptiness” of deep know-how to provide game-changing portable digital lifestyle experience to the consumer by combining hardware, software, service, and an ecosystem of partners, making downloading of digital music, video, games and apps via iTunes Store (since April 2003) easy and convenient. Imitators of the hardware all burn down because they fail to appreciate and replicate the amount of deep thoughts, details and executions that go into integrating the device into the lives of the consumer.

The potential winners in the vast Apple supply chain in Asia will also be in focus. However, there are cautionary tales for value investors. Currently, these Asian suppliers include main assembler Quanta Computer (2382 TT, MV $10.3bn), packaging and testing company ASE (2311 TT, MV $9.5bn), power control IC designer Richtek (6286 TT, MV $770m), IC substrate company Kinsus (3189 TT, MV $1.7bn), flexible printed circuit board Career Tech (6153 TT, MV $439m), electro-acoustic components makers Merry (2439 TT, MV $1bn), AAC (2018 HK, MV $7.5bn) andGoerTek (002241 CH, MV $6.9bn), GPS system RoyalTek (3306 TT, MV $75m), quartz crystal and clock control modules TXC (3042 TT, MV $427m), curved flexible AMOLED display screen from LG Display (034220 KS, MV $12bn).

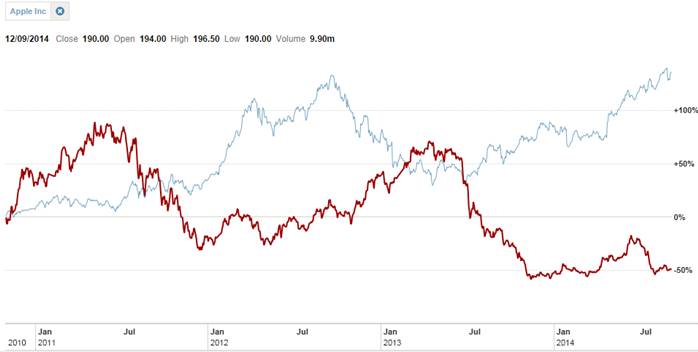

Should you invest in Apple or attempt to pick its winning Asian suppliers, especially when Apple is now the world’s most valuable company with a dizzying $608-billion market cap? A cautionary tale comes from TPK Holding (3673 TT, $2.1bn), the world’s largest touch panel vendor, which generates around 41% of its revenue from Apple. TPK was an early beneficiary of the iPhone, providing…

<Article snipped>

TPK Holding (3673 TT) Vs Apple (AAPL US) – Stock Price Performance, 2010-2014 Apple Watch invoked an interesting twist to the fabled tale of how cheap, accurate quartz watches from Japan’s Casio and Seiko in the 1970-80s put many traditional mechanical Swiss watchmakers into bankruptcy. Within a decade of inventing the first quartz watch, the Swiss saw their export volume decrease from 45% to 10% of watches produced globally. By 1983, two-thirds of all watch industry jobs in Switzerland had vanished and over half of all watchmaking companies in Switzerland had gone bankrupt. Swatch Group’s Nicholas Hayek and LVMH watch president Jean-Claude Biver repositioned mechanical watches as luxury and self-identity pieces and the Swiss watch industry no longer competes on the same dimensions as quartz watches.

Apple Watch is a new twist as quartz crystals are key components in frequency generation and control devices for signal timing in smartphones and smartwatches. If the Qualcomm chip is the smartphone’s heart, then the quartz crystal component would be the delivery system, which supplies blood (digital signals) to every part of the body (product). The unassuming quartz crystal serves as the “pulse” of the digital products, propelling all personal computers, digital cameras and mobile phones. The digitization of auto electronics has increased the demand for quartz crystal components from 4 per car to over 40. For mobile phones, that figure has increased from 1-2 per phone to 4-5 per phone, and quartz crystal components are becoming ever smaller and more intricate.

Of the 700m smartphones globally, one of the five uses the quartz crystals produced by Taiwan’s TXC (3042 TT, MV $427m), who overtook Japan’s KDS in April 2013 to become the third largest quartz crystal component maker in the world, only behind Seiko Epson (6724 JP, MV $10.1bn) and NDK (Nihon Dempa Kogyo) (6779 JP, MV $185m). TXC also accounts for 75% of the quartz crystal components of Apple’s mobile devices and its customers also include all the top brands such as Samsung, HTC, Huawei, ZTE etc. TXC currently has 3 production plants in Taoyuan, China’s Ningbo and Chongqing. Its 200+ automated production lines churn out 260m+ monthly quartz crystals. TXC expanded its R&D team six times to 400+ engineers in 10 years, accounting for 20% of the workforce at its Taoyuan factory. Mobile communications remain the largest contributor to TXC at 35% of revenue. New growth applications include motion sensors and bio sensors. Interestingly, since iPhone was launched in June 2007, Apple is up nearly 6-fold while TXC is flat. TXC generates $31m in profits from $316m in sales last year with a ROE of 11.2% and ROA of 7.2%. TXC trades at around PE 11.7x, P/Book 1.6x, EV/EBIT 14.1x, EV/EBITDA 7.3x and a dividend yield of 5.3%.

For a long time, the Japanese dominated with 80% of the global market for quartz crystal components. How did two brothers – Paul Lin Jin-biao and Peter Lin Wan-xin from a Taiwanese farming family break the Japanese monopoly to make TXC third in the world?

<Article snipped>

Warm regards, KB Managing Editor

The Moat Report Asia SMU: http://accountancy.smu.edu.sg/faculty/profile/108141/Kee%20Koon%20Boon

To read the exclusive article in full to find out more about the story of the implications of Apple Watch on the Asian supply chain and the story of Taiwan’s TXC, please visit:

|

| The Moat Report Asia |

| “In business, I look for economic castles protected by unbreachable ‘moats’.”– Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produceThe Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of August investigates an Asian-listed company who’s the leading ecommerce group in its home country with the complete platform coverage in the Amazon-type of B2C ecommerce of selling directly to end consumers (Sales/Net Profit: 90%/78%), Rakuten-type of B2B2C platform (Sales/Net Profit: 4%/12%) to support the online SME merchants who in turn sell to the end consumers, and the eBay-type of C2C auction site (Sales/Net Profit: 2%/21%) where individuals buy and sell to one another. This “Amazon-Alibaba” is highly profitable with recurring free cashflow (FCF yield 4.6-5% compounding at 25% in the next 3-5 years) bypioneering the world’s-first 24-hour delivery promise and guarantee when world-class logistics experts said it cannot be done. In emerging markets and Asia where logistics costs is 15-20% of GDP, most ecommerce companies fail to scale up due to lack of fulfillment capabilities and inventory risk became the killing blow as they pursue growth without the intangible know-how. The company designs and builds its own warehouses to provide fast and efficient delivery with 99.68% on-time rate and also complete backend services to suppliers, widening the gap between itself and peers. With its superior infrastructure, the company is able to provide consumers a one-stop shopping experience with all goods purchased from different vendors packaged into a single box and delivered to the client’s door. The company has consignment agreements with suppliers which allow it to have control over inventory management but carry no liability of inventory on its balance sheet, in other words, there is minimal inventory riskfor the company to scale up sustainably and without the usual accounting risks that plagued the ecommerce companies.

With (1) a superior ROE of 23.6% due to its wide-moat business model in 24-hour delivery system, (2) negative cash conversion cycle (-29 days) in its unique warehouse system with minimal inventory risk, (3) a sustained 25-30% recurring earnings and cashflow growth per annum in the next 5 years, especially a long run-way in disrupting traditional retailers, and (4) potential exponential growth in its option value in the third-party electronic payment business, the company can scale up multiple times. Short-term downside risk is protected by its healthy$128m net-cash balance sheet (15% of MV) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. Its terminal value and long-term downside risk will be protected by giants Alibaba, Rakuten, eBay, Amazon who wish to swallow it up to possess its valuable trust and brand equity support it enjoys and its wide-moat business model in 24-hour delivery system. The company is one of the few Asian ecommerce companies with good governance and low accounting risks with its net-value revenue recognition method and it deserves a valuation premium. Upcoming deregulation in third-party electronic payment with the passing of the law in Sep 2014 will result in various government restrictions to be removed, paving the way for the company to introduce stored-value payments, O2O payment, P2P payment (money transfer without transactions), multiple currencies’ payments, big data analysis, payment services for customers outside the group to boost transaction volume and scale up its existing proprietary PayPal/AliPay business. Led by the inspiring and highly-determined founder and Chairman who established and listed the company in 1998 and 2003 respectively, the company has overcome the multiple obstacles to ecommerce transactions in its home market. The founder described the obstacles to ecommerce transactions as ‘friction’, and that he “resolve to take on the Life’s Task to reduce this ‘friction’”.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

| Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

| Thank you so much for reading as always.

Warm regards, KB Kee Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

| P.S.1 Here is a little more about my background:KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of theinvestment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

| CONNECT WITH US |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT USThe Moat Report Asia A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013Other offices: London, Singapore, Zurich |