Tide Reverses in Latin America; Brazil’s Prospects Fall While Mexico’s Rise as Fed Prepares to Ease Bond Buying

September 9, 2013 Leave a comment

September 8, 2013, 7:35 p.m. ET

Tide Reverses in Latin America

Brazil’s Prospects Fall While Mexico’s Rise as Fed Prepares to Ease Bond Buying

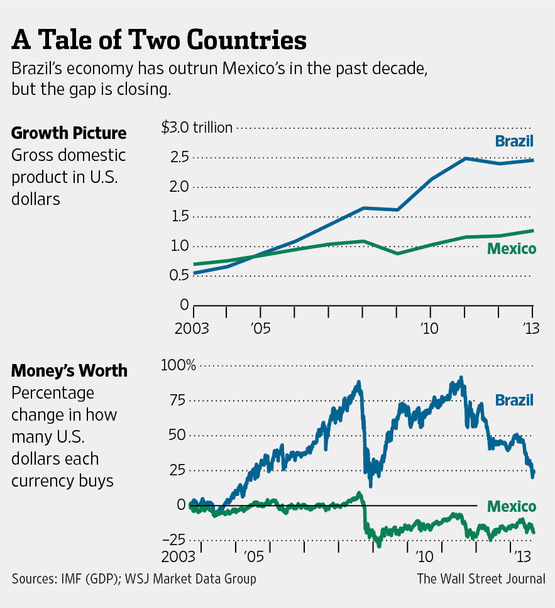

The divergent fortunes of global emerging markets can be told through Latin America’s two biggest economies: Mexico and Brazil. Think of it as a tortoise-and-hare story. For the past decade, Brazil has boomed by selling raw materials to China. Its expanding middle class gorged on a tide of cheap credit unleashed by central banks in advanced economies as they tried to energize their recoveries.Brazil’s economy averaged 3.6% annual growth over the past decade, peaking at a 7.5% pace in 2010. Its currency surged in value.

All the usual signs of excess were in evidence: Brazilian shoppers cramming stores in New York and Miami; news stories reporting $30 cheese pizzas and $35 martinis in São Paulo.

By comparison, Mexico has seen lackluster growth, partly because it has been tied to a struggling U.S. economy. It has also suffered from deep problems of its own: laws that banned foreign investment in energy, a dysfunctional tax code, a tattered education system and hidebound economy dominated by a handful of near-monopolies. And it suffered a surge in drug violence, deterring tourists and investors.

Mexico’s economic growth averaged 2.6% per year over the past decade, while its currency has slipped slightly in value.

Now the shoe’s on the other foot. Brazil is being punished by investors as the U.S. Federal Reserve signals a coming wind-down of its ultra-loose money policies and as China’s hunger fades for its raw materials. Brazil’s currency and stocks have both sunk by more than 10% this year.

“Brazil has done very well over the past 10 years on the back of a commodities boom that’s transferred massive wealth from China, said David Rees, emerging-markets economist at Capital Economics. “That’s now coming to an end.”

Brazil largely squandered the bonanza, investing little in roads and other areas that could foster its development. Its government has pursued a state-led economic model, rendering many of its businesses uncompetitive abroad. And businesses and households loaded up on debt, further constraining future growth. It has developed a significant gap that must be financed by foreign borrowing.

Meanwhile, Mexico used its lean years to overhaul its economy, revamping the country’s labor laws, education system and its telecommunications system, financial and energy sectors—including a plan to open up its oil and gas sector to private investment. If completed, economists expect the changes to lift the country’s growth potential at a time when Mexico’s biggest trading partner, the U.S., kicks into higher gear.

At the same time, Mexico has maintained a relatively small trade deficit that is easily financed by long-term foreign investment in companies and factories there. It isn’t as dependent on fickle flows of short-term foreign cash and, as a result, has been less affected by the turmoil roiling Brazil and other emerging markets in recent weeks.

Mexico could still disappoint. Its economy shrank slightly in the second quarter, while Brazil has had a stronger few months than many analysts expected. Mexico’s central bank on Friday cut interest rates by a quarter point to support the economy. But many economists expect Mexico to pick up speed in the months and years to come.

The story of Latin America’s two largest economies helps illustrate why the fortunes of emerging markets are now diverging. For the past five years, developing economies such as Brazil, Russia, India, China and South Africa—the so-called BRICS—have been the engines of global growth as developed economies coped with the after-effects of the financial crisis.

To support their sluggish economies, central banks in the U.S., U.K., and Japan bought bonds to push their interest rates down to historic lows, sending a wave of cash into emerging markets in search of higher yields. With the Fed signaling that it will start to wind down its $85 billion-a-month bond-buying program this year, that tide is reversing and money is draining from developing nations.

The list of losers is already apparent. They’re countries with large financing needs—because they have large trade gaps or budget deficits or because they’ve borrowed heavily abroad. India, Turkey, Indonesia, South Africa and Brazil have all suffered big market selloffs in recent weeks—a chief topic of discussion at last week’s meeting of the Group of 20 nations in St. Petersburg, Russia.

Others, including Mexico, the Philippines, Poland and South Korea, have suffered smaller outflows of cash. In general, they tend to be countries with small trade gaps to finance and relatively little debt—both public and private. They’re also countries that export manufactured goods to a slowly recovering U.S. and Europe instead of raw materials to China.

Unlike the BRICS, they tended to grow more slowly over recent years and didn’t build up large trade imbalances or big debts. They undertook difficult economic overhauls during the slow years. They didn’t become dependent on China, and aren’t as exposed to its slowdown. And they stand to benefit from trade links to the West.

Call it the revenge of the tortoises.