Could Bed Bath & Beyond Be Buffett Bait? With strong profits and steady growth, Bed Bath & Beyond was a great retailing story in the 20th century. The moves it’s making could make it an even better story in the 21st.

March 10, 2013 Leave a comment

SATURDAY, MARCH 9, 2013

Could Bed Bath & Beyond Be Buffett Bait?

By ANDREW BARY | MORE ARTICLES BY AUTHOR

With strong profits and steady growth, Bed Bath & Beyond was a great retailing story in the 20th century. The moves it’s making could make it an even better story in the 21st.

One of the country’s most successful retailers is on the bargain counter.

Bed Bath & Beyond has generated 16% annual growth in earnings per share over the past 10 years. But its shares, at $59, trade for less than 12 times projected profit for its fiscal year that ends in February 2014. The stock (ticker: BBBY) trades at a discount to other top retailers’, including Costco Wholesale (COST) and Target (TGT), neither of which has such a good profit history.

The shares could trade into the $70s in the next year, simply based on projected earnings gains and a higher price/earnings multiple. The insular company could attract interest from private-equity investors or even Berkshire Hathaway (BRK.A) if Bed Bath & Beyond’s co-founders, Leonard Feinstein, 75, and Warren Eisenberg, 82, decide to sell. However, there is no indication that the company is looking to sell.

A BUYER MIGHT PAY $85 a share—roughly 10 times this fiscal year’s projected earnings before interest, taxes, depreciation, and amortization (Ebitda)—consistent with prices paid for other quality companies, versus Bed Bath & Beyond’s current modest valuation of 6.5 times. The company’s $13 billion market value makes it large, but digestible. “This is a high-quality, cash-rich company that could see improving margins this year, particularly in the back half,” says Laura Champine, an analyst at Canaccord Genuity who carries a $74 price target on the stock. Bed Bath & Beyond has commanded an average of 15 times forward earnings in the past seven years.

The company, based in Union, N.J., operates 1,469 stores, including 1,004 Bed Bath & Beyonds, in all 50 states. The other 400-plus stores include World Market, which sells home furnishings, wine, and gourmet food; the fast-growing buybuy Baby chain, Christmas Tree Shops, and Harmon discount shops.

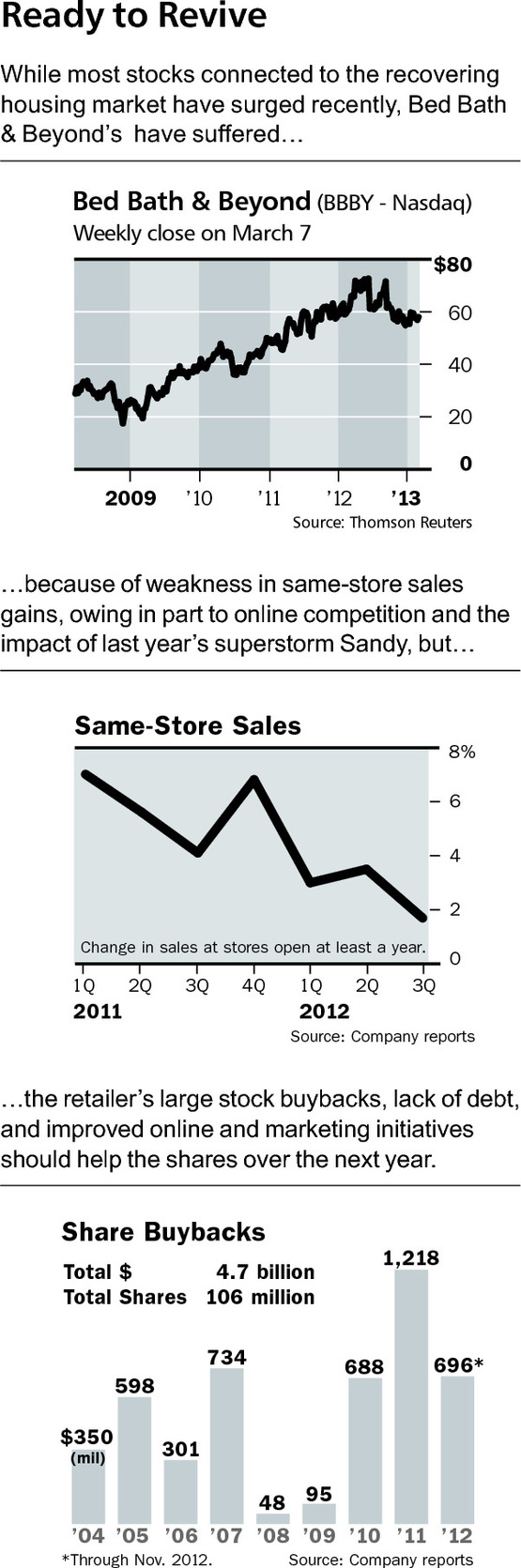

Bed Bath & Beyond has fallen from favor on Wall Street because of slowing comparable-store sales gains, mild profit disappointments, and concern that its weak Website makes it vulnerable toAmazon.com (AMZN) and other top Internet retailers. The company’s shares have slid 6% in the past year, even as virtually all stocks connected to the improving housing sector have surged.

Nonetheless, the company’s earnings in its just-concluded fiscal year ended in February likely rose a healthy 12%, to $4.56 a share, and are projected to increase 10% in its current fiscal year to $5.03.

Bed Bath & Beyond could be the most financially conservative big retailer in the U.S. It has no debt and it hasn’t carried a smidgen of debt for nearly all of the two decades since it went public in 1992. And it has $859 million—nearly $4 a share—in cash and marketable securities. The company has grown enormously, with revenue hitting an estimated $10.9 billion last year, versus $216 million in 1992 and it has accomplished this entirely with internally generated funds. Longtime investors have huge gains; the split-adjusted initial-offering price was $1 a share.

Management, led by CEO Steve Temares, plus co-Chairmen Feinstein and Eisenberg, run Bed Bath as if it were a private company. There are no investor days, limited financial disclosure, and no opportunity for questions on earnings conference calls. Want to know the sales breakdown among its chains? Bed Bath doesn’t disclose it. The retailer didn’t return Barron’s calls seeking comment.

The company’s retailing smarts and financial strength might appeal to Warren Buffett as he continues to seek large acquisitions for Berkshire Hathaway. We suspect that if Eisenberg and Feinstein were to sell, they’d prefer a long-term buyer like Berkshire that would keep management in place, rather than private equity, which would lever up the company with a lot of debt and possibly slash costs to boost returns for a quick score. It should be said that neither co-founder owns a big stake anymore. Eisenberg has 1.5%; Feinstein, 1%.

Since 2004, Bed Bath & Beyond has bought back $4.7 billion worth of stock, dropping its share count by more than 100 million, to 226 million. Indeed, most of its annual free cash flow of about $1 billion goes for buybacks. The company expects to spend about $800 million in each of the next three years to retire perhaps another 15% of its stock. Bed Bath, however, is one of the few big retailers that pays no dividend, even though it could comfortably support a $1.50 yearly payout, producing a 2.5% yield, and still have a nice-size buyback program. Says Champine: “A dividend would attract a whole set of investors who can’t look at the stock now.”

THE BULK OF SALES and profits likely come from Bed Bath stores, which carry a wide selection of home furnishings, including sheets and towels; small kitchen appliances like coffee makers and toasters; crystal, drapes, and picture frames.

Bed Bath has had no direct competition since Linens ‘n Things was liquidated in 2008 after a bankruptcy. It controls an estimated 25% of the domestic home-furnishings market. Department stores offer limited competition because clothing generally generates higher profits per square foot of selling space than housewares.

Bed Bath’s strategy is unlike any other major retailer’s. It rarely advertises and usually avoids markdowns except on seasonal items, while providing excellent customer service. It targets customers with coupons offering a 20% discount, or $5 off, a single item (with a wide number of excluded products) to help drive traffic. As savvy shoppers know, Bed Bath & Beyond generally accepts expired coupons, and it’s known for a liberal returns policy–customers sometimes needn’t present a receipt. And they often present multiple coupons. The approach works because many customers come for a single item and leave with many, as they walk around the “racetrack” layout of the narrow-aisled stores.

The Bottom Line

Shares of Bed Bath & Beyond could rise 25% from a recent $59 over the next year, on good profits. The company could fetch $85 a share if the founders decide to sell.

Despite the discounts, Bed Bath & Beyond consistently boasts a high net profit margin—10% in 2011 and just under that last year. Most retailers aren’t even close.

Bed Bath’s store managers have considerable autonomy in merchandise selection. The company has no central distribution facilities; suppliers typically deliver directly to stores. Feinstein has called this “our uniquely decentralized culture.”

Bed Bath remains very much a 20th-century retailer, and that worries Wall Street. Sales growth in stores open at least a year has slowed, falling to 1.7% in the quarter ended in November from 3.5% in the second quarter and 5.9% for all of 2011. The company says superstorm Sandy cut sales about 1% in that quarter. Management sees a recovery in same-store sales growth to 2% to 4% in the just-ended February quarter—results are expected to be reported around April 10–and in the current year. One reason for weaker sales could be flagging interest in Keurig coffee makers made by Green Mountain Coffee Roasters (GMCR). Bed Bath is a major seller of them.

The retailer hopes its purchase last year of Cost Plus, which operates World Market stores, boosts overall sales. It’s putting World Market products—including food and wine—into some Bed Bath stores. “The company is looking to drive traffic at Bed Bath & Beyond with consumables. How often do you need to buy drapes?” Champine asks.

The company’s lack of a strong online presence concerns investors. Its Website isn’t believed to have had a major makeover in a decade. Bed Bath probably gets less than 5% of its sales online, versus Williams-Sonoma‘s (WSM) almost 40%. However, Bed Bath plans to roll out an improved Website this year and is building a large e-commerce fulfillment center in Georgia. Analysts have compared prices of various products on Amazon.com and Bed Bath and given a slight edge to Amazon. Yet the gap doesn’t reflect the impact of Bed Bath’s coupons. In addition, customers shopping for towels, sheets, drapes and other home furnishings often want to touch them, something that benefits Bed Bath & Beyond.

Champine says the retailer only recently focused on developing a data analytics group: “It looked like they were papering the world with coupons and that’s because they probably were.” The new group could better target its marketing.

Expenses for the improved online and marketing efforts are hurting earnings, but Champine sees higher margins later this year.

Wall Street isn’t giving the old-school retailer credit for finally moving into the 21st century. But the transformation should help it keep thriving. It’s also good to know that the founders probably could pick up the phone and sell the company quickly for a premium, rather than offering a 20%-off coupon.

Touchy-Feely

Bed Bath & Beyond stores, which feature narrow aisles heaped with goods, are meccas for shoppers. Shares trade at a lower price/earnings ratio than those of other top retailers despite a record of strong profit growth.

| Bed Bath |

Williams- |

Pier | |||

| & Beyond | Costco | Target |

Sonoma |

One | |

| Ticker | BBBY1 |

COST2 |

TGT |

WSM |

PIR1 |

| Recent Price | $58.83 |

101.97 |

65.85 |

45.44 |

22.28 |

| 12-Month Change | -4.7% |

16.0 |

16.3 |

20.1 |

32.9 |

| 2012 EPS E | $4.56 |

3.97 |

4.78 |

2.54 |

1.19 |

| 2013 EPS E | $5.03 |

4.50 |

4.71 |

2.82 |

1.38 |

| 2013 P/E | 11.7 |

22.6 |

14.0 |

16.1 |

16.1 |

| Dividend Yield | None |

1.1 |

2.2 |

1.9 |

0.9 |

| Annual Sales (bil)3 | $10.9 |

99.0 |

73.0 |

4.0 |

1.7 |

| Market Value (bil) | $13.5 |

44.1 |

42.9 |

4.5 |

2.4 |

| 1-BBBY and PIR fiscal year ends February. 2-COST fiscal year ends August. 3-2012 sales. E=Estimate. | |||||

|

Source: Thomson Reuters |

|||||