Chinese College Graduates Play It Safe and Lose Out; Chinese college graduates say they want to work for the government or big state-owned firms, which are seen as recession-proof, rather than the private companies that have powered China’s economic climb

March 26, 2013 Leave a comment

March 25, 2013, 10:32 p.m. ET

Chinese College Graduates Play It Safe and Lose Out

By BOB DAVIS

BEIJING—Xie Chaobo figures he has the credentials to land a job at one of China’s big state-owned firms. He is a graduate student at Tsinghua University, one of China’s best. His field of study is environmental engineering, one of China’s priorities. And he is experimenting with new techniques for identifying water pollutants, which should make him a valuable catch. But he has applied to 30 companies so far and scored just four interviews, none of which has led to a job. Although Mr. Xie’s parents are entrepreneurs who have built companies that make glasses, shoes and now water pumps, he has no interest in working at a private startup. Chinese students “have been told since we were children to focus on stability instead of risk,” the 24-year-old engineering student says.

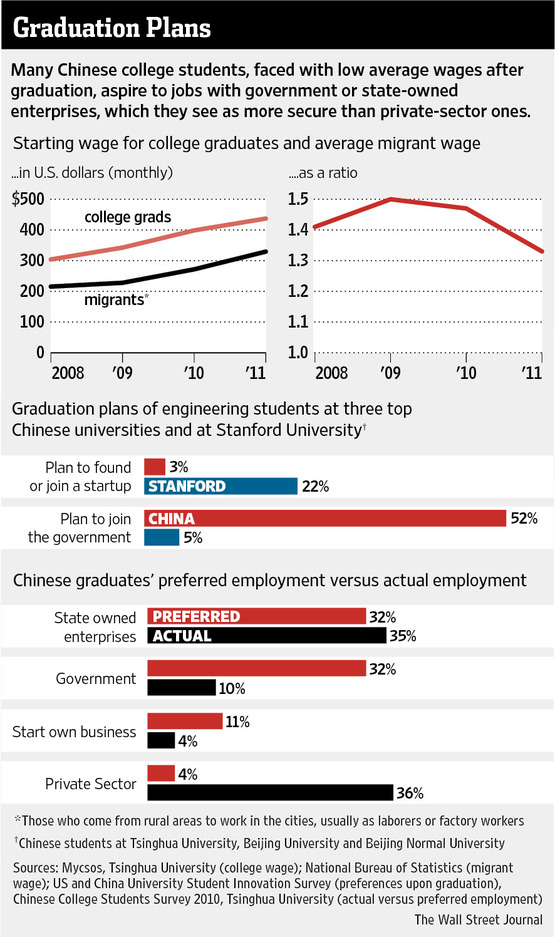

Over the past decade, the number of new graduates from Chinese universities has increased sixfold to more than six million a year, creating an epic glut that is depressing wages, leaving many recent college graduates without jobs and making students fearful about their future. Two-thirds of Chinese graduates say they want to work either in the government or big state-owned firms, which are seen as recession-proof, rather than at the private companies that have powered China’s remarkable economic climb, surveys indicate. Few college students today, according to the surveys, are ready to leave the safe shores of government work and “jump into the sea,” as the Chinese expression goes, to join startups or go into business for themselves, although many of their parents did just that in the 1990s.

Chinese economists worry that waning entrepreneurial zeal could hobble China’s ability to remake its economy and reach the ranks of wealthy nations. “The current education system does not produce people who are innovative,” says Li Hongbin, a Tsinghua University economist who specializes in education and conducted some of the surveys. “That makes it harder for the country to reach its long-term goal of building an innovative society.”

Among Chinese age 21 to 25, university graduates have an unemployment rate of 16.4%, four times the rate for those who quit school after elementary school, according to a 2011 survey of 8,400 households by Texas A&M economist Gan Li. The new college grads who do get jobs often get crummy ones. Nearly half of college graduates in 2011 started at wages below those paid to migrants who come from China’s farms to fill its factories and construction sites, according to surveys by Tsinghua’s Mr. Li.

Working hard in college doesn’t appear to make much difference. On average, Mr. Li found, graduates with top grades make about 10% less on their first jobs than those with mediocre ones—an outcome that many students ascribe to their mediocre classmates having better political connections.

China’s population-control policy may have further undermined risk-taking among college students. Some parents who are limited to one child say their families have little margin for error, so they discourage their children from taking a flier working for a private firm. Government work also is a plus when seeking a marriage match. “If you’re a civil servant, you’ll be so popular on the blind-date market,” Zheng Jiangqiu lectured her daughter, Dong Linshan, an international-business graduate, over lunch recently in Wenzhou, a south China city famed for entrepreneurship.

Five researchers compared engineering students at Stanford University with those at three top Chinese universities—Tsinghua, Peking University and Beijing Normal University—and found that a majority of the American and Chinese students dreamed of starting their own firm. But when it came time to take the plunge, only 3% of the Chinese students said they would join a startup, compared with 22% of Stanford students. Ten times as many Chinese students as Stanford ones said they would seek government jobs.

Matthew Boswell of Stanford, who led the research project, said that Chinese students didn’t have as much venture-capital and research funding available to them as their Stanford contemporaries—resources that help would-be entrepreneurs “offset the risk of trying to branch out and do something new.”

Chinese students also understand the pre-eminent role of the state in business, says a 34-year-old Chinese economist for a Western financial firm. “When I was graduating, I wanted to be like Steve Jobs,” the Apple founder, the economist recalls, so he sought out jobs in Western firms to learn modern business techniques. But in China, he says, even famous entrepreneurs “have to bow to the government,” which discourages initiative.

China’s dilemma has been seen in other developing countries that try to advance their economies through college-building booms, then find they can’t produce enough jobs to employ the graduates. In Latin America, Korea, India and elsewhere, that has led to complaints of a “brain drain,” as graduates head to the U.S. or Europe in search of opportunity.

China is unusual in that its college-graduate problems have arisen despite the economy’s average annual growth rate of 10% for three decades. Unemployment among college grads of all ages is about 3%, well below the rate for those who drop out after elementary school. But for recent grads, there aren’t enough available jobs that require a college education.

China’s college-building boom began around 2000 and gained speed by turning vocational schools into four-year colleges. As incomes of Chinese families grew, more could afford to pay college tuition, which puts a dent even in incomes considered “middle class” by Chinese standards. Decisions about curriculum and fields of study were made largely in Beijing at the Ministry of Education or by provincial officials, with little input from local employers. The result was a mismatch between graduates turned out by many schools and the skills sought by employers. According to Tsinghua’s Mr. Li, employers don’t pay much because they don’t believe the graduates are worth much.

Students look to the government as a lifeline. Last year a record 1.1 million students took the national civil-service exam, 13% more than the prior year, according to Xinhua, China’s state-owned news agency. In the northern Chinese city of Harbin, 3,000 college graduates last fall applied for about 1,000 jobs to be street cleaners, drivers and other sanitation-department workers, Chinese state media has reported. In Taiyuan, in the heart of China’s northern coal belt, Guo Yihan, a senior at Shanxi University’s business school, says he would rather join the army than take an accounting job at the usual private-sector starting salary of about $250 a month.

In a 2010 survey of students at 50 colleges by Tsinghua’s Mr. Li, two-thirds said they wanted jobs in the government or state-owned firms, while only 11% said they wanted to start their own business. With not enough government jobs to go around, 36% of students wound up working for private firms and another 4% became entrepreneurs. About 10% wind up working for foreign firms.

Beijing is attempting to rekindle entrepreneurship among the young, including by wooing back Chinese entrepreneurs and younger professionals who studied overseas and stayed there. That includes offering subsidized apartments, research money and bonuses of as much as $160,000. Since 2008, just 3,300 professionals have taken the offers, says Wang Huiyao, director of a Beijing think tank, the Center for China and Globalization.

Some of China’s elite universities, including Tsinghua and Peking University in Beijing and Fudan University in Shanghai, have set up “incubator programs” to help entrepreneurs develop commercial applications for research conducted at the universities.

But talent continues to drain from China. Between 1996 and 2011, 2.2 million Chinese students went overseas to study and only one-third have returned, according to Chinese government statistics.

Dai Yusen, 27, came back after studying at Stanford’s School of Engineering in 2009. He founded Jumei.com, an online cosmetics business that now employs 1,700 and has made Mr. Dai a poster boy for Chinese entrepreneurship.

He says he learned important lessons at Stanford on team building and got a jolt of self-confidence by meeting with famous Silicon Valley entrepreneurs. He says the success of young Chinese entrepreneurs may eventually change the safety-first attitudes of college graduates.

That could take time. In 2009, Jing Ming, a bioengineering graduate at Jiangsu Normal University in southern China, banded together with a group of friends to start a yogurt-making company. They moved to the city of Nantong to set up operations. But after learning of the bureaucratic hassles and petty corruption they would face—including picking up the cellphone tabs for some officials, he says—the group abandoned their dream. Mr. Jing went to work at a state-owned environmental-monitoring firm.

In the 1990s, small businesses turned the southeastern China city of Wenzhou from a backwater into a bustling metropolis of three million. Its downtown boasts a replica of Paris’s Arc de Triomphe and its outskirts are dense with factories. Locals say they had little choice but to go into business. In Wenzhou and elsewhere, the government was closing tens of thousands of money-losing state-owned firms and throwing millions out of work.

But instead of being hailed as saviors, entrepreneurs were viewed suspiciously by many residents, who have memories of bankrupt factory bosses shutting down and scooting out of town without paying workers. During the past decade, meanwhile, many of China’s surviving state-owned firms thrived, and now dominate banking, transportation, energy and other profitable sectors, making them sought-after employers.

In 2000, wages paid by foreign-owned firms were 40% higher, on average, than by state-owned companies, government statistics indicate. By 2011, the gap had narrowed to just 11%. In addition, state-owned enterprises provide some benefits that foreign-owned firms can’t, such as residence permits that enable new workers to bring their families with them and get their children into good schools.

“SOEs have a lot to offer,” says Jim Leininger, a Beijing consultant at human-resources firm Towers Watson TW +1.15% & Co. “They’re big. They’re famous. They engender a tremendous amount of national pride. And you’ll be able to develop good connections there.”

The Chinese government itself, meanwhile, is seen as rock-solid employer, largely immune to layoffs. Although average government wages lag behind those of state-owned firms, government work is regarded as prestigious. In addition, college graduates realize the decisions of senior bureaucrats can make or break companies—and can provide opportunities for payoffs for the less scrupulous.

“You have to beg government officials sometimes,” says Mr. Xie, the Tsinghua grad student, who hails from Wenzhou. He said his parents wanted him to get a government job, in part because they felt that might position him to help the family businesses. When it comes to dealing with government bureaucrats, he says, “there’s a saying in Chinese, ‘You have to pretend that you’re their grandson,’ ” playing up to those in power. Mr. Xie says he doesn’t want to work for a private firm where he might be put in the position of supplicant.

Ms. Dong, 25, the international-business graduate, attended the Ningbo, China, branch of Britain’s Nottingham University, where courses are taught in English. She says she wanted to learn the “critical thinking” that her uncle, a Wenzhou shoe exporter, and other employers say is lacking in Chinese graduates. She says she was taught to see the world more broadly than her Wenzhou contemporaries, but her degree led to just a handful of low-paying job offers, including one at a language school where she would assist foreigners who teach English.

“If you work for private-sector [Chinese] firms, your family will lose face,” she says. “Those aren’t famous firms.”

Instead, she pursued a master’s degree in international business at Nottingham, graduating in November and setting her sights on a job in a state-owned bank. She sent out 50 resumes and landed a half-dozen interviews with banks, but has yet to find a job.

She recently told her mother, again, that she won’t apply for a civil-service job because she considers the work boring and sometimes corrupt, but will keep searching for a secure job in a state-owned firm. She sees jobs at entrepreneurial firms as too risky in a global economy riddled with uncertainties.

Only as a last alternative, she says, will she turn to her uncle to ask for a job in his shoe business. “It’s not cool to start a business,” she says. “If you try something and it fails, people will laugh at you.”