Australia: Rising debt weighs heavily on any future boom

May 8, 2013 Leave a comment

Rising debt weighs heavily on any future boom

May 8, 2013

Clancy Yeates

When confidence is building in the property market, as it has been lately, it can be easy to get swept up in the hype. Many of us know people who have made small fortunes on property. After all, house prices rose 6 per cent each year in the boom years between 1995 and 2005. Might this happen again?

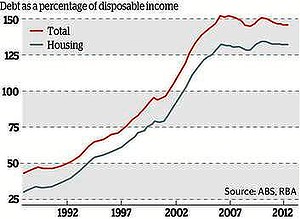

Household indebtedness

There are entire industries – from real estate agents to mortgage brokers – that like to believe so. Some of the less scrupulous operators even like to mention this boom era in their sales pitch, implying it may soon return. While there are signs the housing market could be strengthening at the moment – prices are up 2.7 per cent nationally in the past year – a long-term view suggests we won’t see a return to the boom days of old. Why not? Perhaps the biggest reason is household debt. There were several reasons prices rose so quickly in the past, but the big one was that people bid them up by borrowing more. As this week’s graph shows, we went from borrowing about 50 per cent of disposable income in the early 1990s to 150 per cent – where it has settled. This increase occurred because we were taking out bigger home loans. Such a staggering rise was only possible because debt became a lot cheaper, thanks to a one-off drop in interest rates, and competition in banking.

But both these factors are highly unlikely to be repeated, and here’s why.

First let’s look at interest rates.

First let’s look at interest rates.

In the early 1990s, the cash rate got up to 17.5 per cent, which severely restricted how much people could borrow.

Rates were so much higher because inflation had been running at around 10 per cent throughout much of the 1980s.

Over the 1990s, Australia became a low-inflation economy, and rates fell accordingly. These days, rates tend to fluctuate between about 7 per cent in boom times and 3 per cent when things are weak, as is the case now. The second reason borrowing became a lot easier was an opening up of the banking sector to competition.

The Commonwealth Bank was privatised, foreign lenders entered the market, and a bunch of non-banks started lending.

The result was fiercer competition, a keenness among banks to lend, and cheaper credit.

The thing to remember is, these shifts can only occur once.

Inflation can’t be contained again, and we can’t deregulate our financial system a second time.

Other factors may push up house prices, like strong demand and lacklustre supply of new dwellings.

But without house prices being turbocharged by higher leverage as they were in the last boom, the housing market in the future is likely to feature more modest prices than in the past.