Beware of ‘Bargain’ Stocks; Why a Low Share Price Alone Doesn’t Make for a Good Value

May 25, 2013 Leave a comment

May 24, 2013, 6:14 p.m. ET

Beware of ‘Bargain’ Stocks

Why a Low Share Price Alone Doesn’t Make for a Good Value

By LIAM PLEVEN

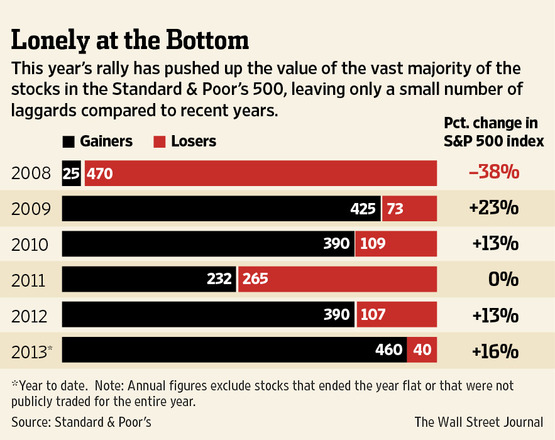

Bargain hunters shopping for underpriced U.S. stocks in the ongoing rally could end up with less than they bargained for. The pool of large-company stocks with prices that are lower than they were at the end of 2012 is getting perilously small. All but 40 of the stocks in the Standard & Poor’s 500-stock index are up so far this year. Just 35 others are up by less than 5%. The S&P 500 has jumped 16%, not including dividends, so far this year. U.S. stocks held firm Thursday despite a 7.3% drop in Japan, though the S&P lost 1.1% for the week. That so few stocks are in the red so far this year suggests the stragglers are unlikely to catch up to the overall market soon, experts say. For investors, that makes the discount bin a potentially risky place to buy. “I don’t believe the laggards are going to arise from the dead any time soon,” says Kim Forrest, a senior equity analyst at Fort Pitt Capital Group in Pittsburgh, which manages about $1.3 billion. Value investors like Ms. Forrest hunt for stocks of companies that are underappreciated and undervalued. It is an approach championed by Warren Buffettand many other bargain hunters. But a low share price isn’t the same thing as a good value, particularly if the weakness reflects some fundamental problem facing a company or its industry.Investors who conflate the two may be succumbing to a common desire to buy cheaper stocks in order to avoid overpaying, says Meir Statman, a finance professor at Santa Clara University in California.

It is similar to the impulse that compels investors to cling to stocks they already own that have declined in price, he says.

Research suggests that is a bad strategy, Mr. Statman says, because stocks that have gone down over the past six months to a year are more likely to keep going down for roughly the same amount of time.

“Usually, losers continue to lose,” he adds.

Stocks in every major part of the economy are rising. This year, all 10 sectors in the S&P 500 are up between 7.2% and 23%.

Those sectors consist of many smaller categories, but even there losers are scarce. For instance, the consumer-staples sector is up 19% this year, while food retail and household products, which are parts of the sector, are up 23% and 20%, respectively.

Across the S&P 500, only seven of 126 subsectors are in negative territory in 2013, according to FactSet, and the reasons are often obvious. The gold category is down 31%. That isn’t surprising, since the price of the bullion that miners produce is down 17% so far this year and 27% from its 2011 peak.

Among individual stocks that are duds, there also are frequently clear explanations.J.C. Penney JCP -2.11% recently underwent a management shake-up after a turnaround plan faltered. Shares of the retailer are down 3.7% this year. Alcoa,AA -0.70% down 2.3% in 2013, faces falling prices for the aluminum it produces.

Industries and individual stocks that have been left behind could turn around, of course. But that could take time.

“Don’t expect these things to shoot up in 2013,” says Fort Pitt Capital’s Ms. Forrest. She thinks it could take three to five years for some laggards to rebound.

That could pay off for investors who have lots of patience. But many investors are more like “hyperactive kindergartners playing musical chairs,” says Sam Stovall, chief equity strategist at S&P Capital IQ. “They don’t have the patience.”

Meanwhile, some stocks that have gotten more expensive this year might rise further, says Gina Moore, a portfolio manager at AJO in Philadelphia, which manages $22 billion, mostly for institutional clients. If that happens, investors who sold gainers in order to load up on laggards could regret the move.

For instance, Ms. Moore says the stocks of some companies that try to tap into consumers’ discretionary purchases, such as DirecTV, DTV -0.28% GameStopGME -10.83% and Macy’s, M +0.47% remain undervalued, despite having risen by 26% to 28% this year.

The rally, of course, could also end suddenly. Many investors are concerned that the economy and earnings remain weak.

“A lot of investors have been waiting for a strong correction,” Mr. Stovall says. If that happens, the stocks that have climbed the most this year could skid, he says—but the same stocks are the most likely to bounce back strongly if investors see the slide as a buying opportunity.

Rather than buying up laggards, Mr. Stovall says, the appropriate response to this year’s rally may be to “let your winners run and cut your losers short.”