China’s consumers look for alternatives for their savings and their smartphones, at the expense of state firms

May 25, 2013 Leave a comment

Updated May 24, 2013, 7:03 p.m. ET

China’s Consumers Fight Back, Explore Options

By TOM ORLIK And PAUL MOZUR

BEIJING—On a freezing winter evening, Philip Chow jumped a long taxi line at Beijing’s airport by using an app on his smartphone that signaled to drivers he would pay a tip for a quick pickup. The app, called Didi Dache—Honk Honk, Catch a Cab—is among the latest examples of a new force sweeping China: consumer power. Chinese households are signaling impatience with government controls that cut against their interests. They have started to win important victories, not just finding ways around artificially low fare levels that reduce the number of taxis on Beijing’s streets, but also alternatives to high cellphone costs by state-run telecom firms and low interest on their savings in state-run banks.The trend, which is often aided by technology, is breaking ground in a quest where China’s leaders have fallen short, to redistribute wealth and get more of the benefits of China’s development into consumers’ hands, a crucial goal in steering growth onto a more sustainable path.

Didi Dache is a small but important illustration of this trend. Government-set fares for taxis haven’t kept pace with inflation, reducing incentives for drivers to start their engines. That leaves Beijing, like other large cities, with too few cabs to go around—a city of 20 million trying to thumb a ride from just 66,000 cabs.

“The rule is, if it’s rush hour, forget about cabs,” said Mr. Chow, a philanthropy consultant who lives in Beijing. The new app brings market forces into play by letting customers pay a premium for a quick pickup.

For the past decade, a combination of low wages, low bank interest rates on deposits and limited opportunities for entrepreneurs has starved China’s households of their share of rising prosperity.

The main task for China’s new generation of leaders: get funds flowing back into households’ pockets. Economists say that requires changes to everything from government control of the commanding heights of the economy, to a more market-based financial system. The government has made some progress, with increases to the minimum wage a key policy to raise household income.

But a big stumbling block to doing more is China’s state-owned enterprises, beneficiaries of existing arrangements that rack up more than 1.4 trillion yuan ($230 billion) in profits a year. “SOEs have many means at their disposal to block reforms,” said Minxin Pei, an expert on China’s politics at Claremont McKenna College.

However, even with the limited changes in policy, consumer power means small but significant changes are under way.

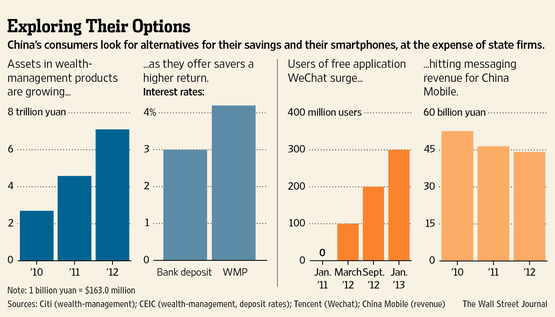

In telecoms, customers have long been hostage to expensive charges for texting from the three state-owned firms that dominate the market. Now WeChat, a free online messaging application, offers an alternative—letting smartphone users exchange text and voice messages free of charge over the Internet. WeChat has already garnered 300 million users since it was introduced 2½ years ago by by Internet giant Tencent Holdings Ltd. 0700.HK +2.19% —one of China’s largest private-sector companies.

Liu Yang, a 22-year-old cosmetics saleswoman in Beijing says she uses WeChat to keep in touch with friends. “In the past, I’d have to make calls or send short messages to friends that cost me about 100 yuan each month. Now my phone bill is less than 50 yuan,” she said.

China Mobile, the largest phone operator, reported profit growth of just 0.3% year on year for the first quarter, blaming “substitution of traditional communication business by new technologies” for slow growth. In the period, Tencent’s net rose 37%.

In banking, China’s households have long suffered from low returns on their deposits. Over the past decade, with interest rates on average below the level of inflation, households were propping up fat profits for the banks and providing cheap borrowing rates for state-owned firms.

Wealth-management products—short-term investments that offer some of the security of a deposit but higher returns—are starting to change that picture.

Three years ago, Stella Kuai, an administrator in a financial-services firm in Beijing, had all of her savings in bank deposits. Now she has tens of thousands of yuan in wealth-management products. “I usually buy whatever products have higher returns,” she said.

Assets in wealth-management products have grown from close to zero a few years ago, to about 7.1 trillion yuan ($1.2 trillion) at the end of 2012, equivalent to 8% of deposits in the banking system, according to the China Banking Regulatory Commission.

Wealth-management products offer households higher returns—currently averaging 4.2% a year compared with 3% in a one-year bank deposit. They are also crimping bank profits. Simon Ho, China bank analyst at Citi, estimates that the margin on wealth-management products is about 0.8%, substantially lower than margins of around 2.6% on their traditional lending business.

The rapid growth of the sector also brings risks, especially because many consumers are in the dark about the exact assets they are investing in. In March, China’s banking regulator moved to clamp down on the riskier investments and require higher standards of disclosure to investors.

China’s state-owned empire could yet strike back and China’s consumers are starting from a very low base. Private consumption accounted for just 35.7% of gross domestic product in 2012, compared with about 70% in the U.S. Investment accounts for 46.1% of the total, high in international and historical comparison. Changes like the rapid growth in online messaging and wealth management products have some funds moving back into household’s pockets but not all of them.

As for Didi Dache, in April, a local press report picked up by the official Xinhua news agency, said Beijing’s city government will soon “clean up” taxi apps like Didi Dache. One objective for China’s government appears to be keeping taxi fares affordable.

Didi Dache’s marketing director Zhuo Ran said in a statement the company is currently cooperating with the Beijing city dispatch center and denied rumors that it has been asked to stop service by the government.