Defensive Stocks Won’t Shield Investors

July 1, 2013 Leave a comment

June 30, 2013, 7:20 p.m. ET

Defensive Stocks Won’t Shield Investors

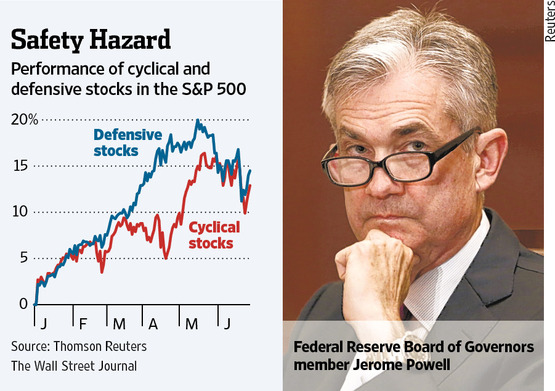

A rising stock market has always been a sign investors are taking on more risk. What made the recently stalled rally odd are the types of stocks where that risk-taking was concentrated. From the start of the year to its peak on May 21—the day before Federal Reserve Chairman Ben Bernanke intimated that the central bank might begin to scale back its bond buying program this fall—the S&P 500 rose 17%. But stocks that traditionally have been regarded as safe did better. A market-weighted index of defensive sectors of the S&P 500—which include consumer staples, health care, telecommunications services, utility and real-estate investment trust shares—rose 19.2% over the same period. An index of the remaining, more cyclically sensitive companies rose by just 16.4%.This goes against what usually happens in bull markets, where investors get enticed into cyclical stocks such as retailers, software firms and manufacturers. That is because these are companies that, so long as the economy is growing, are seen as having a much better chance of generating big earnings gains.

This time, partly on concerns about how well the economy would weather tighter fiscal policy, and partly because of a hunger for alternatives to low-yielding bonds, investors piled into defensive stocks.

In the process, those stocks got less safe.

Indeed, a Credit Suisse CSGN.VX -0.60% HOLT analysis shows that when Mr. Bernanke spoke, shares of defensive firms were trading at some of their stiffest premiums to their more cyclical counterparts, on the basis of future projected cash flows, in the past 20 years. Small wonder, then, that they fell more sharply. Through Thursday, defensives were down 3.9% since the market peak versus a 3% drop for the cyclicals.

Yet the defensives remain quite expensive relative to cyclicals. Looking at relative implied discount rates—which help put a price on expected future cash flows—the Credit Suisse analysis implies investors are paying a 1.57 percentage point premium for defensive stocks relative to cyclicals, compared with a historical average of 0.36 percentage points. It is hard to see that situation continuing if, as seems likely, the economy gains ground in the latter half of the year.

Fed Governor Jerome Powell said in a speech Thursday that, though growth has been middling so far this year, he has been surprised at how well the economy has performed in the face of tighter fiscal policy.

With those fiscal headwinds calming, growth ought to pick up—especially as businesses, recognizing that the economy didn’t actually get clocked by Washington’s shenanigans, gain in confidence.

As long as the economy really does improve, the Fed in all likelihood will begin moderating its bond purchases, with economists currently divided over whether that will happen in September or December. That might not provoke another sharp leg up in long-term rates. (The Fed certainly hopes it won’t). But it certainly suggests that the days of the 10-year Treasury yielding less than 2% are a thing of the past. Income-oriented investors’ need to find some alternative to bonds has, in turn, gotten a little less intense.

So the two things that have propped up defensive stocks—worries about economic growth and ultralow long-term interest rates—are getting kicked away, setting up a rotation into more cyclical stocks. It is time to play offense.