It was fun while it lasted. As Debt Boom Wanes, Firms in the U.S. have lost the luxury of being able to sell bonds at will

July 1, 2013 Leave a comment

June 30, 2013, 7:07 p.m. ET

As Debt Boom Wanes, Firms Readjust

MATT WIRZ

It was fun while it lasted.

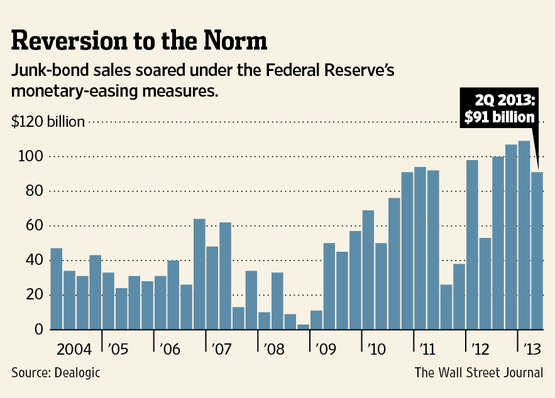

U.S. companies have borrowed unprecedented amounts in bond markets over the past four years, while the investors they sold the debt to have watched bond prices hit records courtesy of a wave of money from the Federal Reserve. All the while, borrowers and lenders have known this debt boom couldn’t last, and many responded with a paradoxical mix of angst and relief to the volatility triggered when Fed Chairman Ben Bernanke said in June that the central bank could start tapering its $85 billion-a-month bond-buying program by the end of 2013.“I don’t’ think this a terribly unhealthy thing,” said Craig Packer, head of leveraged finance in the Americas for Goldman Sachs Group Inc. “I think we were experiencing an unnatural level of issuance because we were in an unnatural environment, and this is more a return to the normal ebb and flow of the leveraged finance markets.”

As markets have become volatile, U.S. companies have lost the luxury of being able to sell bonds at will and will have to be more strategic in timing deals, investors and bankers said. The silver lining, some said, is that with recently issued debt trading as low as 90 cents on the dollar, some borrowers now have the option of retiring debt on the cheap.

Corporate issuance of both bonds and loans dropped sharply in June as the combination of rising Treasury rates and falling bond prices sent borrowing costs higher. This comes after investment-grade bond sales hit a record of $1.05 trillion in 2012 and averaged $105 billion a month in the first five months of this year before dropping to $44 billion in June for a total of $568 billion in the first half, according to data provider Dealogic.

The rolling 30-day yield on bonds rated double-B rose 1.38 percentage points, to 5.91%, in June, according to data from S&P Capital IQ LCD. The four-week rolling average of investment-grade bond sales fell to $11 billion at the end June, a 58% decline from the end of May, while sales of below-investment-grade, or “junk,” bonds slid 71%, to $3.1 billion, over the same period, according to Dealogic.

This, in markets lingo, is called a closing window of opportunity. For the past four years, the Fed has largely been able to keep the window open, fostering a bumper crop of bonds, but that isn’t the historical norm. Even in the go-go years of 2004 to 2006, new-issue activity varied quarter to quarter depending on market sentiment, and corporate treasurers had to monitor those swings to time deals.

With volatility back on the rise, timing is becoming more important once again. Investment-grade bond sales ground to a halt in early June, but a bout of investor optimism in the third week of the month briefly calmed markets and a number of companies launched large bond sales, including manufacturer Ingersoll-RandIR +0.05% PLC and energy company Chevron Corp. CVX -0.31%

Chevron sold $6 billion of debt on Sept. 17, its largest bond issue since at least 1995, before rates could rise further. “We’re very cognizant of some of the moves forecast by [the Fed], and we figured this was a good time to enter the market,” a spokesman said.

Meanwhile, companies may be more focused on buying back the bonds they recently sold than in issuing new debt. That is because many of the corporate bonds sold over the past year at record-low interest rates are now trading at deep discounts due to the rise in Treasury yields. As bond yields rise, their prices fall.

For the corporations with hefty cash balances, of which there are many, they can buy the bonds for less than investors first lent them and pocket the difference.

Health-care company Cardinal Health Inc., CAH -1.09% which has a single-A rating, sold in February a 30-year bond with a 4.6% interest rate. In early May, the debt traded at 103 cents on the dollar, but by last week it was trading at about 90 cents on the dollar, according to MarketAxess. A spokeswoman for Cardinal declined to comment.

Should economic activity slow, companies might engage in discounted buybacks to offset tepid profit growth, said Justin D’ercole, head of Barclays‘s BARC.LN 0.00%investment-grade-bond syndicate in the Americas. “If you need to release some earnings you might buy back bonds that you sold at what is now a wildly submarket rate.”