Burned Bond Buyers Re-Evaluate Africa

July 5, 2013 Leave a comment

July 4, 2013, 4:20 p.m. ET

Burned Bond Buyers Re-Evaluate Africa

SERENA RUFFONI And PATRICK MCGROARTY

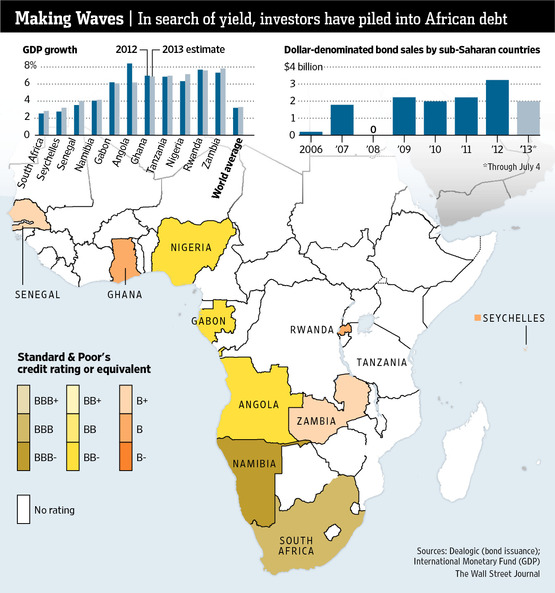

Just weeks ago, Africa was a hot destination for yield-hungry bond investors. It was a bet that burned many money managers. Prices of government bonds around the world have declined, pushing yields higher, as investors come to terms with the possibility the Federal Reserve could scale back its economic stimulus within months. A flurry of bonds issued by nations in sub-Saharan Africa since September have taken some of the biggest hits, an unpleasant wake-up call for investors who dove into these “frontier” markets in search of fat yields. The selloff has spurred investors to take a closer look at these countries’ finances and re-evaluate the risks that come with investing in Africa. As exuberance turns to trepidation, doubts have surfaced about whether countries with plans to tap international markets this year will proceed. Flagging investor interest has already raised borrowing costs for Nigeria, which sold $1 billion worth of bonds to global money managers Tuesday.Nigeria’s 10-year bonds were priced to yield 6.375%. In late April, yields on existing bonds were around 4%.

Zambia’s bonds, yielding 5.6% at the beginning of May, closed Thursday near 6.7%, according to Tradeweb. Tanzania sold $600 million of debt in February. Those bonds now yield around 6.2%, compared with 5.5% in May. Rwanda sold $400 million of 10-year bonds in late April at a yield of 6.875%. Those bonds are now trading north of 8%.

Many African economies, such as Rwanda’s, are dependent on international aid. Others, including Nigeria’s, rely on commodities to fill their coffers. Those complications come on top of military conflicts and unstable governments that persist in some parts of the continent.

And positions, once taken, are often very difficult to exit from, says Francesc Balcells, an emerging-markets portfolio manager at Pacific Investment Management Co., the world’s biggest bond-fund manager.

“You’re not in Brazil or Mexico, where you have countless data releases from official sources, and everyone can hop on and off highly liquid markets,” Mr. Balcells says. “In Africa, once you get in, you’re in for good.”

Many African bonds performed worse than other emerging-market debt during May and June, when jitters about the Fed’s next moves rippled through financial markets. The average yield of dollar-denominated emerging-market debt rose from 4.6% at the beginning of May to 5.8% as of July 2, according to the J.P. Morgan JPM -0.06%EMBI Global index.

It is difficult to determine whether many African countries are politically stable and fiscally responsible enough to invest in, says Valentina Chen, emerging-markets-debt fund manager at Aviva Investors, a London money manager that oversees about $416 billion in assets.

“We believe there are many risks investing in Africa and many unknown unknowns,” Ms. Chen says. “To put it simply, the yields in Africa are higher for a reason.”

To be sure, Africa is growing faster than most of the rest of the world. Gross domestic product is set to expand 5.6% across sub-Saharan Africa this year, according to the International Monetary Fund, well above a global average of 3.3%.

Nigeria’s bond sale Tuesday showed that demand for risky, high-yielding bonds could be on the rise again, as investors reconsider how fast, in fact, the Fed will move to dial back some easy-money policies.

Even though the yields on Nigeria’s bonds were high compared with the past few weeks, the final yield was considerably lower than the guidance bankers gave when the deal launched earlier in the day. The $1 billion deal drew about $4 billion in offers, Nigerian Finance Minister Ngozi Okonjo-Iweala said.

“This sends a very positive message to other would-be African borrowers,” said Jean-Charles Sambor, a managing director at Everest Capital LLC, an investment firm that manages $1.8 billion in frontier and emerging markets. Frontier markets, where bonds rarely trade once issued, are considered riskier than mainstream emerging markets.

Despite the rise in borrowing costs, officials in several countries say they are sticking to their bond plans. Ghana and Kenya both plan to issue up to $1 billion in international bonds later this year. But Ghana is struggling to contain fiscal and current-account deficits that are both wider than 10%. Kenya’s budget and trade deficits are about 8% and 10%, respectively, and in March a man charged with crimes against humanity at the International Criminal Court was elected president.

Now that yields are higher, investors could be emboldened to buy African debt, even with memories of recent losses still fresh.

“After this market turbulence and repricing, yields on African bonds have become more sensible and appropriate to these countries’ risk profile,” said Charles Robertson, global chief economist at Renaissance Capital, an investment bank that specializes in emerging markets. “This should encourage investors to have a closer look at these borrowers.”

Still, for both investors and borrowers, there are reasons to remain wary.

In its economic outlook for the region published in May, the IMF said African nations should find ways other than bonds to finance budgets. Lower interest rates could tempt countries into taking on too much debt, the report said, leaving them struggling to service interest and principal payments in the future.

Rising yields could pose challenges for countries seeking to refinance existing debt, Aurelien Mali, a senior analyst at Moody’s Investors Service, wrote in a May report. “Servicing external debt remains largely untested” in an environment of tighter monetary policies, he wrote.