Netflix Should Read Amazon’s Script; Building a formidable subscriber base should be a more immediate concern than raising margins

July 16, 2013 Leave a comment

Updated July 15, 2013, 4:49 a.m. ET

Netflix Should Read Amazon’s Script

Building a formidable subscriber base should be a more immediate concern than raising margins

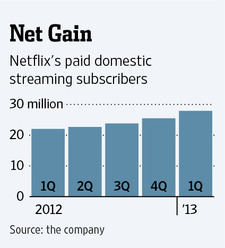

It turns out ’13 has been lucky for Netflix NFLX +0.42% . The stock has surged 178% so far, the best performance in the Standard & Poor’s 500-stock index. But to keep the odds in its favor, the video-streaming and DVD-rental company will need to be more like anAmazon.com AMZN -0.67% than an HBO. Netflix’s paid domestic streaming subscriber base has increased to nearly 28 million from 25.5 million at the start of 2013 and 22 million a year before. This puts it just below Time Warner‘sTWX -0.50% HBO. Meanwhile, Netflix’s domestic streaming margin on the basis of contribution profit, revenue less cost of sales and marketing, was 20.6% in the first quarter, up strongly from 14.3% a year earlier. But expanding margins may represent a risk for Netflix.That sounds counterintuitive. But when Netflix reports second-quarter earnings on July 22, investors will be more focused on how many subscribers it added, something that may require extra spending.

For Netflix, building a formidable subscriber base should be a more immediate concern than raising margins. Having more users enables Netflix to spread the costs of buying and creating new content. And rising market share should help it raise subscriber fees.

Considering the stock’s recent performance and the mounting evidence of its potential, investors are likely to give Netflix a free pass on margin growth for the time being if it can keep its subscriber numbers climbing. That leeway can itself be a competitive advantage: Just look at rival Amazon, which has used razor-thin margins to dominate retail, all with Wall Street’s apparent blessing. It is notable that, at 176 times 2013 earnings, Netflix’s valuation is already approaching Amazon’s 200-plus level.

Much of Netflix’s recent stock-price performance is due to a content-spending spree in late 2012 and early 2013, according to Janney Capital Markets. That saw Netflix agree to pay Walt Disney DIS -1.46% and Time Warner hundreds of millions of dollars each for shows. At the time, investors worried Netflix was spending too much. But the deals appear to have spurred subscriber growth.

Despite those deals, though, Netflix’s overall approach on investment appears cautious. It said in April that it plans to increase content and marketing costs at a slightly slower pace than revenue and will continue targeting about one percentage point of margin improvement per quarter in the U.S. Netflix’s domestic streaming margins have actually been expanding faster than that, by an average of 1.6 percentage points in each of the past four quarters.

Netflix also has become a choosier content shopper. It now targets exclusive deals for high-quality programming, opting not to pay for as much old library content as it did before. The company also is devoting some of its $2 billion-plus annual budget to original content with shows like “House of Cards,” “Arrested Development” and its latest, “Orange is the New Black.”

In a business outlook posted on Netflix’s website in April, Chief Executive Reed Hastings wrote: “We don’t and can’t compete on breadth with Comcast, CMCSA -0.98% Sky, Amazon, Apple, Microsoft,MSFT +1.15% Sony, 6758.TO -0.41% or Google, GOOG +0.33% ” adding “We have to be a focused, passion brand. Starbucks, SBUX -0.13% not 7-Eleven. Southwest, not United. HBO, not Dish.”

Yet being too HBO-like could limit Netflix’s potential audience. HBO has held fairly steady at about 29 million domestic subscribers. Netflix aims for two to three times that. Analyst estimates for Netflix’s potential subscriber base are more conservative, ranging from 43 million to about 52 million subscribers. But even 43 million represents 66% of Netflix’s future addressable market in the U.S., more than twice HBO’s penetration, according to Sanford C. Bernstein. This takes into account the projected number of households that will have an Internet connection fast enough to view Netflix and an Internet-connected TV.

Getting there may require Netflix to spend more and let margins take the brunt of that. Attracting subscribers en masse means offering a broad range of content appealing to all tastes.

In light of these challenges, recent instances of Netflix dropping content are troubling. Take its decision not to renew its deal with Nickelodeon-owner Viacom VIAB +0.76%after it ended in May. Netflix says this fit its strategy of dropping content that doesn’t get enough viewing hours and that it gets plenty of other children’s shows from the likes of Time Warner’s Cartoon Network, Walt Disney’s Disney Channel andDreamWorks Animation SKG DWA +1.58% . The company also signed a deal with DreamWorks in June for original children’s content.

But rival Amazon was quick to seize the opportunity to tap into the lucrative world of kids programming where Netflix previously had a lock, signing a deal with Viacom in June that includes some exclusive rights. Ceding ground to Amazon could lure away parents whose children watch popular Nickelodeon shows like “Dora the Explorer.” In addition, Amazon said in February that it signed an agreement for exclusive rights to the popular PBS show “Downton Abbey.”

Focusing on profits over growth is usually the preferable strategy for a firm. But in Netflix’s case, achieving scale remains key. To justify its valuation, it needs to be a multiplex, not an art-house cinema.